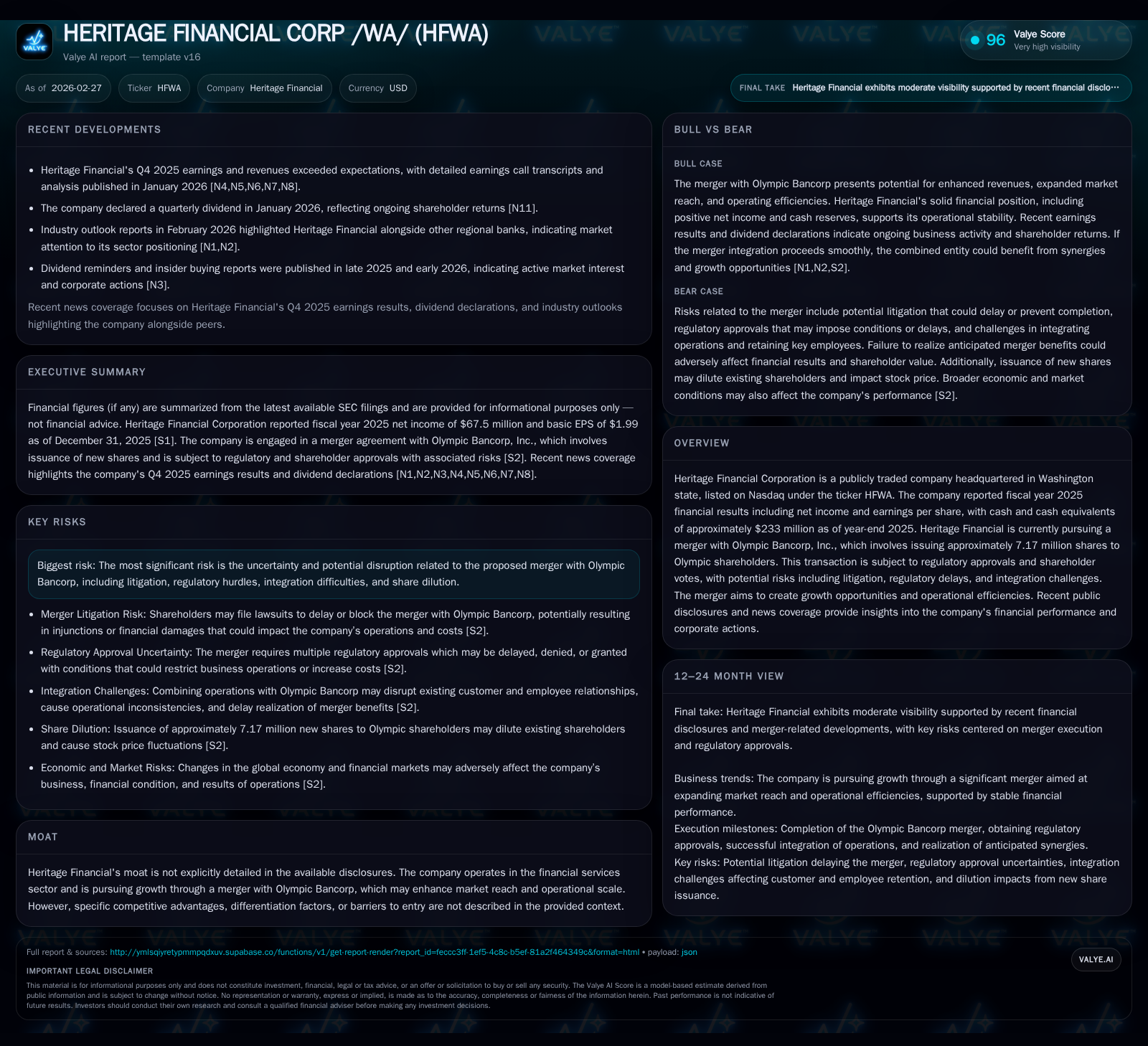

Heritage Financial Corp Strengthens Market Footprint Through Strategic Merger and Loan Portfolio Expansion

Heritage Financial leverages its merger with Olympic Bancorp and robust loan funding strategy to fuel earnings growth and operational scale.

Heritage Financial Corporation reported a noteworthy 56.1% increase in net income for fiscal year 2025, underpinned by strategic growth initiatives including its January 2026 merger with Olympic Bancorp. The company’s disciplined focus on expanding non-maturity deposits, coupled with a diversified commercial loan portfolio featuring balanced fixed and adjustable rate exposures, provides a stable foundation for further expansion. Despite integration and regulatory risks associated with the merger, Heritage maintains strong capital adequacy and prudent capital allocation, supporting consistent dividends and buybacks. Going forward, monitoring deposit traction, loan origination pace, and merger synergy realization will be crucial indicators of sustained performance momentum.

From Established Regional Bank to Growth Catalyst: Reviewing Heritage Financial’s Historical Performance

Heritage Financial Corporation demonstrated a marked financial uptick in fiscal year (FY) 2025, recording net income of approximately $67.5 million—a robust increase of +56.1% over the prior year’s $43.3 million [F1]. This earnings surge was propelled by a combination of organic loan portfolio growth and the strategic momentum generated by the pending merger with Olympic Bancorp.

Operating cash flow (CFO) also expanded significantly to about $94.8 million in FY25, an increase of roughly 47% compared to $64.5 million in FY24 [F1]. The spike reflects higher cash inflows from lending activities complemented by intensified operational investments; capital expenditures nearly tripled from $3.46 million to $9.16 million year-over-year as Heritage ramped up branch openings and digital enhancements aimed at sustaining competitive positioning [F1]. Equity grew by over $58 million to $921.5 million at fiscal year-end [F1].

These financial inflections underscore Heritage’s transition from a historically regional lender toward becoming a more sizeable growth-oriented institution leveraging strategic mergers and an expanding loan book footprint.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 68 | 95 | 9 | +56.1% |

| 2024 | 43 | 64 | 3 | -30.0% |

| 2023 | 62 | 110 | 10 | -24.6% |

| 2022 | 82 | 94 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 6 | 86 | 7.3 |

| 2024 | 22 | 61 | 5.0 |

| 2023 | 7 | 99 | 7.2 |

| 2022 | 3 | 90 | 10.3 |

Source: SEC companyfacts cache [F1].

Table: Heritage Financial annual financial summary illustrating key profit and cash flow drivers plus investment trends [F1]

Deposit Growth & Loan Portfolio Development: Foundations of Operational Expansion

A pillar of Heritage’s strategy is cultivating robust non-maturity deposits—funds without contractual maturities that provide flexible liquidity and stable funding for lending activities [S1]. At the end of FY25 non-maturity deposits represented a commanding majority at about 84.1% of total deposits [S1], emphasizing relationship-based banking targeting both retail and local business customers through enhanced branch networks and online offerings.

Loan portfolio composition as of December 31st documented an aggregated amortized cost of roughly $4.78 billion across diverse segments [S1]:

- Commercial business loans dominated with nearly $3.91 billion (~82%), divided into commercial & industrial loans ($818 million), owner-occupied commercial real estate ($1.03 billion), and non-owner occupied CRE ($2.06 billion).

- Residential real estate loans stood at approximately $359 million.

- Real estate construction and land development comprised about $343 million.

- Consumer loans totaled around $170 million.

In terms of interest rate characteristics for loans due beyond one year (~$4.30 billion), nearly an even split existed between fixed/predetermined rates ($2.19 billion) and floating/adjustable rates ($2.11 billion). The sizable exposure to adjustable rate loans is partially mitigated through interest rate swap contracts on ~$259 million of commercial loans enabling effective adjustment based on one-month SOFR plus margin [S1]. This sophisticated hedging underscores prudent asset/liability matching.

| Loan Segment | $ Amortized Cost Total (Thousands USD) | % Fixed / Predetermined Interest Rates | % Floating/Adjustable Interest Rates |

|---|---|---|---|

| Commercial & Industrial | N/A* | Approximate equal split N/A | Approximate equal split N/A |

| Owner-Occupied CRE | N/A | Approximate equal split N/A | Approximate equal split N/A |

| Non-Owner Occupied CRE | N/A | Approximate equal split N/A | Approximate equal split N/A |

*Detailed breakdown available within SEC disclosures but exact dollar splits by segment not enumerated in provided excerpts [S1]. Analysis based on narrative descriptions.

This diversified loan mix coupled with stable core deposit funding supports Heritage's ongoing growth ambitions while managing interest rate risk exposure prudently.

Merger Synergies and Integration Risks: The Olympic Bancorp Transaction in Focus

The transformative acquisition of Olympic Bancorp completed on January 31st expanded Heritage’s scale materially; Olympic’s Kitsap Bank merged into Heritage Bank immediately thereafter forming a unified banking entity headquartered in Washington State [S3], [S9], enhancing total assets beyond previously reported figures.

This stock-for-stock transaction involved issuance of approximately 7.17 million shares to Olympic’s shareholders—a significant dilutive event but aligned with strategic objectives to broaden market reach and operational capabilities [S2], [S13]. The boards expected revenue synergies via cross-selling opportunities alongside operating efficiencies from combined infrastructure.

Nonetheless the transaction carries notable risks detailed explicitly in SEC filings: potential delays or prohibitions stemming from litigation or regulatory orders could result in significant cost overruns or impair expected benefits [S4], [S10]. Also integration challenges—including retention of key personnel—may disrupt customer relationships or complicate systems harmonization thereby impacting near-term financials negatively [S5], [S13].

Shareholder approval processes progressed favorably with ~80% turnout voted affirmatively for stock issuance underpinning completion readiness [S16]. Regulatory approvals were secured late December ahead of closing but ongoing scrutiny remains critical [S24].

Hence while strategically accretive long-term the transaction's success hinges upon execution efficacy against explicit legal and regulatory headwinds.

Capital Structure & Allocation: Balancing Shareholder Returns with Strategic Investments

Heritage Financial enters this expanded phase with solid capital cushion—consolidated common equity tier 1 (CET1) capital ratio stands at a healthy 12.7%, well above regulatory “well-capitalized” thresholds; leverage ratio is also strong at approximately 10.8% [S1]. These metrics affirm resilience amid balance sheet growth triggered by the merger.

Return on equity for FY25 hovers near an estimated 7.3%, reflecting reasonable earnings generation against expanded equity base [$67.5M net income / ~$921M equity] [F1]. This moderate ROE aligns with regional banking norms where incremental scale involves capital absorption post-acquisition.

Capital allocation actions show consistent quarterly dividends at a payout around $0.24 per common share confirmed for early February payment [N8], [S21]. Simultaneously buyback activity decreased noticeably from ~$22M in FY24 to ~$5.5M FY25 due primarily to recent equity issued for merger consideration limiting repurchase capacity temporarily[F1],[S11], [S16].

Free cash flow remains constructive after capex absorption—about $85.7 million calculated as operating cash flow less capex —underscoring operational cash generation that supports both internal reinvestment and shareholder distributions.[F1]

Continued covenant compliance remains intact as shown by stable risk-based capital ratios maintained through Q4 filings[S6]–[S9].

Asset Quality and Interest Rate Risk Management: Safeguarding Earnings Amid Market Volatility

Asset quality metrics reveal controlled risk levels consistent with conservative underwriting protocols emphasized within commercial real estate (CRE) lending segments.[S1] Non-accrual loan volumes are low relative to total balances indicating minimal credit stress despite macroeconomic uncertainties.[S4]

Interest rate risk management extends beyond natural portfolio diversity through derivatives usage; notably non-hedged interest rate swaps tied to substantial commercial loan portions (@$259m notional) help hedge income volatility linked to floating SOFR rates plus margin adjustments.[S1]

Goodwill arising from historic acquisitions underwent annual impairment testing in late Q4-2025 incorporating qualitative assessments factoring economic environment shifts but showed no impairments confirming underlying asset valuations remain reasonable post-Olympic merger.[S1]

Regulatory oversight continues proactive review focusing on capital adequacy vis-à-vis interest rate risk exposures encapsulated within Board-established limits monitored rigorously through Asset/Liability committees.[S1]

What Comes Next: Milestones, Regulatory Watchpoints, and Indicators for Future Performance

Looking forward into FY26 endpoints several focal points emerge:

- Integration milestones for Olympic Bancorp assimilation remain pivotal including IT system convergence timelines alongside personnel retention results whose outcomes will materially shape synergy realization pace.[N3], [S2]

- Deposit growth sustainability particularly maintenance or improvement above historical run-rates will influence funding costs dynamics given the current emphasis on relationship deposits comprising ~84%. Monitoring shifts toward maturity products or competitive pressures will be essential.[N6]

- Loan originations cadence particularly within middle market commercial sectors will test underwriting discipline versus volume aims amid evolving regional economic factors.[N6]

- Earnings margin preservation amidst fluctuating interest rates tracked alongside derivative effectiveness offers another performance bellwether.[N9]

- Any litigation developments arising from shareholder suits or regulatory investigations related to the merger could introduce episodic volatility requiring attention.[S10]

- Capital allocation adjustments balancing shareholder returns via dividends/buybacks against incremental investment needs post-merger will signal management priorities evolving under new scale conditions.[N10]

Collectively these areas form critical monitoring vectors suggesting whether Heritage leverages its expanded platform effectively or encounters unforeseen obstacles curtailing ambitions.

This analysis is prepared solely for informational purposes based on publicly available disclosures including SEC filings and recent disclosures as of early calendar year 2026; it does not constitute investment advice nor imply any specific recommendation regarding security transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments