Hertz Global Holdings Rebounds with Strategic Financing and Fleet Management

Examining Hertz's financial engineering and operational initiatives amid a revenue contraction and evolving market challenges.

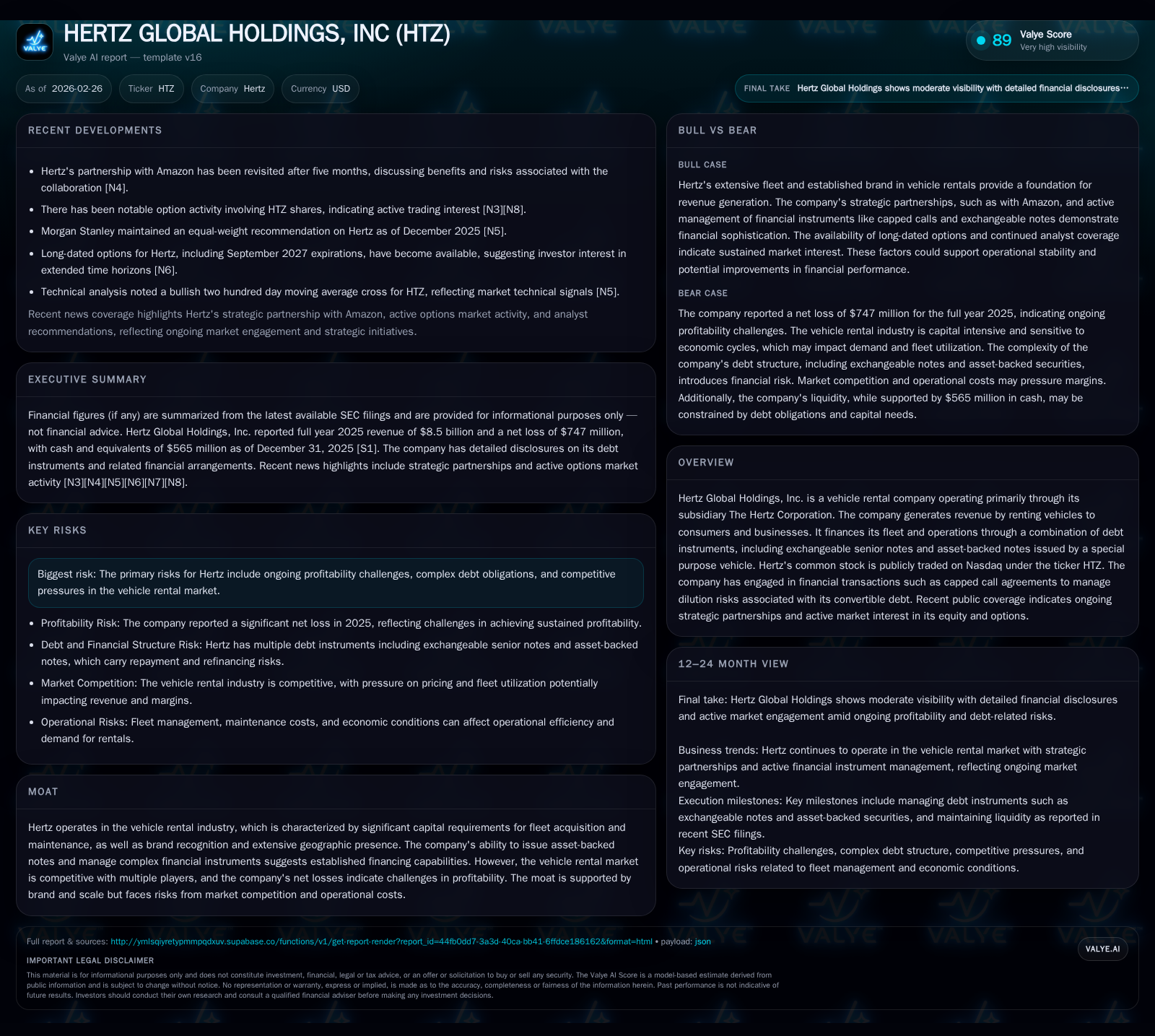

Hertz Global Holdings reported a 6% decline in revenue to $8.5 billion for FY2025 alongside large but reduced net losses, signaling an uneven profitability trajectory. Operationally, the company is leveraging fleet management efficiencies and strategic partnerships, including with Amazon, to drive performance improvements. Detailed refinements in capital structure, especially via exchangeable senior notes and asset-backed securities through HVF III, underscore a focus on managing liquidity and fleet renewal costs. Capped call agreements serve as critical tools mitigating dilution risk from convertible debt issuance. Despite strong operating cash flow and free cash generation, Hertz refrained from dividends or buybacks, likely reflecting cautious capital allocation given a negative equity position. Future growth hinges on partnership synergy and market dynamics, while ongoing leverage and competitive pressures remain key risks.

Revenue Trends and Profitability: An Uneven Path

Hertz's revenue slid approximately 6% year-over-year from $9.05 billion in FY2024 to $8.5 billion in FY2025 [F1], depicting softness in demand or pricing pressures within the vehicle rental industry. Despite this top-line contraction, the company managed a marked improvement in its bottom line compared to the previous fiscal year: net losses narrowed significantly from -$2.86 billion to -$747 million [F1]. This shift underscores an uneven path toward profitability — significant losses persist albeit less severe, suggestive of cost controls or operational efficiency gains partially offsetting diminished revenue.

Operating cash flow also demonstrated resilience at $1.625 billion for FY2025 [F1], down from $2.22 billion the prior year but still strong relative to the negative earnings backdrop—reflecting effective working capital management or non-cash charges impacting net income.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.5 | -0.7 | 1.6 | 13 | -6.0% | +73.9% |

| 2024 | 9.0 | -2.9 | 2.2 | 3 | -3.4% | -564.6% |

| 2023 | 9.4 | 0.6 | 2.5 | 16 | +7.9% | -70.1% |

| 2022 | 8.7 | 2.1 | 2.5 | 23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 0.0 | 1.6 | 162.7 |

| 2024 | 0.0 | 2.2 | -1870.6 |

| 2023 | 0.3 | 2.5 | |

| 2022 | 2.5 | 2.5 |

Source: SEC companyfacts cache [F1].

Amid persistently negative earnings but improving trends, Hertz’s performance portrays a hybrid struggle between market headwinds and operational recovery efforts.

Operational Drivers Behind the Recent Performance Shift

Hertz's operational narrative centers on optimizing fleet utilization—the ratio of rented vehicles versus total inventory—and enhancing margins across its geography-spanning locations [S6][S10][S11]. The company benefits from broad geographic reach which amplifies brand recognition yet necessitates localized fleet mix adjustments to meet variable demand patterns.

A notable driver includes strategic partnerships such as the multi-month collaboration with Amazon highlighted in recent market commentary [N3]. This alliance aims to integrate innovative vehicle offerings into last-mile delivery solutions, potentially diversifying Hertz's revenue streams beyond classic consumer rentals.

Higher utilization rates coupled with enhanced location-level margin contributions signify gradual recovery momentum even as broader travel demand fluctuates.

Capital Structure Refined: Navigating Complex Debt Instruments

A defining characteristic of Hertz's financial position is sophisticated capital structuring tailored to support fleet acquisition while managing liquidity.

In late September 2025, Hertz issued $425 million aggregate principal amount of 5.500% Exchangeable Senior Notes due in 2030 with an initial exchange price set at roughly $9.24 per share — a ~32% premium over prevailing stock prices at issuance [S16][S19][S21]. These notes are senior unsecured obligations guaranteed by subsidiaries and offer conversion flexibility under designated conditions.

Complementing this are asset-backed notes issued by Hertz Vehicle Financing III LLC (HVF III), a special-purpose vehicle administering fleet financing securitizations [S8][S9][S14][S18]. HVF III issued multi-class tranches totaling approximately $1 billion across series 2025-5 and 2025-6 with coupon rates ranging from ~4.6% to over 8%, reflecting tranche seniority layering.

These securitized notes have staggered amortization schedules beginning between December 2028 to December 2030 unless triggered earlier by amortization events such as covenant breaches or insufficient asset coverage [S9]. Such events could force accelerated principal repayment and require active monitoring.

This blend of corporate senior unsecured debt with structured finance instruments exemplifies Hertz’s approach to balancing fleet capital needs against leverage constraints.

Capped Call Transactions and Dilution Management

To contain dilution risks stemming from convertible debt issuance, Hertz engaged in capped call agreements concurrently with note offerings in September 2025 [S15].

These derivatives effectively impose a ceiling on potential dilution by compensating for common stock issuance upon note conversion through cash settlements capped at preset strike prices (~$13.94 initially).

Such capped calls protect shareholder equity values without modifying underlying debt terms — a nuanced layer of financial engineering contributing to Hertz’s holistic capital strategy.

Fleet Financing via Asset-Backed Notes: Strategic Fleet Renewal

HVF III’s asset-backed securities function as critical enablers of Hertz’s fleet renewal — funding new vehicle acquisitions or refinancing existing assets under leases [S8][S9]. Proceeds from Series 2025 Notes were partly deployed to repay prior variable funding rental car asset-backed notes while leaving capacity for continued fleet investments.

However, these arrangements incorporate amortization event clauses that can trigger early mandatory repayments if liquidity or asset coverage falters — potentially resulting in forced vehicle sales by HVF III administrators to satisfy note holders [S8]. Thus, while providing financing scalability, they also introduce obligations requiring careful covenant compliance oversight.

Future Growth Catalysts Anchored on Partnerships and Market Dynamics

Growth prospects rest on unlocking partnership synergies (e.g., Amazon collaboration) that may yield incremental revenue diversification beyond conventional rental streams [N3].

Additional drivers are technical market signals: bullish two-hundred-day moving average crossovers noted in January 2026 indicate investor optimism [N6], complemented by expanding options availability extending through September 2027 enhancing hedging/liquidity profiles [N7].

Recent upgrades by analysts further underscore positive sentiment rationales grounded in operational improvements and financial restructuring progress [N4]. Together these hint at latent growth potential if macroeconomic conditions hold favorably.

Monitoring Forward Indicators: What Investors Should Watch

Key performance indicators warranting attention include pace of revenue recovery relative to peers, adherence to amortization schedules on securitized notes reducing credit risk exposure, and operational KPIs like incremental changes in utilization rates at core U.S. markets [S11].

Market observers should also track option volume spikes that reveal sentiment shifts—the active trading noted on February 5th signals evolving views on HTZ shares’ volatility profile [N5]. External economic indicators influencing travel patterns will similarly impact fundamental outlooks.

Assessing Capital Allocation: Cash Flow Prioritized Over Dividends or Buybacks

Despite sizable operating cash flows ($1.625 billion after modest capex spend) for FY2025 [F1], Hertz has abstained from paying dividends or conducting share repurchases recently — a prudent stance given its negative book equity (-$459 million) indicating retained earnings deficits and leveraged balance sheet positions.

With capex notably low ($13 million), free cash flow generation remains strong ($1.61 billion), favoring liquidity retention for debt servicing or strategic investments rather than distributive returns [F1]. The approximate return on equity calculation yields an anomalous figure due to negative equity base; thus traditional ROE metrics are distorted amid leverage complexities.

Risk Landscape: Balancing Leverage Against Competitive Pressures

Primary risks intertwine high leverage burdens—maturing debt concentrations including near-term senior note pay downs—and persistent net losses despite billions in annual revenues [F1][S4][S7]. Failure to meet amortization event covenants could precipitate accelerated repayment scenarios exposing refinancing challenges.

Concurrently, Hertz operates within an intensely competitive vehicle rental industry where brand recognition and geographic presence compete against emerging mobility alternatives impacting demand elasticity and margin structures.

Operational cost inflation pressures complement cyclical travel volume uncertainties as headwinds constraining sustainable profitability trajectories—all necessitating vigilant financial discipline alongside agile strategic positioning.

This report synthesizes publicly available SEC filings and recent news disclosures up to February 26, 2026 reflecting factual company data without recommending any investment course or valuation judgment.Legal risk disclosures, historical financial data points, and structured finance details presented herein align with official Hertz Global Holdings submissions filed via SEC forms referenced accordingly.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments