Cassava Sciences Navigates Challenges While Advancing Filamin A-Targeted CNS Therapy

Cassava Sciences focuses on its filamin A modulator simufilam amid clinical, manufacturing, and legal challenges with a lean financial position.

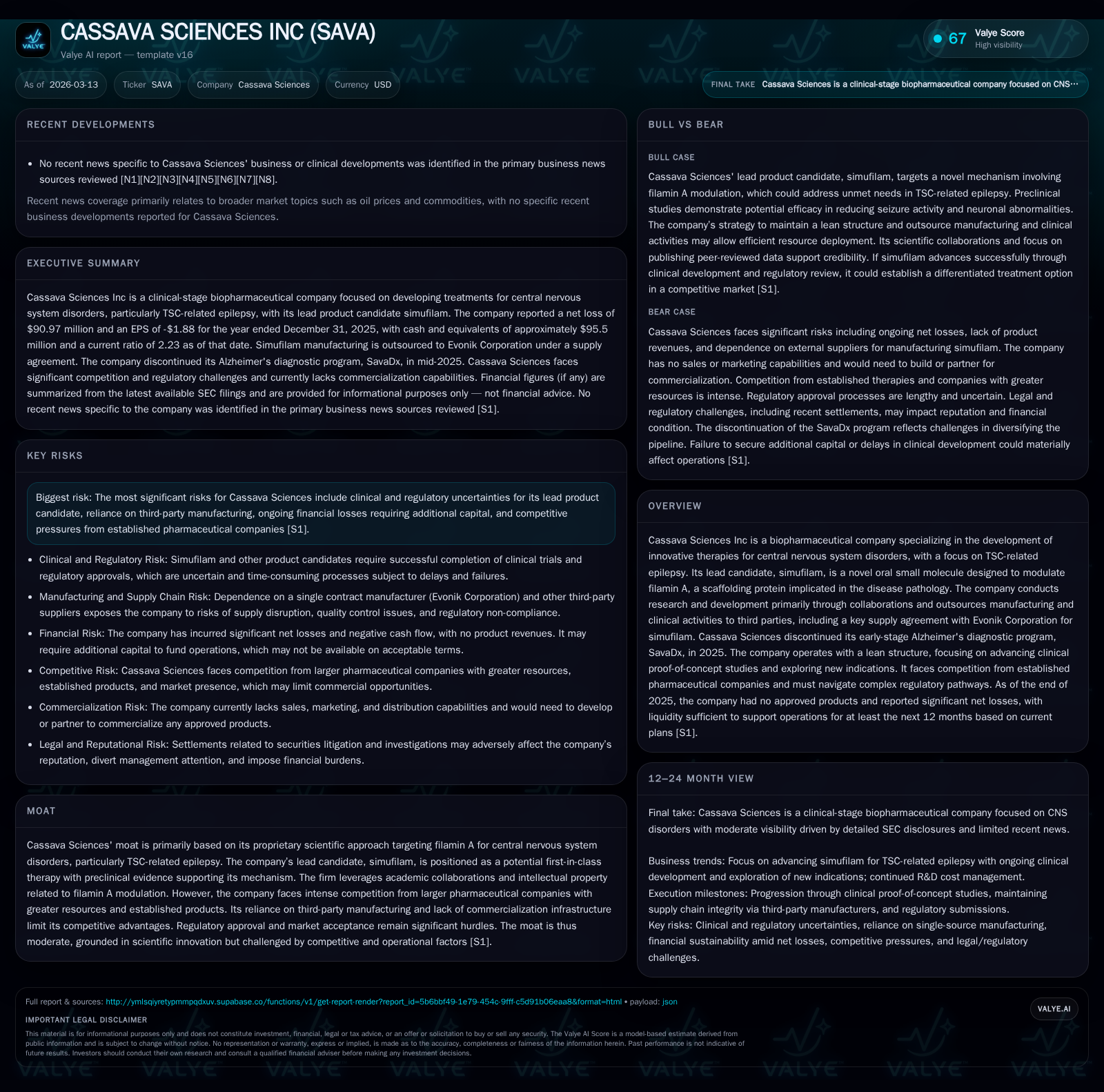

Cassava Sciences is a clinical-stage biopharmaceutical company developing treatments for central nervous system disorders, chiefly TSC-related epilepsy, through simufilam, an oral small molecule that modulates filamin A. The company has generated flat revenue since 2013 and sustained operating losses reflecting its development focus and discontinued Alzheimer’s diagnostic program. Future prospects depend on clinical validation of simufilam and expansion of indications while managing regulatory, manufacturing, and legal risks. Cassava operates with a lean structure relying on third-party suppliers like Evonik Industries AG and faces ongoing legal settlements affecting its reputation and finances.

Company Overview and Historical Performance

Cassava Sciences Inc is a clinical-stage biopharmaceutical company focused on developing therapies for central nervous system (CNS) disorders, primarily tuberous sclerosis complex (TSC)-related epilepsy. Its lead candidate, simufilam, is an oral small molecule designed to modulate filamin A, a scaffolding protein involved in neuronal protein interactions implicated in disease pathology [S1].

The company has reported flat revenue around $35.2 million as of 2013 with no subsequent growth reflected in available data [F1]. This static revenue underscores its pre-commercial status focused on research and development rather than product sales. Operating income worsened from -$80 million in 2022 to -$141 million in 2024 before improving to -$95 million by the end of 2025. Net losses similarly fluctuated, reaching -$243 million in 2024 then moderating to approximately -$91 million in 2025. These results reflect sustained investment toward advancing simufilam through preclinical and early clinical phases rather than generating positive cash flows from marketed products [F1].

Operating cash flow remained negative but improved by over 70% year-over-year to an outflow of about -$32.3 million in 2025. Capital expenditures were minimal at approximately $0.58 million for the same period, consistent with Cassava's strategy of outsourcing manufacturing and infrastructure needs rather than internal buildout [F1]. The resulting free cash flow remains negative.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -91 | -32 | -95 | 1 | -273.7% |

| 2024 | -24 | -117 | -141 | 0 | +75.0% |

| 2023 | -97 | -82 | -106 | 0 | -27.5% |

| 2022 | -76 | -78 | -80 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -33 | -122.3 |

| 2024 | -117 | -16.7 |

| 2023 | -82 | -70.7 |

| 2022 | -80 | -33.5 |

Source: SEC companyfacts cache [F1].

Revenue stable circa FY2012-FY2013 per available data [F1].

Scientific Rationale and Product Development

Simufilam is Cassava's primary therapeutic candidate targeting filamin A modulation to address TSC-related epilepsy—a condition marked by elevated filamin A levels combined with mTOR pathway activation leading to seizures and neuronal abnormalities [S1]. Preclinical mouse models showed that both genetic normalization and pharmacological targeting of filamin A reduced seizure activity independently of mTOR signaling, supporting the biological rationale for clinical development.

The company explores additional CNS indications where filamin A may play a role in neurodegeneration or neuroinflammation but has not publicly disclosed extensive pipeline expansions beyond this core focus [S1]. Artificial intelligence tools are being integrated into research workflows to improve productivity and data analytics.

In mid-2025, Cassava discontinued SavaDx, an early-stage Alzheimer’s blood-based diagnostic program representing less than one percent of research expenditure historically, reflecting a strategic shift exclusively toward therapeutics [S1].

Manufacturing and Operational Model

Cassava operates with a lean organizational structure lacking internal manufacturing or commercialization functions. The company relies heavily on third-party contractors for supply chain activities including drug substance production, formulation, packaging, labeling, and distribution coordination [S1].

Evonik Industries AG serves as the exclusive supplier of clinical-grade simufilam under contract manufacturing arrangements critical for ongoing trials [S7]. This dependency introduces risks related to potential supply disruptions or cost increases that could delay development timelines or increase expenses.

Regulatory Compliance and Legal Environment

The company faces complex regulatory requirements encompassing FDA approval processes as well as compliance with federal healthcare laws including anti-kickback statutes, false claims acts, HIPAA privacy rules, pricing transparency mandates such as the Sunshine Act, among others . Noncompliance risks include fines, penalties, exclusion from government healthcare programs, and reputational damage.

In recent years, Cassava settled significant legal matters including:

- A $40 million civil monetary penalty paid in late 2024 resolving an SEC investigation related to Phase 2b study disclosures,

- A $31.25 million settlement resolving securities litigation linked to disclosure issues.

These settlements have materially impacted financial resources and corporate reputation while requiring ongoing management attention amidst continued litigation exposure including shareholder derivative lawsuits and intellectual property disputes common within biotech sectors [S6][S7][S10][S20][S24][S29].

Competitive Landscape and Industry Challenges

While filamin A modulation offers a first-in-class approach for CNS disorders like TSC-related epilepsy, Cassava competes against larger pharmaceutical companies possessing greater resources and established commercial infrastructure which could limit market penetration upon approval.

Regulatory scrutiny remains intense due to safety concerns inherent in CNS drug development requiring extensive late-stage trials and possible post-market obligations that may increase costs post-launch. Pricing pressures are also expected under U.S. government programs influenced by legislation such as the Inflation Reduction Act potentially compressing margins even if commercialized successfully [S13].

Financial Position and Capital Allocation

As of December 31, 2025, Cassava held approximately $95.5 million in cash and equivalents compared with current liabilities near $43.8 million producing a current ratio above two times—indicating adequate short-term liquidity given the absence of revenues from marketed products at this stage [F1].

Equity declined from $146 million at end-2024 to about $74 million at end-2025 reflecting cumulative net losses impacting shareholders’ capital base during continued operational funding needs.

No dividends or share repurchases have been indicated or feasible given persistent net losses (approximate return on equity at -122%). Capital expenditures remain minimal consistent with outsourcing reliance allowing capital focus toward clinical development rather than fixed asset investments [F1].

Future funding requirements will depend heavily on achieving clinical milestones or securing partnerships; failure to do so may increase dilution risk absent near-term commercial revenues or licensing income.

Outlook Considerations

Growth prospects hinge on progressing simufilam through pivotal trials demonstrating efficacy and safety sufficient for regulatory submissions targeting TSC-related epilepsy initially with potential indication expansions leveraging filamin A biology.

Key forward-looking factors include:

- Upcoming clinical trial readouts,

- Expansion into additional CNS conditions,

- Stability of supply chain partnerships,

- Resolution or management of ongoing litigations,

- Reimbursement environment developments,

- Potential strategic alliances addressing commercialization capabilities.

Given prior legal settlements impacting finances alongside competitive pressures from larger firms developing CNS therapies, Cassava faces a challenging path requiring rigorous execution across multiple operational dimensions.

Conclusion

Cassava Sciences presents a scientifically innovative approach targeting filamin A modulation for difficult-to-treat neurological diseases supported by preclinical evidence but contends with significant developmental financial legal risks compounded by lack of internal commercialization infrastructure requiring heavy reliance on external partners. Scientific innovation forms the core value proposition while regulatory complexities reimbursement challenges competitive dynamics litigation exposure all weigh on future viability. Monitoring upcoming clinical milestones alongside operational risk management will be essential metrics defining Cassava’s evolution from investigational biotech entity toward potential therapeutic commercial stage enterprise.

This analysis synthesizes publicly available SEC filings alongside financial disclosures without investment advice or price forecasts. Investors should consider biopharma sector risks including lengthy development timelines capital intensity regulatory uncertainties competition plus company-specific litigations when forming views.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments