Eventbrite’s Growth Stalls with Declining Paid Ticket Volume and Merger Transition

Eventbrite faces revenue pressure amid a sizable merger and competitive challenges in the live event ticketing marketplace.

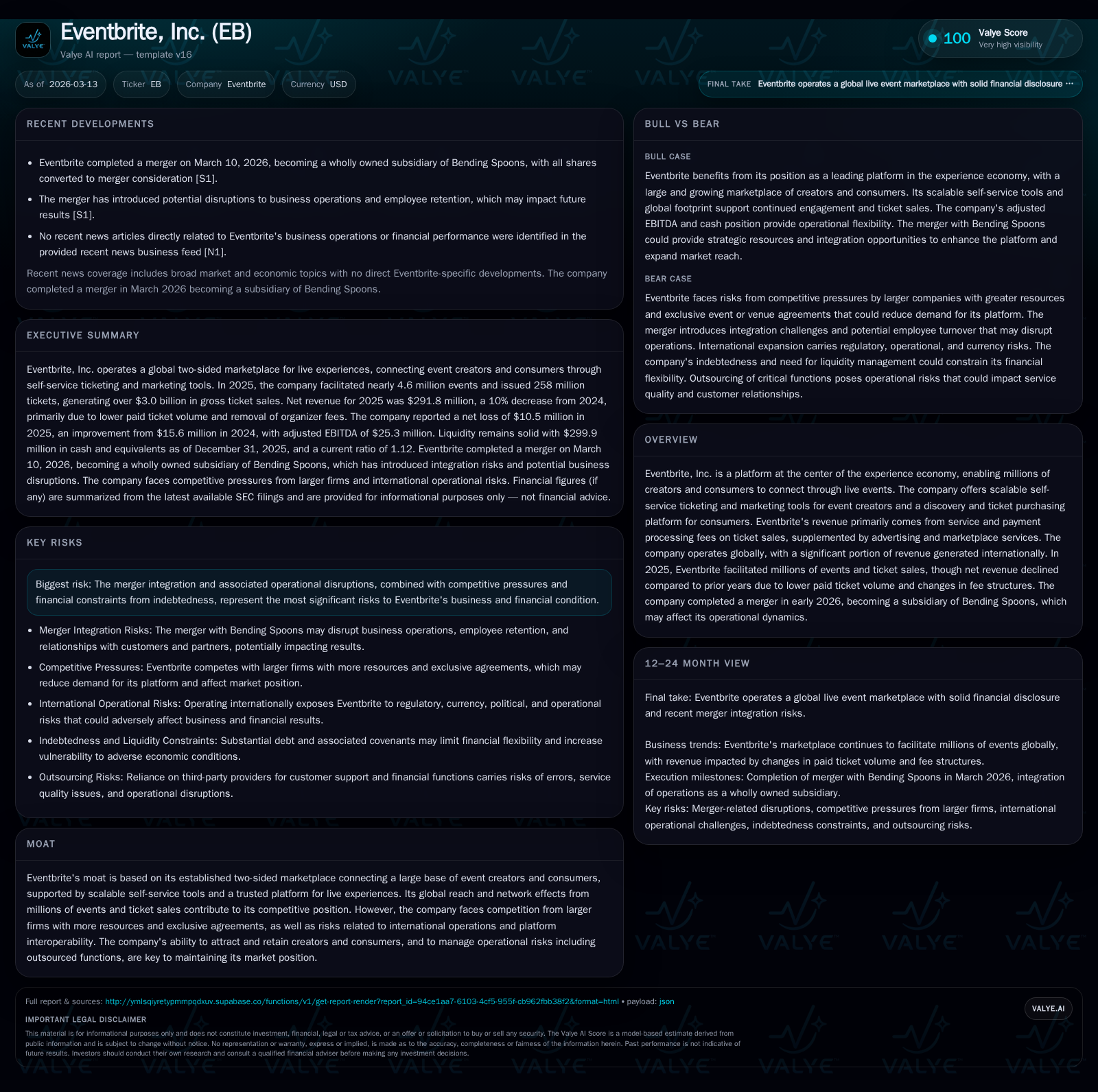

Eventbrite, Inc., a key player in live event ticketing and experience economy, has seen its revenue decline since peaking in 2023 largely due to falling paid ticket volume and fee structure changes. Recently acquired by Bending Spoons, the company’s standalone public financials reflect operational stresses including margin compression and subdued cash flow. Growth prospects hinge on integration success post-merger, international expansion, and competitive positioning against larger rivals. Capital allocation has been conservative recently, with no repurchases after substantial buybacks in 2024. Monitoring merger-related disruption, debt servicing costs, and market expansion execution will be critical going forward.

Company Overview and Historical Performance

Eventbrite operates as a global platform facilitating live event creation and discovery within the experience economy. Its core offering features scalable self-service ticketing and marketing tools that connect millions of creators with consumers monthly. The company’s revenue stems mostly from service fees on paid tickets plus payment processing fees, alongside advertising and other marketplace revenues [S1].

Financially, Eventbrite saw top-line growth from $106 million in 2020 to over $326 million by 2023—a compound annual growth trajectory powered by increased adoption of live events post-pandemic recovery [F1]. However, this traction has reversed somewhat since, with net revenue decreasing about 10% to just under $292 million in 2025 [F1], driven primarily by a decline in paid ticket volume.

Paid ticket volumes illustrate this trend clearly: dropping from roughly 93.4 million tickets sold in FY23 to around 78.9 million in FY25—a near-15% contraction over two years [S1]. Approximately 40%-41% of this volume originates outside the U.S., underscoring Eventbrite's broad geographic footprint though margins vary internationally due to payment processing cost differences [S1][S8]. The removal of organizer fees in late 2024 also significantly impacted higher-margin revenue components negatively influencing gross margin (down from approximately 70% in FY24 to about 68% in FY25) [S8][F1].

Operating losses have improved year-over-year yet remain material: operating income loss narrowed from roughly $31 million in FY24 to $26 million negative in FY25; net losses followed a similar pattern shrinking to -$10.5 million in FY25 [F1]. This reflects cost discipline notably on product development spend which fell ~24%, mainly due to headcount reductions following prior restructuring [S16][F1]. Marketing and support expenses were similarly reduced although these categories remain significant portions of overall operating costs.

Operating cash flow proved more challenging—falling by over half from $35.6 million to $17.7 million between FY24 and FY25—while capital expenditures were minimal ($95k) indicating a tight rein on investments [F1]. Capital allocation stopped short of share repurchases for the period ending FY25, contrasting sharply with approximately $50 million repurchased during FY24 before suspending buybacks amid pending merger activity [S5][F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -11 | 18 | -26 | +32.5% | ||

| 2024 | -16 | 36 | -31 | +41.2% | ||

| 2023 | 326 | -26 | 19 | -41 | +25.0% | +52.2% |

| 2022 | 261 | -55 | 9 | -47 | +39.4% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 18 | -5.9 |

| 2024 | 50 | 35 | -9.1 |

| 2023 | 18 | -13.8 | |

| 2022 | 7 | -33.3 |

Source: SEC companyfacts cache [F1].

Note: Buyback values pertain mainly to repurchase of Class A common stock.

Merger Impact and Operational Context

A watershed event for Eventbrite occurred with the March 10, 2026 completion of an all-cash merger with Bending Spoons S.p.A., formerly announced late December prior year [S1][S3]. The transaction valued shares at $4.50 each in cash consideration leading to cancellation of public shares subsequently delisting Eventbrite from NYSE [S1]. As a result, ongoing standalone financial disclosures will cease.

Management identified risks inherent in such a transition including disruptions to business operations, potential loss of key personnel fearing uncertainty, strained vendor/customer relations due to shifting control dynamics, as well as incurring substantial one-off integration costs [S10][S19]. Shareholders relinquish exposure to future upside or any equity participation post-merger given cash-out structure.

Competitive Positioning & Moat

Eventbrite’s defensibility rests chiefly on its established two-sided network—the extensive base of creators relies on its self-service technology while consumers benefit from broad event discovery capabilities [N/A]. This large-scale marketplace dynamic fosters network effects crucial for sustaining liquidity and reducing switching incentives.

However, the landscape is intensely competitive with global incumbents wielding deeper pockets or exclusive partnerships that can fragment creator loyalty or consumer engagement. International expansion offers both opportunities—such as cost-efficient payment processing—and risks linked to regulatory compliance complexity notably GDPR interpretations, cross-border data transfer scrutiny, anti-corruption statutes and local consumer protection laws [S10][S11][S13].

Risks & Regulatory Environment

Beyond integration challenges due to recent ownership change, Eventbrite confronts continuing operational risks including debt servicing constraints from convertible notes maturing between now and next few years combined with restrictive covenants embedded within credit agreements limiting financial flexibility [S6][S7][S14][F1]. Furthermore:

- Data privacy laws globally are increasing compliance burdens with fines or penalties for breaches affecting platform usage patterns.

- Ticketing-specific regulatory reforms aspire for transparency which may require costly system changes.

- Global trade sanctions complicate cross-border service provisioning requiring diligent controls.

- Intellectual property protection demands ongoing enforcement efforts exposing management time and resources.

Failure or perceived failure on these fronts could erode trust undermining Eventbrite’s creator-consumer network effect.

Growth Prospects & Outlook (Analysis)

Post-merger prospects hinge critically on several dimensions:

- Successful operational integration minimizing disruption while capturing synergies; retention of key talent is paramount.

- Recovery or growth of paid ticket volumes via platform innovation or expanding appeal internationally where less saturated markets exist.

- Monetization mix optimization balancing organizer fees restoration or alternative offerings without deterring participants.

- Navigating evolving regulation efficiently maintaining compliance while avoiding punitive costs.

- Leveraging Bending Spoons’ resources potentially for technology development enhancements or market reach extension.

Absent explicit company guidance on milestones post-merger due to cessation of public disclosure obligations, stakeholders should monitor third-party communications for signs around user engagement trends or strategic pivots.

Capital Allocation & Financial Health

With no dividends declared historically and zero share repurchases following material buybacks ahead of the merger completion [$49.7M repurchased in FY24], Eventbrite prioritized deleveraging approximately through repurchasing convertible notes early while controlling operating expenses [S5][F1]. The company maintains a modest capital expenditure profile consistent with SaaS-style platforms focusing investments judiciously.[F1]

Its approx ROE is currently negative (-5.9%) driven by recurring net losses despite narrowing trends reflecting ongoing investment phase coupled with pandemic normalization impacts on live events demand [F1]. Operating cash flow remains positive but halved year over year highlighting thinner buffer for discretionary spending or further deleveraging absent external financing sources currently constrained by market conditions.[F1][S18]

Conclusion

Eventbrite stands at a crossroads: as a long-established facilitator within the experience economy's live events niche facing stagnant or contracting paid ticket volumes amid heightened competition, regulatory scrutiny, and structural changes following its acquisition by Bending Spoons. The historical momentum that drove strong revenue growth up through early-mid pandemic recovery has slowed notably post-2023 tied also to fee removals impacting margins negatively.

The company’s future hinges largely on effective merger execution mitigating operational friction; expansion strategies especially internationally balanced against regulatory complexity; stable capital structure management amidst existing debt loads; sustaining platform relevance against entrenched competitors; and reaccelerating user engagement metrics including paid ticket sales volumes without sacrificing net profitability further.

Investors should be alert for early indicators emanating from integration progress updates or shifts in audience behavior landscaping post-merger since public financial reporting will cease underway going forward restricting transparency into direct performance drivers beyond what parent-level disclosures provide.

This analysis is based exclusively on publicly available information as of March 13, 2026 extracted from SEC filings (Forms 10-K/10-Q/8-K), official company announcements, validated numeric financial data ([F1]), and reputable news sources ([N#]). It does not constitute investment advice or recommendation but aims solely at providing an informed corporate performance overview integrating operational context within pertinent industry dynamics relevant for professional due diligence purposes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments