ImmunityBio’s Revenue Surge and EU Approvals Challenge Capital Intensity and Profitability

The company’s substantial ANKTIVA sales growth and expanded European marketing authorization test its capacity to convert innovation into sustainable profits amid ongoing losses.

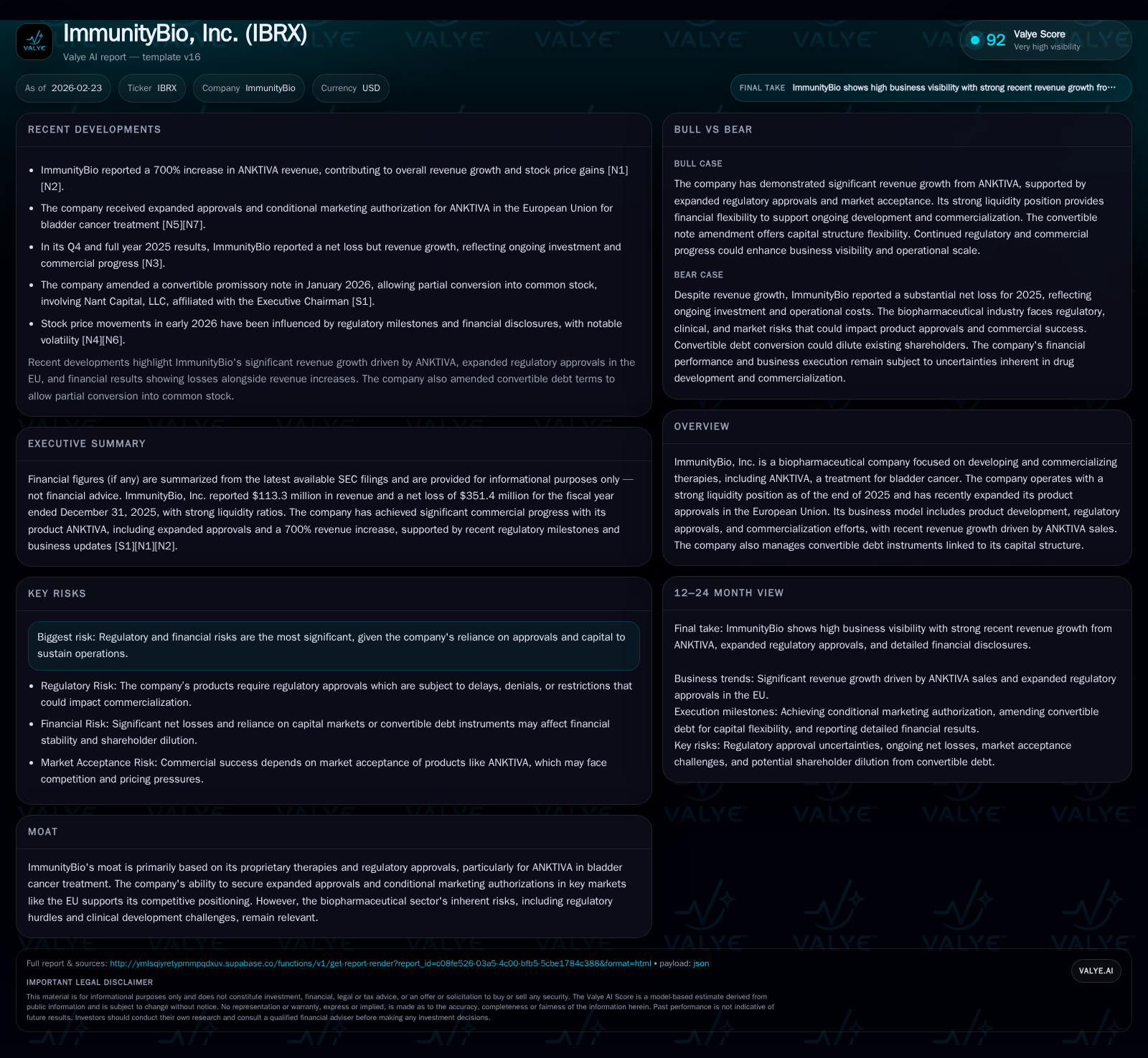

ImmunityBio, Inc. has exhibited dramatic revenue growth fueled predominantly by its ANKTIVA bladder cancer treatment, with sales expanding over 700% year-over-year in 2025 following EU regulatory nods and broader commercial availability. Despite the top-line momentum, the company remains unprofitable with significant operating losses and negative cash flows reflecting ongoing development and commercialization expenses. ImmunityBio’s future trajectory hinges on execution in scaling ANKTIVA sales internationally, managing regulatory risks, and addressing a stretched balance sheet burdened by convertible debt. Investors should monitor upcoming regulatory milestones, market adoption rates of ANKTIVA combinations, and any shifts in capital strategy given the high burn rate.

Overview

ImmunityBio, Inc. operates as a biopharmaceutical company concentrating on developing and commercializing immunotherapies, most notably ANKTIVA® (nadofaragene firadenovec), which targets bladder cancer treatment. Recently, the company's strategic focus on expanding regulatory approvals domestically and internationally has led to a pronounced inflection in revenue growth.

Historical Financial Performance

From a financial perspective, ImmunityBio demonstrated a remarkable acceleration of revenues in fiscal year 2025 compared to previous years. Total revenue surged to approximately $113 million in 2025 from just $14.7 million in 2024—a staggering increase of over 668% year-over-year [F1]. This spike correlates closely with the expansion of ANKTIVA’s commercial footprint following key approval milestones including FDA resubmissions and European Commission conditional marketing authorizations.

However, this positive topline trajectory contrasts with continuing net losses that reflect significant investments ImmunityBio is making in clinical development, manufacturing scale-up, marketing efforts, and general corporate costs. The operating loss improved somewhat but remained substantial at around $256 million (down from $344 million a year earlier), demonstrating persistent operating leverage challenges typical of late-stage biopharmaceutical manufacturers transitioning from R&D mode to commercialization [F1]. Net loss followed suit improving by about 15%, from a very high baseline at $351 million for FY2025.

Operating cash flows continue to be negative with roughly -$305 million outflows recorded—better than prior periods but signaling ongoing high cash burn against the nascent revenue base [F1]. Capital expenditures decreased notably reflecting a shift away from heavy infrastructure investment.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 113 | -351 | -305 | -256 | +668.3% | +15.0% |

| 2024 | 15 | -414 | -391 | -344 | +2270.6% | +29.1% |

| 2023 | 1 | -583 | -367 | -362 | +159.2% | -40.0% |

| 2022 | 0 | -417 | -338 | -351 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -309 | 70.2 |

| 2024 | -398 | 84.6 |

| 2023 | -397 | 99.4 |

| 2022 | -416 | 93.1 |

Source: SEC companyfacts cache [F1].

Note: Dividends paid are not available in provided tags; share repurchases have been negligible per filings.

Business Model & Drivers

ImmunityBio primarily operates through proprietary immunotherapy candidates progressing from clinical development into commercialization phases. The current commercial stage centers heavily on ANKTIVA, a gene therapy approved for non-muscle invasive bladder cancer that has exhibited promising clinical benefit especially when combined with Bacillus Calmette-Guérin (BCG) treatment regimens.

Recent approvals have broadened market access significantly:

- In February 2026, the European Commission granted conditional marketing authorization for ANKTIVA plus BCG across 33 countries marking an important step toward geographic diversification outside North America [N5][S16].

- The Saudi Food and Drug Authority granted accelerated approval for expanded indications including combination therapy with immune checkpoint inhibitors targeting metastatic non-small cell lung cancer post-standard care treatments highlighting pipeline breadth beyond bladder cancer [S24].

Commercial execution involves market education for prescribers, patient advocacy engagement for rare oncology segments, establishing reimbursement pathways across fragmented healthcare systems in Europe and emerging markets, as well as scaling manufacturing capacities.

Capital Structure & Financial Position

A significant element shaping ImmunityBio's financial profile is its capital structure dominated by sizeable convertible debt instruments connected to Nant Capital LLC, affiliated with Executive Chairman Patrick Soon-Shiong [S15]. These instruments totaled approximately $505 million principal with amendments allowing partial conversions into common stock at holders' discretion—introducing potential dilution dynamics affecting shareholder equity metrics.

The balance sheet shows cash and equivalents near $88 million at end-2025 against current liabilities of about $61 million yielding a strong current ratio exceeding five—indicating adequate short-term liquidity [F1]. Nonetheless, prolonged operating losses necessitate continued access to external funding sources through equity or debt markets supported by shelf registrations which were augmented recently increasing authorized shares to facilitate capital raises or incentive grants [S9][S21].

No dividends or repurchase programs were executed or announced as capital allocation clearly focuses on reinvestment into pipeline advancement and commercial scale-up activities.

Forward-Looking Considerations & Catalysts

Future prospects hinge on several key factors:

- Successful penetration of European markets where ANKTIVA's conditional authorization must translate into physician adoption and payer reimbursement.

- Completion and positive outcomes of further clinical trials supporting label expansions beyond bladder cancer into lung cancer combinations that can materially expand patient addressable markets [N10][S24].

- Managing regulatory risks including potential delays or requirements imposed by agencies like FDA regarding supplemental Biologics License Applications (sBLAs), although recent dialogues suggest clearer resubmission paths [N11][N14].

- Strengthening margins via operational efficiencies as sales volumes ramp offsetting fixed SG&A costs.

- Navigating ongoing financial risks related to capital raises or debt conversions without diluting shareholder value excessively.

Absent explicit guidance disclosures on future financial metrics or milestones beyond regulatory announcements, monitoring quarterly earnings trends, cash burn rates, progress reports on clinical programs, and competitive oncology therapy landscape developments remain vital analytical checkpoints.

Returns & Capital Allocation Review

Due to continuous heavy investments in pipeline development and commercialization, ImmunityBio has yet to approach profitability thresholds despite robust revenue growth trajectories. Approximate return on equity (ROE) calculations are skewed as stockholders' equity remains negative at roughly -$500 million suggesting accumulated deficits outweigh book value despite improving net losses—reflecting typical characteristics of biopharma companies transitioning toward commercial productization after long R&D phases [F1].

Free cash flow stays deep in the red given negative operating cash flows far exceeding low capex outlays signifying limited asset buildup but sustained expense levels particularly SG&A given launch activities.

No dividend distributions occurred; share repurchases have not been recorded recently aligning with conventional biopharma strategies favoring reinvestments over returns until consistent profitability emerges.

Governance & Management Updates

The appointment of Bruce Wendel—a seasoned pharmaceutical executive with experience spanning Bristol-Myers Squibb leadership roles associated with blockbuster drug commercialization—to the Board adds relevant expertise enhancing corporate governance during an active growth phase [S23]. Such board-level reinforcements are customary as companies ramp commercial operations requiring robust oversight on strategy execution risks including regulatory compliance, intellectual property stewardship, and capital management.

Industry Context Analysis

ImmunityBio's scenario typifies challenges facing emerging biotechnology firms driven by innovative therapies where topline acceleration follows landmark approvals yet margin stabilization lags due to upfront fixed costs inherent to clinical development phases combined with expensive launch commercialization efforts across global fragmented healthcare systems.

The oncology segment presents evolving opportunities but also complex payer negotiations reflecting diverse national health policies particularly within European Union jurisdictions requiring sophisticated market access strategies beyond mere regulatory endorsements.

Convertible debt linked to insider entities may complicate financial statement interpretation due to potential equity dilution pending conversion choices influencing ownership structures—a nuance increasingly scrutinized within investor circles balancing growth optimism against financing risk premiums.

Conclusion

ImmunityBio’s financial results reflect a critical inflection point where substantial product approval achievements translated into outsized revenue growth while underscoring persistent structural losses characteristic of biopharma firms scaling commercial operations globally.

Navigating the path from innovative therapeutic concepts through rigorous regulatory approvals into profitable large-scale sales remains challenging amidst clinical uncertainties and capital market dependencies.

Close attention should be maintained on progress reports regarding cross-market adoption of ANKTIVA treatments especially outside US borders including reimbursement success; next-step pipeline candidate advancement; cash flow management; and overall balance sheet evolution given convertible debt positions that could alter shareholder alignments significantly.

Disclaimer: This analysis is based purely on publicly available data up to February 2026 compiled from SEC filings and reputable financial media sources without forecasting or providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments