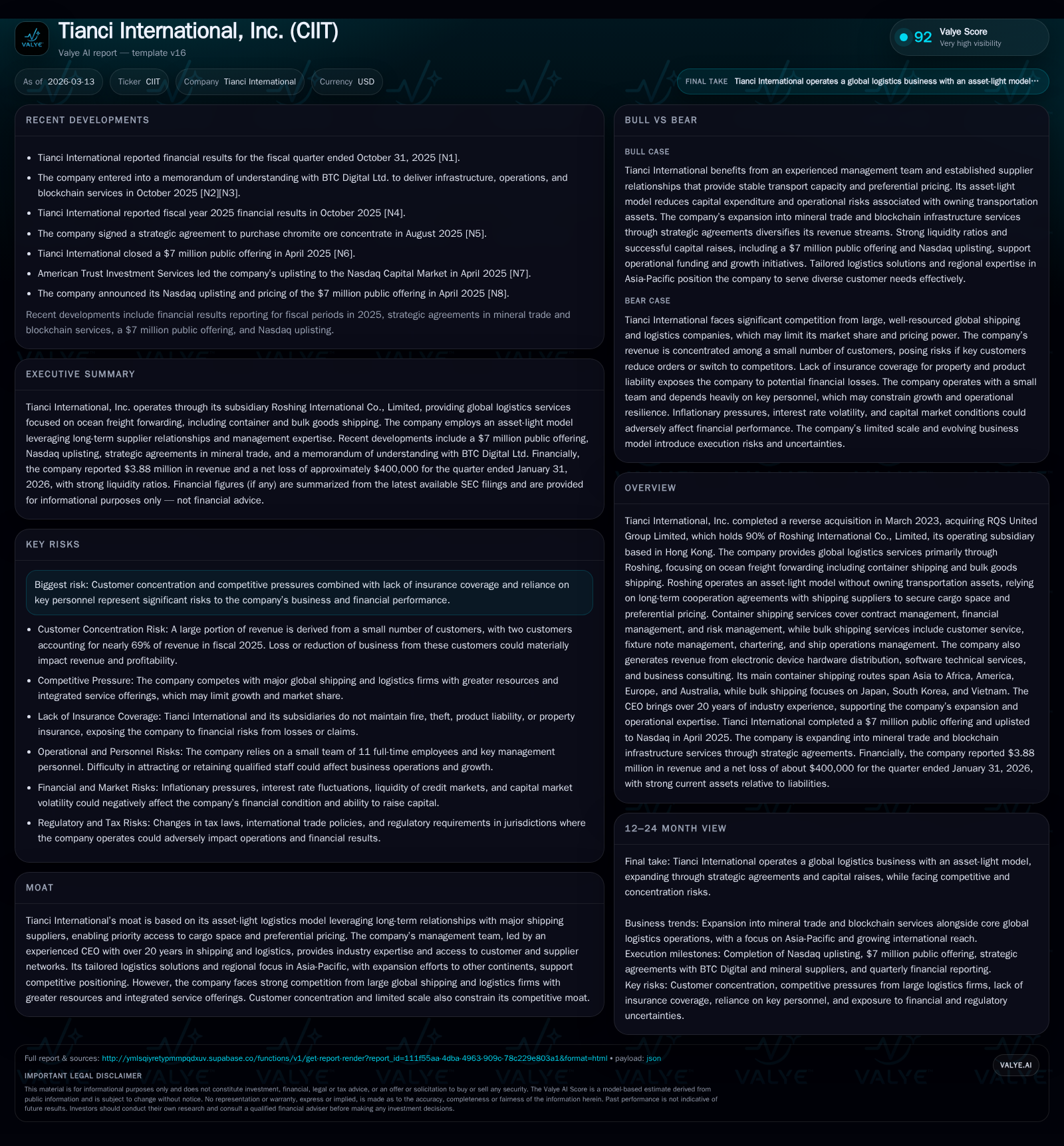

Tianci International’s Post-Acquisition Surge and Financial Strains Highlight Asset-Light Logistics Challenge

Tianci International transformed its scale through a 2023 reverse acquisition but continues grappling with profitability and liquidity issues inherent in its asset-light ocean freight forwarding model.

Since the March 2023 reverse acquisition of RQS United Group Limited and its operating subsidiary Roshing International, Tianci International has recorded rapid revenue growth from negligible levels to nearly $9.3 million by FY2025, reflecting a successful scaling of its global logistics services. However, this surge in top-line coincides with sustained operating losses exceeding $2.7 million and significantly negative operating cash flows indicative of ongoing financial pressure. The company’s asset-light model—relying on long-term contracts with shipping suppliers rather than vessel ownership—provides flexibility but exposes it to cargo space procurement risks and intense competition, compounded by high customer concentration where two clients represent nearly 70% of revenues. With no dividends or buybacks and a lean capital base, Tianci’s prospects hinge on expanding its customer base, diversifying operations into mineral trade, and navigating geopolitical and competitive challenges.

March 2023 Reverse Acquisition: Catalyzing Rapid Revenue Expansion

Tianci International's pivotal transformation occurred through the March 6, 2023 reverse acquisition of RQS United Group Limited (RQS United), which owns 90% of Roshing International Co., Limited (Roshing). Prior to this transaction, Tianci was essentially a shell corporation with no material operations ([S1]). This deal converted Tianci into an actionable player within the ocean freight forwarding niche globally.

This restructuring catalyzed an extraordinary jump in reported revenues: from zero in fiscal year (FY) 2022 to approximately $452K in FY2023, followed by a dramatic escalation to over $9.28 million by FY2025 ([F1]). Such growth evidences the initial success of Roshing's logistics services gaining commercial traction after being folded into Tianci.

Nonetheless, this scale-up was nascent as operational profitability remained elusive amidst efforts to grow market share rapidly.

Asset-Light Shipping Operations: Strategic Advantages and Industry Tailwinds

Roshing operates through an asset-light model that emphasizes chartering cargo space rather than owning vessels or trucks ([S1]). Specifically, Roshing charters container shipping cargo space under long-term cooperation agreements allowing preferential access and pricing terms. The operational scope includes contract management for container shipments as well as fixture note issuance and chartering for bulk goods transportation ([S4]).

The use of industry-specific workflows such as fixture note management exemplifies the operational intricacies—Roshing arranges ship bookings then facilitates cargo transport from load port to destination without direct asset ownership. This strategy reduces capital intensity but increases dependence on supplier relationships for reliable cargo space procurement.

The approach positions the company to flexibly respond to shifting global freight demands while minimizing fixed asset burdens inherent in shipping operators like Oldendorff Carriers or Pacific Basin ([S21]). However, it implicitly limits control over supply chain stability during periods of capacity scarcity or rate volatility ([S18]).

Customer Concentration Risks and Competitive Pressures in Global Ocean Freight

A key vulnerability for Tianci stems from pronounced customer concentration; two clients accounted for nearly 69% of all revenue in FY2025 ([S5]). During the prior year (FY2024), three customers contributed roughly 84%. This narrow client base magnifies exposure to single-customer demand shocks or contract non-renewals.

The ocean freight industry is notably competitive—with large multinational logistics firms exerting more extensive global networks and integrated service capabilities ([S4]). These competitors usually have deeper capital resources enabling fleet ownership or technology investments that can undercut asset-light players.

Furthermore, customers routinely solicit bids from multiple providers seeking price reductions and flexible contract terms which compress margins across the sector ([S15]). Thus, Tianci must balance aggressive customer retention efforts against sustainable pricing amid competition.

Profitability and Cash Flow Dynamics: Analyzing FY2025 Financial Performance

Despite rapid revenue growth (up 7.7% YoY from FY2024 to FY2025), Tianci experienced worsening profitability metrics last fiscal year ([F1]). Operating income swung sharply from a positive $168K in FY2024 to an operating loss surpassing $2.7 million in FY2025—a more than seventeen-fold worsening.

Net losses closely mirrored operating losses at approximately -$2.64 million suggesting limited ancillary income offsets ([F1]). Operating cash flow turned strongly negative at -$3.23 million in FY2025 after modestly positive levels in previous years, indicating that higher sales volume has yet to translate into healthy cash generation.

The approximate return on equity was -88.5% reflecting the deep net losses relative to shareholder capital of just under $3 million ([F1])—underscoring investor capital erosion amid growth efforts.

The disconnect between escalating revenues against deteriorating profits highlights operational cost structure challenges possibly linked to scaling complexities or pricing pressures discussed earlier.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | -3 | -3 | -3 | +7.7% | -4949.9% |

| 2024 | 9 | 0 | 0 | 0 | +1804.8% | +116.0% |

| 2023 | 0 | 0 | 0 | 0 | -37.7% | |

| 2022 | 0 | 0 | 0 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -88.5 |

| 2024 | 7.3 |

| 2023 | 125.9 |

| 2022 | 111.0 |

Source: SEC companyfacts cache [F1].

This table captures rapid revenue escalation juxtaposed with persistent net losses and operating cash outflows revealing financial stress amidst growth.

Capital Structure, Dividend Policy, and Shareholder Returns

Tianci maintains limited liquidity with nominal cash reserves around $13K as of January 31, 2023 ([F1]), although reported current assets exceed current liabilities by a wide margin yielding a strong current ratio near 35 ([F1],[S7]). This unusual discrepancy arises because current liabilities are modest (~$73K), possibly reflecting conservative liability management but limited working capital needs given small-scale operations outside traditional asset holdings.

No dividends have been declared historically nor have there been any stock buybacks indicating all available funds are retained for operational use or potential growth initiatives ([S19]). The company may require external financing beyond internal cash flow generation owing to continued free cash flow deficits visible in FY2025’s negative operating cash flow.

Potential dilutive equity raises or debt financing could be necessary—introducing investor dilution risks or leverage costs influencing future capital returns ([S7],[S19],[F1]). The absence of dividend distributions aligns with typical early-stage industrial service companies prioritizing reinvestment over yield.

Growth Drivers Ahead: New Ventures in Mineral Trade and Geographic Expansion

Tianci is proactively pursuing expansion beyond core freight forwarding through launching mineral trade operations specializing in metallurgical ores like chrome and manganese ([S1],[S14]). The company presently accumulates high-grade inventory strategically sourced from resource-rich regions intending vertically integrated supply chain solutions combining mining materials distribution with transport logistics.

Geographic expansion targets include South America and Africa focused on building collaborative partnerships regionally enhancing global reach ([S14]). These initiatives represent promising revenue diversification avenues but also carry execution risk considering Tianci has only eleven full-time employees constraining scalability at present ([S5],[S14]).

Environmental sustainability commitments are noted aiming at greener shipping practices aligning with increasing regulatory scrutiny within maritime sectors though practical impact remains nascent at this stage ([S14]).

Key Risks: Geopolitical Tensions, Competition, and Reliance on Key Personnel

Operating primarily outside the U.S., Tianci is exposed to macroeconomic uncertainties including tensions between major economies like U.S.-China relations plus regional conflicts impacting maritime trade routes ([S1],[S6],[S10]). Trade protectionism trends may increase costs or reduce shipment volumes adversely affecting demand.

Intense competition features prominently from incumbents with larger fleets and integrated logistics offerings who compete aggressively on price/service quality fronts threatening market share gains by Tianci’s asset-light platform ([S4],[S21]).

Risk is amplified by high customer concentration coupled with dependency on few suppliers for cargo space procurement; any loss or renegotiation could materially disrupt operations ([S5],[S18]). Additionally notable is lack of fire/theft/product liability insurance leaving the company economically vulnerable to unforeseen loss events ([S10],[S16]).

Human capital risk also looms given limited employee headcount placing critical reliance on senior management experience—particularly CEO Shufang Gao’s track record—as key success factors amid sector complexity ([S1],[S5],[S6]).

What Investors Should Monitor: Milestones and Potential Catalysts

Absent explicit forward guidance from management publicly disclosed up to now ([N/a]), near- to medium-term outlook hinges on:

- Diversification reducing customer concentration below current dominant two-client threshold supporting revenue resilience;

- Improvement turning negative operating cash flows toward breakeven evidencing scalable business economics;

- Successful launch and integration of mineral trading lines advancing vertical diversification;

- Expansion progress into targeted new geographies improving service network breadth;

- Contractual renegotiations exhibiting ability to pass-through inflation-driven cost increases maintaining margin integrity;

- Corporate governance enhancements including risk mitigation around insurance coverage adoption.

Progress along these vectors would signal maturation from nascent post-acquisition scaling toward sustainable profitability. Conversely any setbacks—especially client attrition or worsening liquidity metrics—could heighten operational vulnerabilities uniformly noted within SEC filings [S#].

This analysis relies solely on information derived from verified SEC filings through July 31, 2025 and company disclosures as referenced; no speculative forecasts or market opinions are offered.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments