iBio, Inc.: Strategic Antibody Platform and Capital Strength Paving Path for Novel Obesity Therapeutics

Amid intense biotech competition and clinical-stage uncertainty, iBio’s proprietary antibody technology and collaborations mark a critical juncture.

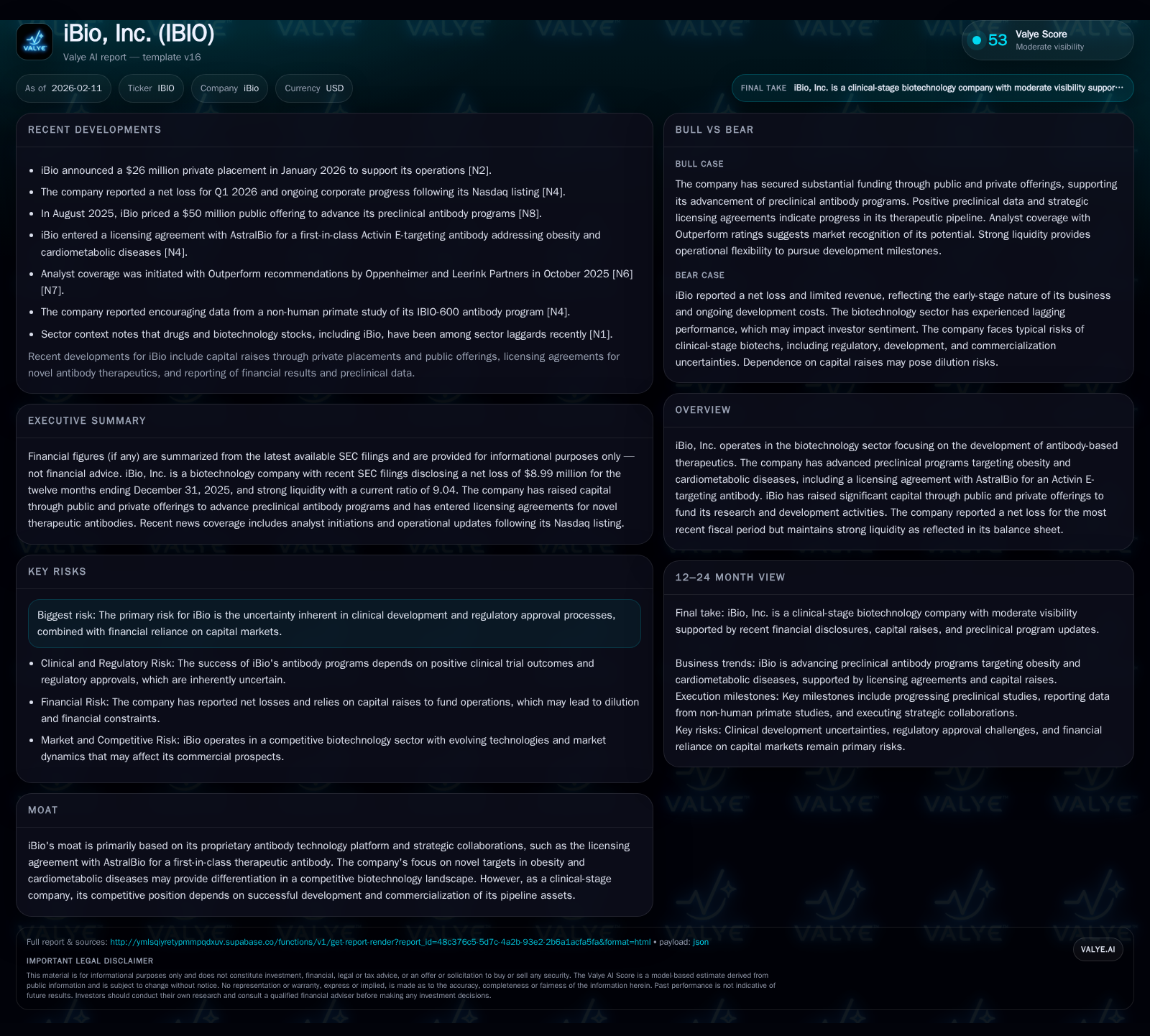

iBio, Inc. stands at an inflection point driven by its proprietary antibody platform focused on obesity and cardiometabolic diseases, underpinned by an exclusive licensing agreement with AstralBio. The company’s recent $26 million private placement and previous fundraises have fortified its liquidity, supporting continued R&D despite ongoing net losses. As a clinical-stage player, iBio faces customary regulatory and development hurdles, yet upcoming milestones and pipeline advances could significantly impact its competitive positioning in the biotechnology sector.

A Platform Built for Tomorrow’s Therapeutics: iBio’s Antibody Technology

iBio’s core competency lies in its proprietary antibody technology platform designed to address unmet medical needs within obesity and cardiometabolic disease spaces. This focus taps into growing global health concerns where novel biologic therapies can disrupt traditional treatment paradigms. The company’s moat is defensible largely through this proprietary technology combined with targeted pipeline initiatives centered on antibodies—a modality with established clinical relevance but requiring sophisticated specificity to stand out.

What distinguishes iBio is its strategic targeting of inflammatory pathways implicated in metabolic disorders, notably through antibodies that explore less saturated mechanisms compared to standard approaches. In a sector densely populated with companies chasing broadly defined cardiovascular or metabolic pathways, this platform offers differentiated scientific angles. However, the success of such specialized antibody therapeutics hinges critically on translating preclinical promise into clinical efficacy—a hurdle that continues to define competitive positioning at this stage [F1][valye_report_excerpt].

Partnerships in Innovation: The AstralBio Licensing Agreement's Strategic Role

iBio’s exclusive license agreement with AstralBio represents a pivotal strategic alliance underpinning its pipeline expansion. By acquiring rights to an antibody targeting Activin E—a protein linked mechanistically to energy metabolism—iBio aims to pioneer a first-in-class therapy addressing obesity-related pathology. This form of collaboration leverages complementary expertise while mitigating early-stage discovery risks inherent in wholly internal programs.

From the filings perspective, this arrangement not only grants access to cutting-edge intellectual property but also signals validation from external scientific stakeholders. Such deals often serve dual purposes: accelerating development timelines and enhancing investor confidence in the pipeline's novelty and commercial potential. The exclusivity around this Activin E-targeting asset differentiates iBio within biotech’s therapeutic landscape increasingly wary of commoditized approaches [valye_report_excerpt][S2].

Does this partnership position iBio uniquely enough to command earlier adoption or preferential investment interest in obesity therapeutics? The answer depends on subsequent clinical progress but sets an important foundation.

Capitalizing Progress: How Recent Fundraisings Bolster Development Pipelines

In January 2026, iBio announced a $26 million private placement that augmented its existing capital base—an essential move given the high cash burn typical of clinical-stage biotechs [N4]. This infusion follows prior public and private offerings designed explicitly to finance expanded research efforts and operational needs.

Assessing the balance sheet reveals cash and equivalents totaling approximately $28.7 million against current liabilities near $5.9 million, translating into a current ratio exceeding 9—indicative of prudent liquidity management amidst intensive R&D expenditure [F1][S2]. This financial posture provides crucial runway extension potentially allowing uninterrupted progression through early development hurdles.

Such capital strategies underscore management’s commitment to sustaining momentum without overly diluting shareholder value or risking liquidity shortfalls. For companies like iBio, early financial robustness is as vital as scientific advances since funding gaps can derail promising platforms irreversibly.

Navigating the Clinical-Stage Gauntlet: Risks and Rewards Explored

Clinical development is inherently uncertain—a reality reflected explicitly in the risk disclosures emphasized by iBio. Success depends not only on scientifically validating novel targets but securing regulatory approval amid complex safety profiling requirements [valye_report_excerpt].

Moreover, reliance on continuous capital raises introduces vulnerability to market sentiment fluctuations. Biotech investors often exhibit cyclical enthusiasm; thus, timing financing rounds relative to clinical milestones is critical. Failures or delays can suppress stock valuations sharply, while positive data may unlock substantial upside.

The reward side lies in first-mover advantages within niche therapeutics addressing widespread chronic conditions like obesity—a field actively seeking innovative solutions beyond lifestyle management or generic pharmacotherapy.

How effectively iBio manages trial design, regulatory interactions, and milestone delivery will strongly dictate whether it converts platform promise into commercial reality.

Fiscal Health Under the Microscope: Analyzing Liquidity and Loss Trends

iBio's fiscal reports through late 2025 detail a net loss nearing $9 million over the year—typical for a pre-revenue biotech investing heavily in R&D [F1]. Yet, juxtaposed against these losses is a notably strong liquidity profile with cash reserves comfortably above immediate liabilities.

Such positioning affords operational resilience but requires sustained cash flow management vigilance lest expenditures outpace available funding during potentially protracted development phases [S2]. The current ratio above 9 implies the company could cover short-term obligations multiple times over; however, continuous fundraising remains necessary until product commercialization or licensing revenue streams materialize.

This dual reality demands investors pay close attention not just to headline losses but underlying cash burn trajectories relative to pipeline advancement milestones.

Market Performance Amid Sector Volatility: Positioning Within Biotech Peers

iBio operates in an environment marked by recent biotechnology sector volatility with notable laggards among drug developers affecting overall investor confidence [N3]. Against this backdrop, iBio is positioned for Q2 earnings expectations modestly above consensus estimates indicating market anticipation of manageable operational costs or developmental progress [N2].

Comparatively smaller float sizes and emerging pipelines typify firms like iBio making them vulnerable but also potentially attractive upon delivery of positive catalysts. Sector-wide dynamics such as advances in genetic medicine or shifts towards metabolic disease treatments may exert tailwinds but require alignment with internal execution.

Will upcoming financial disclosures reinforce growth narratives or highlight susceptibility under current macroeconomic pressures? Monitoring such reports alongside sector indices will clarify relative investor sentiment.

Looking Ahead: Milestones That Will Define iBio’s Trajectory

iBio has several key near-term objectives capable of reshaping its strategic storyline. Chief among these are data readouts from ongoing preclinical evaluations for its Activin E-targeting antibody alongside announcements about additional collaborations or licensing deals that enhance pipeline breadth or depth [valye_report_excerpt][N2].

Such milestones serve as inflection points where validation of science translates into tangible corporate value enhancement or alternatively exposes developmental fragility. Operational updates around capital deployment efficacy or regulatory submissions will further inform feasibility of scaling innovation towards market introduction.

Investors and stakeholders alike should focus on these events as markers defining whether iBio capitalizes on its proprietary platform advantage decisively or encounters setbacks common within clinical-stage biotech endeavors.

Investor Considerations: Balancing Opportunity Against Regulatory Uncertainty

iBio exemplifies quintessential clinical-stage biotechnology investment complexities: a blend of high scientific potential counterweighted by developmental and financial risks intrinsic to novel therapeutic creation [valye_report_excerpt][N2][S2].

Prudent stakeholder evaluation involves assessing how well management mitigates these risks via strong partnerships (e.g., AstralBio licensing), disciplined capital strategies (recent fundraises), and clear milestone-driven operations. Additionally, understanding sector context including peer trajectories and macroeconomic influences enhances decision frameworks without prescribing investment action.

Ultimately, the company's prospects hinge on execution amidst uncertainty—the degree to which ambitious innovation can be matched by robust science translation will determine if iBio moves beyond promising pipeline status toward sustainable therapeutic commercialization.

Disclaimer: This analysis is intended solely for informational purposes reflecting publicly available data as of early 2026 and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments