Hanmi Financial Corp's Loan Portfolio Growth Drives Profit Expansion Despite Volatility

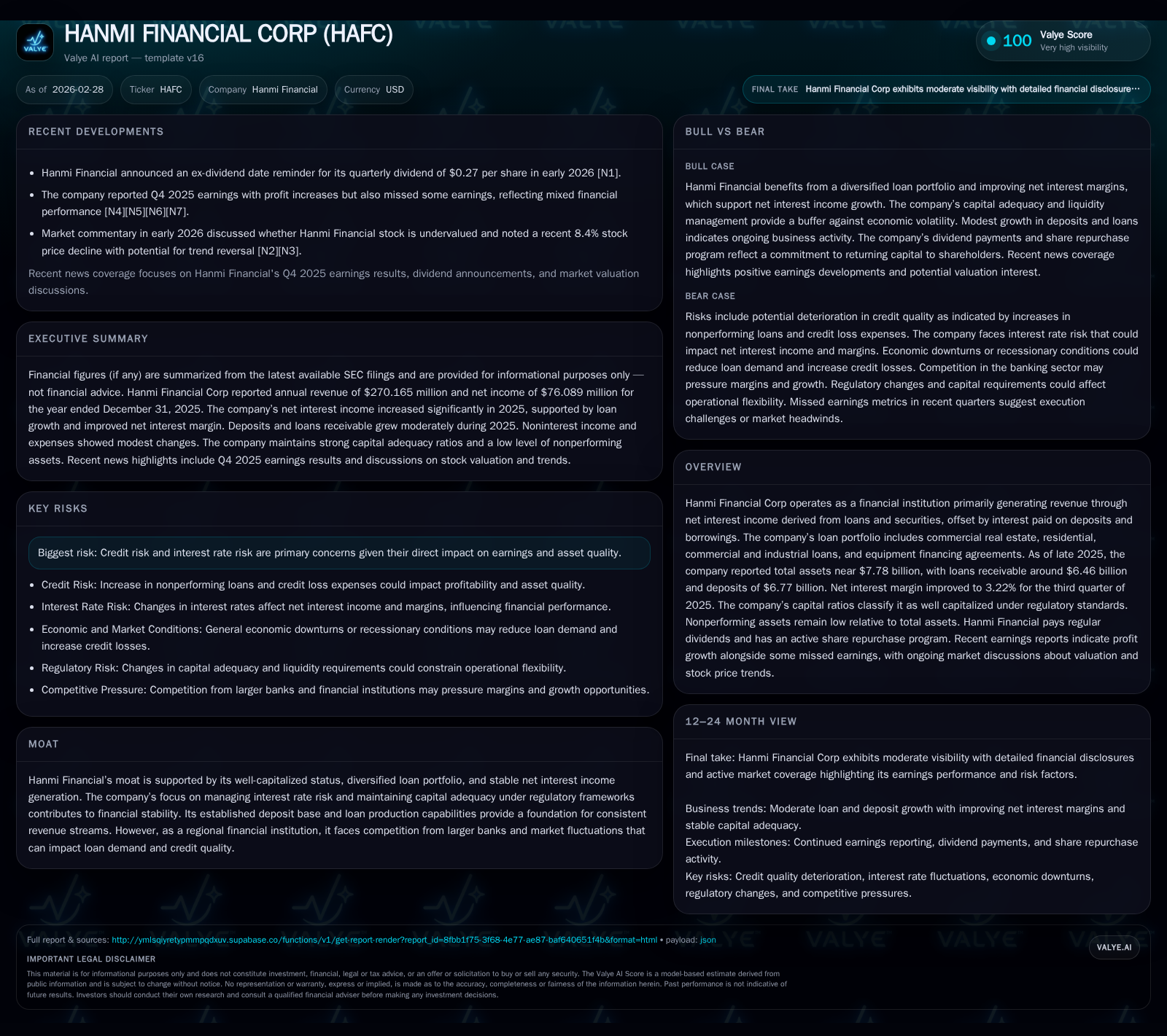

Hanmi Financial grew revenues and earnings in 2025, leveraging a diversified loan portfolio while managing credit and interest rate risks.

Hanmi Financial Corp demonstrated solid revenue and net income growth in 2025, supported by increased loan production across commercial real estate, residential, and industrial sectors. The company’s net interest margin expanded to 3.22% by Q3 2025, reflecting effective interest rate risk management. Capital ratios remain robust, categorizing Hanmi as well capitalized under regulatory standards. While credit loss provisions increased, nonperforming assets stayed low relative to total assets. Ongoing dividends and share repurchases underscore disciplined capital allocation in a competitive regional banking landscape.

Overview and Historical Performance

Hanmi Financial Corp operates as a holding company for Hanmi Bank, a community-focused state-chartered bank primarily serving Korean-American and other ethnic minority markets across several U.S. states including California, New York, Texas, and Illinois [S1]. The company's revenue stream is predominantly derived from net interest income generated by a diversified loan portfolio encompassing commercial real estate (CRE), residential mortgages, commercial and industrial (C&I) loans, SBA loans, and equipment financing agreements.

From a financial perspective, Hanmi Financial reported revenues of $270.2 million for FY2025, marking a solid increase of 15.3% compared to $234.4 million in FY2024 [F1]. Operating income rose by a comparable percentage (22.3%) reaching $76.1 million in the same period [F1]. Net income followed suit with a significant uplift of 22.3%, totaling $76.1 million for the year [F1]. This performance represents an improvement over prior trends where net income showed some variance but generally exhibited upward momentum from earlier periods.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 270 | 76 | 206 | 76 | +15.3% | +22.3% |

| 2024 | 234 | 62 | 54 | 62 | -22.3% | |

| 2023 | 80 | 108 | -21.1% | |||

| 2022 | 101 | 147 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 33 | 9 | 9.6 |

| 2024 | 30 | 6 | 8.5 |

| 2023 | 31 | 4 | 11.4 |

| 2022 | 29 | 6 | 15.9 |

Source: SEC companyfacts cache [F1].

The growth trajectory correlates closely with the expansion of the loan book as well as improvements in net interest margin (NIM), which reached approximately 3.22% by Q3 of 2025 — a meaningful improvement from around 2.74% a year earlier [S6].

Loan Portfolio Dynamics

As of late 2025, Hanmi's loans receivable stood near $6.46 billion, up approximately $277 million versus year-end 2024 [S12]. New loan originations for the nine months ending September included about $435 million in CRE loans, $242 million residential mortgages, over $300 million in C&I loans, along with significant SBA loan production totaling roughly $147 million [S12]. This diversified originations mix underscores the company's strategy of balanced exposure across multiple sectors within its community banking niche.

Nonperforming assets remain relatively low compared to overall assets despite some increases in classified loans related principally to specific CRE office loans placed on nonaccrual status during early 2025 [S23][S24]. Credit loss expense escalated notably in the first nine months of FY2025 rising to $12.5 million from just $3.5 million for the corresponding prior period; this increase was primarily due to higher net charge-offs reflecting elevated delinquencies on certain equipment financing agreements and office loans [S18]. Nonetheless, Hanmi continues emphasizing rigorous underwriting standards combined with proactive loan monitoring.

Deposits and Interest Cost Management

Deposits grew moderately to around $6.77 billion by September 30, 2025 from about $6.44 billion at the end of the prior year — a gain of approximately 5% fueled particularly by new commercial account acquisitions and branch expansions that bolstered money market and savings deposits [S25]. The company manages cost of funds effectively with average deposit costs declining from about 4.23% to near 3.63% year-over-year due primarily to falling market rates over much of the year [S18][S16].

Borrowings and subordinated debentures remained steady around approximately $220 million combined while carrying relatively stable average interest costs close to mid-4% levels [S9][S16]. The bank benefits from Federal Home Loan Bank advances as part of its liquidity management strategy.

Capital Adequacy and Regulatory Status

Hanmi's capital position remains sound with total risk-based capital ratios exceeding regulatory "well capitalized" thresholds — reported at approximately 15% total risk-based capital ratio with Tier 1 leverage above 10% as of Q3 2025 [S7]. Equity rose to nearly $796 million by fiscal year-end [F1], supporting leverage capacity and maintaining compliance amid evolving credit quality metrics.

The company routinely assesses future sources and uses of capital considering provisions for stock repurchases and dividend declarations within constraints imposed by California banking regulations that limit dividend capacity based on retained earnings or net income metrics [S4].

Dividend Policy and Share Repurchases

Hanmi maintained consistent dividend payments totaling about $32.6 million in FY2025 — modestly higher than the prior year's distribution of roughly $30.4 million [F1]. The dividend pattern confirms commitment to returning cash flow while balancing capital retention needs.

Share buybacks accelerated to approximately $9.4 million repurchased during FY2025 compared with a lower level of around $6.3 million repurchased in FY2024 [F1]. About one million shares remain authorized for repurchase under current programs illustrating ongoing shareholder return focus.

Interest Rate Risk Management

Management actively monitors interest rate risk through simulation modeling scenarios assessing impacts on net interest income and economic value measures given potential yield curve shifts [S5]. This approach aligns assets and liabilities with sensitivity limits seeking earnings stability amid volatile policy-driven rate changes nationally.

Maintaining an optimal balance between fixed-rate versus variable-rate loans contributes further resilience; approximately half the loan book carries variable or adjustable rates mitigating margin compression risks when rates fluctuate sharply downward [S13][S14].

Future Growth Prospects and Risks

Looking forward, Hanmi’s prospects rest on continued organic loan growth supported by vibrant small- and medium-sized business activity within its targeted communities alongside steady expansion of its diverse deposit base through new commercial customer onboarding and branching initiatives [N1][N2]. Sustained margin improvement efforts will hinge on managing deposit costs against evolving Fed rate policies while navigating competitive pressures from larger regional banks.

Credit quality remains an area requiring vigilance given recent upticks in charge-offs linked mainly to specialty lending segments such as equipment financing amid cyclical industry factors [S18][S24]. Any economic downturn or sector-specific stress could accentuate credit losses impacting earnings volatility.

Monitoring nonperforming asset trends closely is essential since localized CRE office space challenges represent one known pressure point although overall asset delinquency levels remain controlled relative to peers.

No explicit full-year earnings guidance has been issued by management post-FY2025 filings; thus industry participants will watch Q1/early fiscal updates regarding loan growth momentum and credit provisions as critical near-term milestones [N2][N3].

Historical Financial Summary

| Fiscal Year | Revenue (USD millions) | Operating Income (USD millions) | Net Income (USD millions) | Dividends Paid (USD millions) | Share Repurchases (USD millions) | Equity (USD millions) |

|---|---|---|---|---|---|---|

| FY2025 | 270.2 | 76.1 | 76.1 | 32.6 | 9.4 | 796 |

| FY2024 | 234.4 | 62.2 | 62.2 | 30.4 | 6.3 | 732 |

| FY2023 | - | - | 80 | 30.5 | 4 | 702 |

Conclusion

Hanmi Financial Corp has successfully grown revenue and profits through deliberate expansion of its core lending franchise complemented by disciplined asset-liability management resulting in improved margins amidst challenging economic conditions for regional banks broadly. The company’s capitalization strength provides operational flexibility while regular dividends plus share repurchases underline steady returns focus conducive for its niche clientele base. However, elevated credit costs signal emerging risks particularly linked to some segments vulnerable under tighter financial conditions; persistent diligence here is needed going forward. Overall, Hanmi remains characterized as a well-capitalized regional financial institution catering to ethnically diverse communities leveraged on stable funding coupled with varied commercial loan exposures forming its competitive moat.

This report is based solely on publicly available information including SEC filings ([F1],[S#]) and recent news reports ([N#]). It does not contain investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments