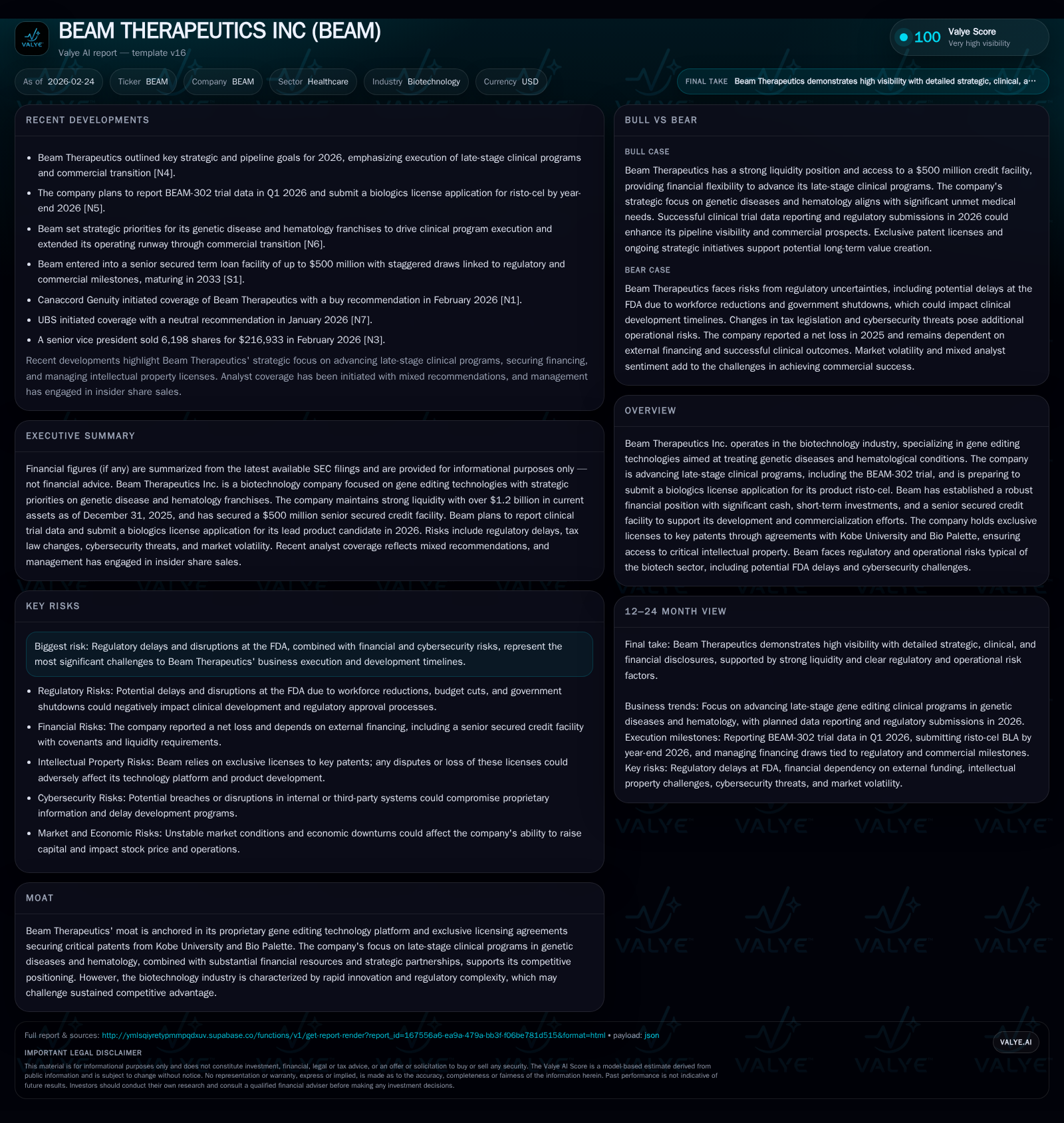

Beam Therapeutics' Transition to Commercialization Highlights Strategic Capital Deployment

Beam moves towards commercial launch while leveraging a $500M senior secured credit facility to support late-stage gene editing clinical programs.

Beam Therapeutics, a biotechnology firm specializing in advanced gene editing, is poised at a pivotal inflection as it approaches critical clinical data readouts and regulatory submissions for its hematology-focused therapies. Despite operating losses typical of its developmental stage, the company strengthened its balance sheet through a milestone-linked $500 million senior secured credit facility that enhances financial flexibility amid an uncertain FDA review environment. Investors and stakeholders should monitor upcoming BEAM-302 trial data and the year-end biologics license application (BLA) submission for risto-cel as key catalysts shaping Beam's progression from R&D intensity to early commercialization.

Trajectory of Growth: Historical Financial Trends and Operational Drivers

Beam Therapeutics' financial history through FY2025 reflects the archetypal trajectory of an innovative biopharmaceutical developer transitioning from pure research into early commercialization phases. The company's revenues remain nominal—reflecting nascent commercial activity related to initial product introductions—with reported revenue at only $24,000 in FY2020 and absent any meaningful increase up to FY2025 (last reported revenue peak was $6,000 in early 2021), underscoring the developmental stage prior to full market entry [F1].

Operating income paints a telling picture of evolving operating discipline amid ambitious R&D undertakings. The company endured steep operating losses reaching approximately -$415.6 million in FY2024 but achieved a meaningful narrowing of that loss by around 7.7% to -$383.7 million in FY2025 [F1]. This improvement despite scaling clinical activities suggests effective expenditure controls or timing differences in development spends as Beam advances late-stage trials.

Net income mirrored this trend with an even more pronounced improvement: from a -$376.7 million net loss in FY2024 to -$79.9 million in FY2025—a remarkable near 79% reduction YoY [F1]. Such gains may relate partly to non-operating items or one-time expense adjustments but nonetheless signal positive earnings momentum consistent with pre-commercial biotech peers.

Operating cash flow remained heavily negative and stable through FY2024-FY2025 periods at approximately -$347 million and -$345 million respectively, illustrating ongoing cash burn consistent with high investment intensity [F1]. Meanwhile, capital expenditures rose sharply (+67%) to about $14.9 million in FY2025 after a low of $8.9 million the prior year, signaling stepped investments into infrastructure possibly linked to commercial readiness and technology scale-up [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -80 | -345 | -384 | 15 | +78.8% |

| 2024 | -377 | -347 | -416 | 9 | -184.3% |

| 2023 | -133 | -149 | -176 | 34 | +54.2% |

| 2022 | -289 | 23 | -338 | 49 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -360 | -6.5 |

| 2024 | -356 | -51.4 |

| 2023 | -183 | -13.5 |

| 2022 | -26 | -39.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue not regularly disclosed beyond small amounts; thus omitted due to lack of comparable annual data.

These operational metrics reflect Beam’s profile as an early-stage gene editing company intensely investing in platform validation through late-phase clinical trials while positioning for first product launches.

Pipeline Progress: Late-Stage Trials and Regulatory Timelines

Central to Beam’s strategic horizon are its late-stage clinical programs targeting genetic diseases and hematologic malignancies via proprietary base editing technology platforms secured under exclusive license agreements with Kobe University and Bio Palette [S18][S17]. The pivotal BEAM-302 trial is expected to report data in Q1 2026—an inflection point likely to inform regulatory filing strategies as well as validate the therapeutic potential of candidates [N3][N8].

Complementing this effort is the anticipated biologics license application (BLA) submission for risto-cel scheduled by year-end 2026 [N3][N8]. Risto-cel focuses on hematological oncology targets, aiming to harness precise gene edits for durable therapeutic efficacy.

Regulatory timelines at the U.S. Food and Drug Administration (FDA) present crucial dependencies; Beam’s credit facilities tie tranche availability directly to specific FDA milestones including BLA acceptance and approval [S4][S5]. However, regulatory risk remains heightened given recent FDA staffing reductions (~17% workforce decrease following HHS-wide reorganizations) potentially delaying review cycles [S2]. FDA user fee programs under the Prescription Drug User Fee Act (PDUFA) continue funding user fees yet overall review capacity faces uncertainties amid federal budget negotiations and operational restructuring [S2][S6].

Such risks underscore the necessity for agile regulatory strategy management alongside proactive trial execution.

Capital Structure and Liquidity: Senior Secured Credit Facility as a Financial Leverage Tool

On February 24, 2026, Beam closed a sophisticated senior secured term loan facility valued up to $500 million composed of multiple delayed draws contingent on regulatory progress markers: an upfront draw of $100 million on closing; subsequent conditional draws totaling $400 million upon FDA BLA acceptance for risto-cel (Delayed Draw A), BLA approval (Delayed Draw B), achievement of specific risto-cel sales thresholds, plus a discretionary tranche requiring lender consent [S4][S5][S8].

Interest accrues at SOFR plus a margin of 6.50%, subject to customary floors and fees reflective of biotech credit risk profiles. This senior secured loan is heavily collateralized by intellectual property—including core patents underpinning base editing technologies—and other material subsidiaries’ assets [S4][S8], insulating lenders against intellectual property value erosion.

Financial covenants mandate maintenance of minimum liquidity reserves scaled by market capitalization thresholds; e.g., liquidity must exceed $40 million if market cap falls below $1.75 billion with increments triggered upon tranche draws—mechanisms designed ensure solvency amid fluctuating valuations [S4][S5]. Additionally, restrictive covenants limit additional indebtedness beyond capped convertible notes ($400 million max outstanding), asset dispositions affecting core IP, dividend payments, mergers or investments without lender approval [S4].

This layered financing architecture exemplifies emerging biotech firms’ reliance on structured debt facilities tightly coupled with regulatory milestones rather than traditional amortizing bank loans.

Strategic Capital Allocation: Balancing R&D Investment, Debt Capacity, and Commercial Launch Funding

Capital deployment focuses heavily on advancing late-stage clinical programs while preparing infrastructure for initial commercial launch expenditures tied to risto-cel’s market entry [N3][N20].[F1] FY2025 capex increased substantially (+67%) indicating parallel expansion efforts likely encompassing manufacturing scale-up capabilities or platform technology enhancements.[F1]

Operating cash flows remain negative at ~$345 million annually yet steady compared to prior years despite scaling activities.[F1] The free cash flow approximation for FY2025 stands near -$360 million underscoring continued reliance on equity capital raises supplemented now by debt financing.[F1]

Notably, Beam does not distribute dividends nor has it conducted share repurchases—consistent with sector norms where capital retention fuels sustained innovation cycles before commercialization profitability.[S14][S15][S19][S20]

The recent extension of operating runway through this credit facility mitigates near-term refinancing risks allowing strategic prioritization between continuing R&D pipeline commitments versus mounting commercialization cost structures.[N3]

Regulatory Environment and Risk Dynamics Impacting Execution

Beam Therapeutics faces considerable exposure stemming from evolving regulatory landscapes affecting clinical development pacing.[S1][S2]

FDA workforce reductions following government mandated reorganization reduced full-time personnel by approximately 3,500 employees across HHS including FDA reviewers responsible for biologic licensing applications.[S2]

Potential budget cuts compound uncertainty over sustained PDUFA fee program efficacy which funds majority review activities.[S2]

Failures or delays in receiving timely guidance or approvals could postpone commercialization timelines significantly.[S6]

Beyond procedural challenges lies escalating cybersecurity concern targeted at proprietary biotechnology know-how.[S9][S10][S11][S13] Sophisticated cyberattacks—including those leveraging artificial intelligence—pose threats not only to confidentiality but also operational integrity such as potential contamination or data loss during sensitive trials.[S9]

Mitigation efforts continue but breaches could be materially disruptive resulting in delayed approvals or competitive disadvantage.[S9]

Performance Metrics in Focus: Recent Operating Results and Cash Flow Evolution

FY2025 ended with an operating loss near $384 million despite improvements from previous years’ steeper deficits highlighting controlled scalability amidst research demands.[F1] Net income improved strikingly from loss levels over $370 million two years prior down to under $80 million deficit reflecting either non-recurring cost management or improved expense recognition strategies.[F1]

Operating cash flow continues large negative burn showing slight improvement yet reflecting persistent net cash outflow owing largely to expanded trial activities.[F1] Capex surged suggesting allocation toward infrastructure necessary for imminent commercial operations such as manufacturing plant upgrades or IT systems dedicated to product rollout.[F1]

Balance sheet strength remains robust: stockholders’ equity exceeded $1.23 billion indicating solid capitalization relative to the net loss position supporting estimated ROE at an approximate negative 6.5% ratio aligned with peer gene therapy developers progressing towards market entry.[F1]

Liquidity metrics are healthy: current ratio above 13x underscores substantial current assets over short-term liabilities creating a cushion essential given operational volatility typical at this growth stage.[F1]

Market Expectations: Upcoming Catalysts and Analyst Sentiment

Market focus centers on Q1 2026 BEAM-302 trial top-line data release which will serve as critical validation within the genetic disease segment; positive outcomes could accelerate investor confidence ahead of filing milestones [N3][N8].

Concurrently, the planned year-end BLA submission for risto-cel is forecasted as the immediate step towards commercialization launching revenue generation potential after years of R&D capital consumption [N8].

These milestones precipitated Canaccord Genuity’s initiation of coverage with a Buy rating earlier in February 2026 signaling growing analyst optimism aligned with these transitional achievements [N4]. Contemporary stock movements reflect anticipation tied closely to definitive clinical data points expanding visibility among institutional investors [N1][N4].

Investors will primarily monitor FDA guidance updates due to inherent review risks alongside sales ramp assumptions post-approval impacting long-term growth trajectories.

This analysis solely aims to provide grounded insights based on publicly available financial filings and credible news sources concerning Beam Therapeutics Inc., without offering investment advice or recommendations.

Disclaimer: This report is intended for informational purposes only; it does not represent an investment opinion nor warrant future company performance outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments