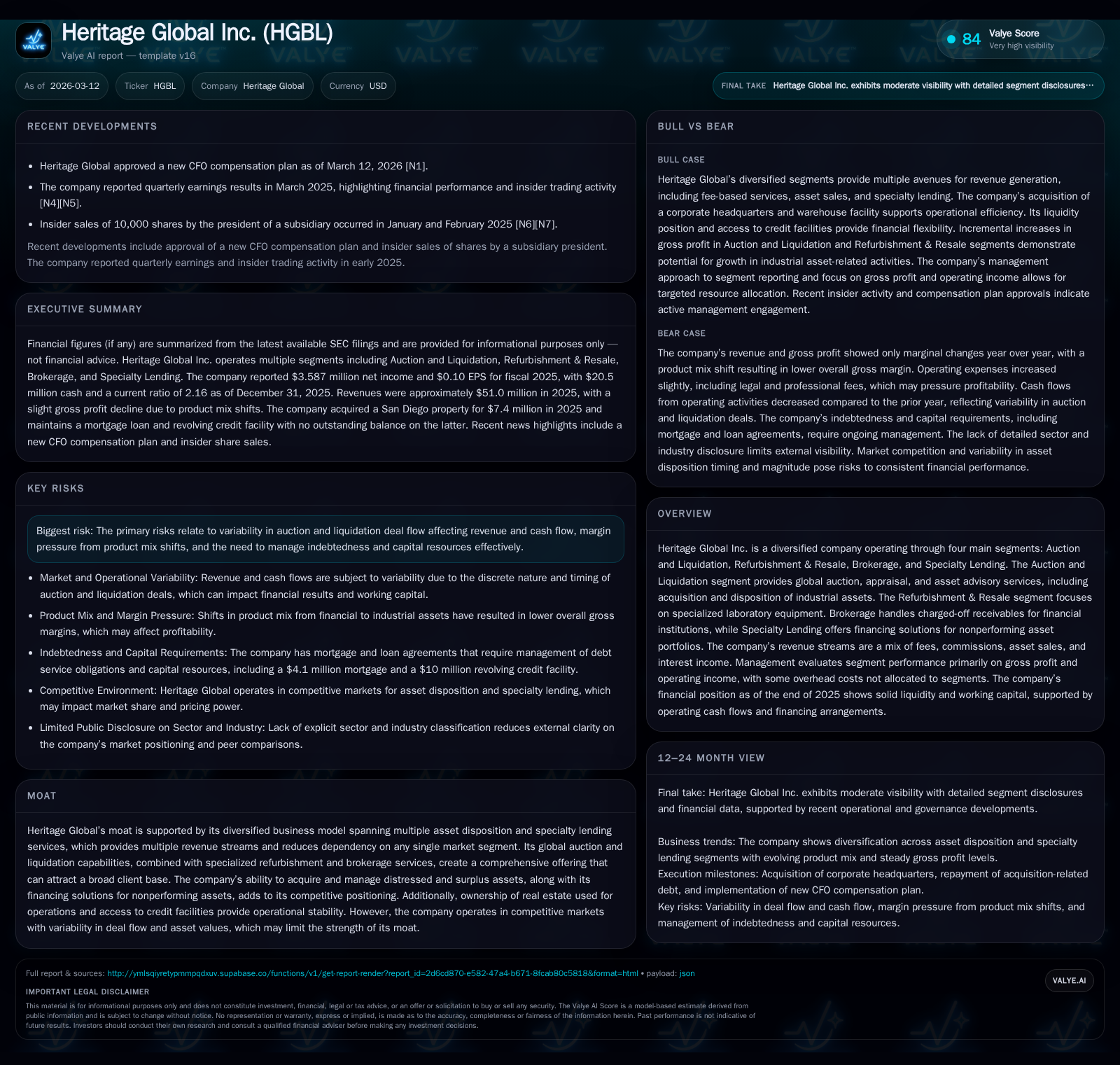

Heritage Global Inc.: Assessing Multi-Segment Resilience and Capital Strategy

The company’s 2025 earnings contraction contrasts with strategic investments in fixed assets and liquidity preservation efforts.

Heritage Global Inc. operates a diversified portfolio spanning auctions, refurbishment, brokerage, and specialty lending, supported by multiple revenue streams that dampen reliance on any single market. Despite a notable year-over-year revenue drop of 15.4% in 2025 driven by deal flow variability and product mix shifts, the company maintained positive operating income and net profit amid margin pressures. Significant capital deployment included acquiring corporate real estate and a sharp rise in capex, balanced against steady cash flow generation and ongoing share repurchases. Going forward, monitoring debt covenant adherence and segment-specific gross profit will be key to assessing recovery resilience.

Four-Pronged Business Model: Drivers Behind Past Growth

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 4 | 6 | 6 | 8 | -30.8% |

| 2024 | 5 | 8 | 9 | 0 | -58.5% |

| 2023 | 12 | 13 | 14 | 0 | -19.5% |

| 2022 | 15 | 6 | 11 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | -2 | 5.4 |

| 2024 | 2 | 8 | 7.9 |

| 2023 | 0 | 13 | 20.4 |

| 2022 | 0 | 6 | 32.1 |

Source: SEC companyfacts cache [F1].

Heritage Global Inc. executes a diversified operational strategy through four distinct segments: Auction and Liquidation (HGP), Refurbishment & Resale (ALT), Brokerage (NLEX), and Specialty Lending (HGC) [S15][S16]. This multi-segment approach underpins the company's ability to generate revenues from fees, commissions, asset sales, and interest income—each contributing variably across segments.

The Auction and Liquidation segment offers global services including auctions, appraisals, asset advisory, and acquisition/disposition of industrial equipment [S15], effectively managing deal flow variability common in asset disposition markets. Refurbishment & Resale targets specialized laboratory equipment sales enhanced by proprietary refurbishment capabilities, providing a differentiated product source [S15]. Brokerage focuses on charged-off receivables' secondary markets for financial institutions primarily in the U.S. and Canada, while Specialty Lending extends financing solutions for nonperforming asset portfolios [S15].

Combined, these segments cultivate multiple revenue streams that act as buffers against isolated market downturns or regulatory impacts—a notable competitive moat albeit subject to industry cyclicality . Importantly, gross profit and operating income are primary metrics management uses for segment performance evaluation, though overhead expenses remain largely unallocated among divisions [S16].

2025 Financial Setbacks: Revenue and Margin Pressures

Heritage Global reported annual revenue of approximately $51 million in 2025, declining around 15.4% compared to $60.3 million in the prior year [F1]. This pullback was mainly attributed to decreased auction deal flow volumes coupled with a product mix shift away from higher-margin financial assets toward lower-margin industrial asset sales within their Auction and Liquidation operations [S24].

Correspondingly, the company’s operating income dropped sharply by roughly 37%, from about $9.07 million in 2024 to $5.71 million in 2025 [F1], reflecting margin compression driven by rising costs associated with physical inventory management of industrial assets as opposed to services or brokerage fees—which usually have higher margins [S24]. Net income followed suit, falling approximately 30.8% year-over-year to an estimated $3.6 million [F1]. This decline also impacted return measures; the calculated ROE was modest at about 5.4%, reflecting reduced profitability relative to shareholder equity [F1].

The quarterly variability typical of Heritage Global's auction business means timing mismatches between deal execution and revenue recognition further accentuate fluctuations—considerations important when interpreting interim periodic results [S4].

Capital Structure Strength: Real Estate Investment and Debt Overview

In early 2025, Heritage strategically invested $7.4 million to acquire a corporate headquarters building in San Diego intended for both office use and warehousing Auction and Liquidation segment assets [S1][S13]. To finance this purchase, it secured a $4.1 million mortgage term loan with an effective weighted average interest rate near 6.42%, representing a notable improvement over prior borrowing costs (~8.75% in the previous year) [S5][F1], suggesting favorable refinancing terms.

The company’s existing debt profile includes a revolving credit facility authorized at $10 million but with zero outstanding balance as of December 31, 2025 [S1][S9], signifying prudent liquidity management without excessive leverage drawdown.

Notably, Heritage fully retired the ALT Note ($2 million principal) during the year, thereby simplifying its debt obligations [S1]. The extended maturity date on its credit facility through June 2026 reduces near-term refinancing risk but necessitates vigilance over covenant compliance ahead of that timeline [S6][N1].

Liquidity Trends: Working Capital, Cash Flows, and Operational Cash Generation

As of fiscal year-end 2025, working capital stood at roughly $18.1 million—a slight decrease from $18.5 million at FY2024-end—but still reflective of solid short-term liquidity given current liabilities rose moderately primarily due to payables increases linked to operational scaling or timing differences in settlements across vendor accounts [F1][S8]. The current ratio approximated a healthy 2.16x underlining sufficient cushion.

Operating cash flows declined about 20.8% to nearly $6.14 million versus previous years largely due to reduced earnings accompanied by shifts in operating asset cycles particularly notes receivable collections influenced by Specialty Lending operations [F1][S8][S17]. The company's receipt profile is cyclical due mainly to discrete auction transactions whose value varies substantially by period end [S4].

Additionally, an increase in inventory balances tied to refurbishing laboratory equipment slightly tightened cash conversion dynamics though strategic expansions occur continuously within core segments [S8][S18].

Strategic Capital Deployment: Capex Surge and Buyback Activity

A striking feature of Heritage’s financials is the stark escalation in capital expenditures—swelling from negligible levels (~$0.14 million in FY2024) up over six thousand percent to approximately $8.47 million in FY2025—primarily driven by investment into their new San Diego headquarters facility together with incremental note receivable extensions supporting specialty lending activities [F1][S23].

This transition represents a strategic repositioning investment contrasting with routine maintenance spend historically observed.

Concurrently, the company continued repurchasing shares under its board-approved repurchase programs with buybacks totaling about $2.63 million during the year versus ~$2.20 million prior year—a meaningful expression of confidence aimed at enhancing shareholder value despite near-term earnings softness given execution flexibility afforded by strong liquidity reserves [F1][S12][S26].

Outlook Considerations: Variable Deal Flow and Market Dependency Risks

Going forward, Heritage Global remains exposed chiefly to variability inherent in auction deal flow volume—a factor that materially influences revenue recognition and subsequent cash generation through fluctuating fee-based contracts or asset sales transactions within its Auction and Liquidation segment [N1]. Competitive pressures restrain pricing power margins especially amidst shifting product mix toward more capital-intensive industrial assets with inherently lower gross margins.

Management has articulated confidence that existing liquidity combined with forecasted operating cash flows will suffice for sustaining operations without needing immediate material external financing support barring unforeseen market disruptions or credit deterioration trends within specialty lending portfolios which itself is undergoing active workout arrangements addressing delinquencies on nonaccrual loans approximating nearly $24 million amortized basis as of December 31 [S11][S17].

These factors collectively dictate close monitoring of segment-level gross profits alongside macroeconomic conditions affecting asset disposition markets.

What to Watch Next: Debt Covenant Compliance and Segment Performance Indicators

Of particular importance will be Heritage Global's adherence to debt covenants embedded within its modified credit agreements expiring mid-2026—including timely repayment schedules on term loans originating from property acquisition efforts—and maintenance of financial covenants even when dealing with episodic earnings swings induced by discrete auction transactions [S9][N1].

Additional signals will arise from granular segment profitability trajectories focusing on gross profit contributions across Auction & Liquidation versus Specialty Lending where workout resolutions appear ongoing yet protracted—these being leading indicators for potential earnings stabilization or further margin degradation ahead.

Financial statement notes hint at continuing scrutiny regarding equity method investments' valuations impacting operating income sourced from joint ventures interacting closely with primary segments (notably ALT for laboratory refurbishments) suggesting investors should triangulate such non-cash accounting effects when evaluating operational momentum [S16][S24].

This analysis integrates information solely derived from verified SEC filings ([F1], [S#]) and officially reported news ([N#]) as of early March 2026 without speculative extrapolation beyond those sources' disclosures. All interpretations strive for neutrality absent any investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments