Hilltop Holdings Inc.: A Diversified Financial Services Company with a Dual Focus on Banking and Broker-Dealer Operations

Hilltop Holdings combines Texas-based community banking with a national broker-dealer platform to deliver diversified financial services and growth opportunities.

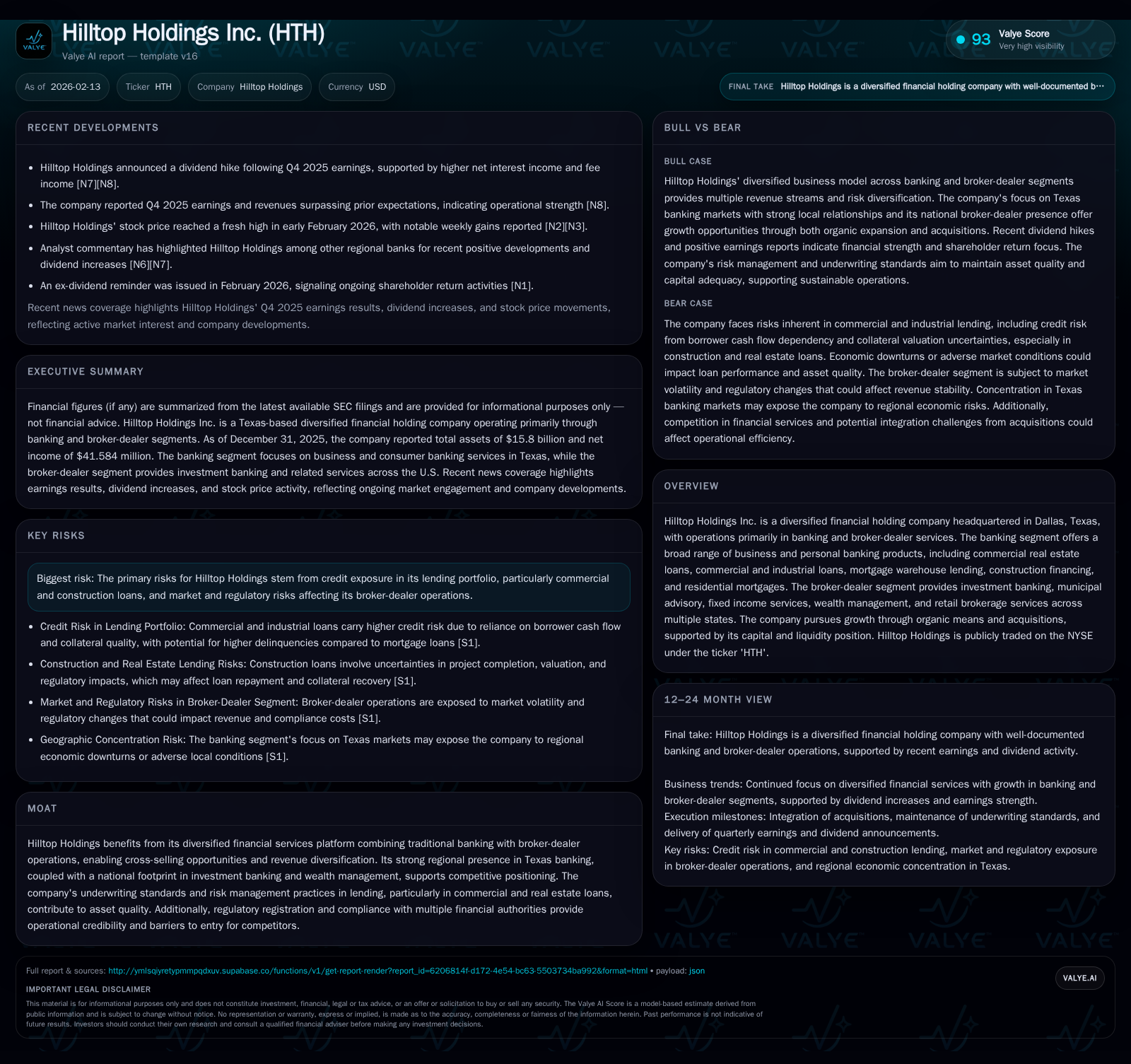

Hilltop Holdings Inc. (NYSE: HTH) operates a diverse financial services platform centered on banking and broker-dealer operations, primarily serving Texas with nationwide reach in investment banking and wealth management. The combination supports cross-selling, revenue diversification, and competitive advantage through regional strength and underwriting discipline. Recent earnings reports indicate robust net interest income and fee income growth, alongside a dividend increase that highlights management’s confidence in the balance sheet and earnings trajectory. Key risks include credit exposure in commercial real estate and construction loans, regulatory compliance burdens, and cybersecurity threats.

Company Overview

Hilltop Holdings Inc., traded on the NYSE as HTH, is a diversified financial holding company headquartered in Dallas, Texas. It operates principally through two primary divisions: its Texas-centric banking operation known as PlainsCapital Bank (PCC), and its Securities Holdings broker-dealer platform offering national investment banking and wealth management services. The firm’s business model balances community banking roots with sophisticated capital markets activities aiming for revenue stability and growth.

At the end of 2025, Hilltop reported consolidated assets of roughly $15.8 billion with deposits near $10.9 billion and loan balances totaling approximately $9.2 billion [S1]. This represents a sizeable regional bank with national reach through its broker-dealer subsidiaries.

Business Segments

Banking Segment

Hilltop’s banking operations provide broad product coverage including commercial real estate loans—a historically lucrative but cyclical segment—commercial & industrial loans serving local businesses across various industries, mortgage warehouse lending supporting homebuilder financing needs, construction loans which entail higher underwriting risk due to project execution uncertainty, and residential mortgages often sold into secondary markets.

PlainsCapital Bank is well entrenched within Texas markets offering both business deposit accounts and personal banking products. The bank’s geographic concentration necessitates vigilance regarding state economic cycles but facilitates deeper client relationships enabling cross-selling opportunities of complementary services.

Broker-Dealer Segment

The broker-dealer unit operates nationally delivering a comprehensive suite of investment banking activities: municipal advisory mandates on debt issuance; taxable and tax-exempt fixed-income sales & trading; securities underwriting including structured finance; retail brokerage; securities clearing; lending platforms for securities collateralized financing; plus wealth management solutions for high-net-worth clients.

This segment provides critical fee-based revenue streams that are less interest rate sensitive compared to core lending activities. Through this diversified non-interest income base Hilltop can temper volatility inherent in traditional banking revenues.

Strategic Positioning & Competitive Moat

Hilltop Holdings benefits significantly from operating across these complementary financial sectors creating a hybrid platform difficult for specialized competitors to replicate fully [Valye Report excerpt]. Cross-selling between deposit-taking clients and brokerage/investment clients strengthens client retention while broadening revenue per customer.

Its strong foothold in Texas—a dynamic economy with robust energy, technology, healthcare, and real estate sectors—also contributes materially to earnings consistency while enabling growth strategies tailored locally but scalable nationally through its Securities Holdings arm.

Underwriting discipline remains a cornerstone of Hilltop’s risk management framework. The company maintains rigorous evaluation of loan creditworthiness with adjustments to allowance for credit losses based on detailed portfolio performance analytics incorporating economic forecasts [S1]. This careful calibration helps mitigate losses though it cannot eliminate credit risk totally given economic cyclicality.

Recent Financial Performance Highlights

Hilltop recently announced Q4 2025 results that beat analyst expectations on both earnings and revenues [N1][N2][N3][N4]. Key drivers included improved net interest income owing to higher loan yields amidst rising rates coupled with increased fee income stemming from enhanced broker-dealer activity.

The company also raised its dividend reflecting confidence in sustainable cash flow generation [N2][N6]. Market commentary has noted Hilltop as a strong momentum stock partly due to this fundamental performance trajectory [N7][N11][N14].

Industry Context & Market Environment

The financial services sector continues to navigate complexities ranging from tightening monetary policy affecting credit demand and pricing to evolving regulatory frameworks imposing compliance costs particularly on broker-dealers managing client asset protections. Concurrently technology advances underpin competitive shifts including growing fintech participation challenging traditional banking models while elevating cybersecurity importance.

Regional banks like Hilltop face unique challenges balancing growth ambitions against concentrated geographic exposures while competing for deposits amidst high rates offered by larger institutions or alternative deposit platforms.

Risk Factors Summary

Per the latest annual SEC filings [S1], Hilltop’s principal risks derive from:

- Credit Risk: Especially from commercial real estate loans which remain sensitive to economic downturns or regional market disruptions. Construction loans bear additional project-specific uncertainties leading to potential loss severity if defaults occur.

- Operational Risks: Including evolving cyber threats due to heavy reliance on digital infrastructure potentially leading to customer data breaches or service interruptions.

- Regulatory Risks: Compliance with banking regulators and securities authorities demands substantial resources; adverse regulatory actions could impact operations or result in fines.

- Market Risk: Broker-dealer revenues fluctuate with capital markets conditions; volatility may depress underwriting activity or trading volumes.

- Reputational Risk: Negative publicity from operational failures or market shocks could affect client trust impacting deposits or brokerage relationships.

Management endeavors to actively monitor these factors deploying robust controls but acknowledges the inherent unpredictability within financial markets subjects the business to periodic pressures.

Outlook Considerations (Analysis)

Looking forward into 2026 and beyond (analysis), Hilltop appears positioned to leverage its dual-segment approach benefiting from rising rates enhancing net interest margins while fee-based revenues offer ballast against macroeconomic headwinds. Organic growth supplemented by targeted acquisitions remains the stated strategy provided capital metrics remain supportive.

However, balance sheet quality will require continued vigilance particularly within construction lending where underwriting prudence must offset borrower default risk should real estate development slow materially. Regulatory developments could impose incremental costs or operational constraints necessitating agility. Finally technological investments aimed at reinforcing cybersecurity defenses constitute an ongoing imperative given increasing attack sophistication.

Conclusion

Hilltop Holdings exemplifies a moderate-sized diversified financial holding company combining regional community banking strength with nationwide broker-dealer capabilities. Its balanced model fosters revenue diversification supporting resilience amid shifting financial conditions while posing challenges typical of mid-market banks contending with credit concentration risks and multi-jurisdictional regulatory requirements. Recent results affirm the company's operational execution though attendant risks underscore the importance of continual credit discipline and operational excellence.

This report was prepared solely for informational purposes without any express or implied investment advice. Users should consider additional sources before making decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments