Hackett Group’s Turnaround: Unearthing Growth in Consultative AI and Enterprise Platforms

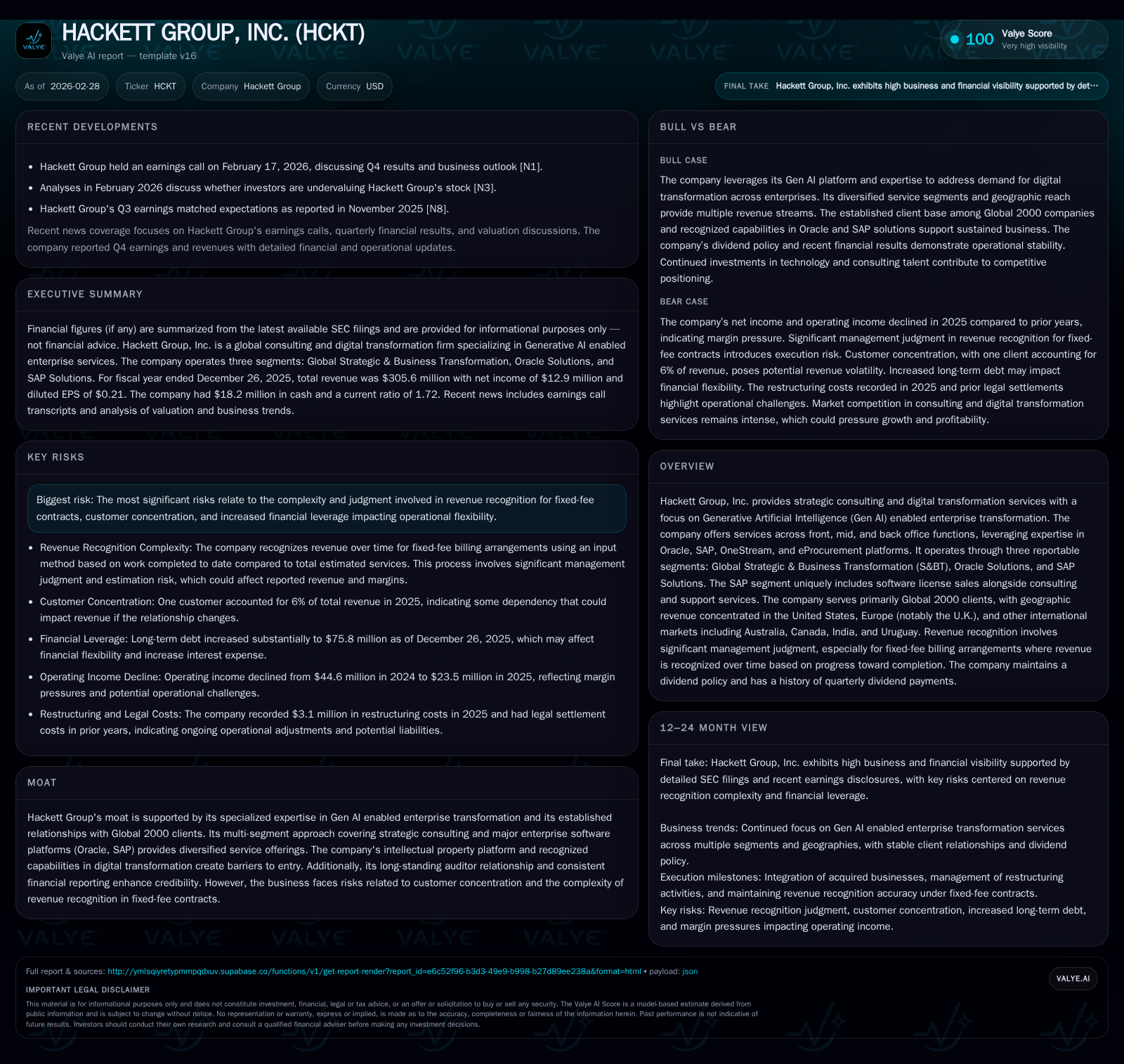

Hackett Group exhibits a financial rebound driven by its Gen AI-enabled consulting services while navigating revenue recognition and customer concentration complexities.

Hackett Group, Inc. demonstrated a notable recovery in operating and net income in fiscal year 2025, grounded in strategic emphasis on generative AI-enabled enterprise transformation across consulting and platform segments. Despite modest top-line growth of 2.5%, the company leveraged operating leverage and cost controls to boost margins, even as cash flow from operations declined by 15.6% alongside capital expenditure nearly doubling year-over-year. The business benefits from a diversified multi-segment structure including Global Strategic & Business Transformation (S&BT), Oracle Solutions, and SAP Solutions—each increasingly infused with AI-driven innovation—yet must manage risks stemming from complex fixed-fee contract revenue recognition and significant client concentration. Capital allocation reflects disciplined share repurchases and dividend payments supported by a strengthened balance sheet, though rising leverage warrants monitoring. Going forward, growth catalysts hinge principally on escalating demand for Gen AI transformation services within global enterprises amid ongoing operational risks.

Financial Trajectory: From Revenue Stagnation to Earnings Improvement

Hackett Group’s financial performance over recent years has been characterized by modest revenue growth coupled with volatility in profitability metrics. Fiscal year 2025 marked an inflection point with operating income rebounding strongly by 17.2% to $9.1 million despite only a 2.5% increase in revenue to $305.6 million compared to FY2024 [F1]. This decoupling indicates successful operating leverage extraction and disciplined cost control amid flat top-line trends.

Net income exhibited an even sharper recovery, rising nearly 57% year-over-year to $5.6 million in FY25 [F1]. However, this earnings improvement contrasts with a decline in operating cash flow which fell by approximately 15.6% to around $40.3 million [F1]. Capital expenditures almost doubled—from about $4 million in FY24 up to $7.9 million in FY25—reflecting heavy investment into digital platforms supportive of Hackett’s AI-driven transformation services [F1][S11].

This divergence between accrual earnings and cash flow underscores the importance of monitoring working capital dynamics alongside profitability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | 40 | 9 | 8 | +56.9% |

| 2024 | 4 | 48 | 8 | 4 | -54.6% |

| 2023 | 8 | 37 | 11 | 4 | -19.2% |

| 2022 | 10 | 59 | 14 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 13 | 69 | 32 |

| 2024 | 12 | 6 | 44 |

| 2023 | 12 | 1 | 33 |

| 2022 | 10 | 117 | 54 |

Source: SEC companyfacts cache [F1].

Segment Performance Overview: S&BT, Oracle, SAP Dynamics

Hackett operates through three reportable segments: Global Strategic & Business Transformation (S&BT), Oracle Solutions, and SAP Solutions [S6][S20]. S&BT focuses on strategic consulting including transformation roadmaps; Oracle Solutions centers on EPM/ERP implementations and application management; SAP Solutions includes consulting alongside software license sales which contribute recurring revenues.

In FY25 segment revenues were approximately $169.6 million for S&BT (virtually flat vs prior year), $72.7 million for Oracle Solutions down from $85.7 million reflecting project timing variability; SAP Solutions grew to about $63.4 million driven mainly by higher software license sales which nearly doubled versus prior years [S20]. Segment contribution margin trends indicate steady margin expansion primarily via improved service delivery models within S&BT and SAP segments [S13][S14].

Revenue Recognition Complexity and Customer Concentration Risks

The company predominantly uses fixed-fee billing contracts for consulting engagements requiring significant management judgment on revenue recognition tied to contract milestones and performance obligations [S18][S20]. This complexity introduces risk related to timing differences between billings and revenues recognized that could result in variability or adjustments.

Contract liabilities stood near $12 million at fiscal year-end representing client prepayments recognized over engagement periods [S20]. One client historically accounted for as much as ~11% of consolidated revenues but more recently around ~6%, underscoring persistent customer concentration risk across segments that merits ongoing scrutiny [S17][S20].

Capital Allocation: Dividends and Share Repurchases

Hackett maintains an active capital return program with quarterly dividends totaling approximately $12.9 million paid during FY25 alongside robust share repurchases amounting to $69.1 million including a tender offer covering roughly seven percent of shares outstanding funded partly via borrowings under its credit facility [F1][S5][S12][S16].

The repurchase activity has contributed materially to treasury stock increases impacting equity balances while supporting shareholder yield.

Balance Sheet Strength & Liquidity Position

As of December 26, 2025, cash & equivalents stood at approximately $18.2 million with current assets exceeding current liabilities resulting in a current ratio of around 1.72x indicating solid short-term liquidity [F1][S8][S10]. Total equity was about $68 million down from over $115 million prior year primarily due to treasury stock purchases.

Long-term debt increased significantly from about $13 million at end-FY24 to roughly $76 million at end-FY25 reflecting borrowings used to finance share repurchases under the revolving credit facility maturing in November 2027 [F1][S4][S10]. Interest rates on debt shifted from BSBY to SOFR benchmarks with margins dependent on leverage ratios.

Free cash flow approximated $32.4 million calculated as operating cash flow less capital expenditures evidencing positive cash generation albeit reduced relative to earlier years due to elevated investment spend fueling growth platforms inclusive of internal-use software capitalization aligned with evolving AI offerings [F1][S11][S23].

Outlook: Growth Catalysts Amid Operational Risks

Management highlights accelerating demand for generative AI-enabled enterprise transformation services among large multinational clients seeking digital modernization and cost optimization initiatives [N1][N4][S3]. Geographic expansion efforts target emerging markets such as India and Uruguay leveraging remote delivery advantages.

While optimistic regarding pipeline growth particularly via embedded software licenses within SAP solutions, management remains cautious given competitive pressures among boutique and global consultancies plus macroeconomic uncertainties affecting IT budgets [N2][N4][S3]. Monitoring order backlog trends segmented by service lines alongside AI platform deployment progress will be critical indicators.

This analysis is based exclusively on Hackett Group’s SEC filings through February 27th, 2026 ([F1],[S#]) and recent public earnings transcripts ([N#]). No speculative projections have been made.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments