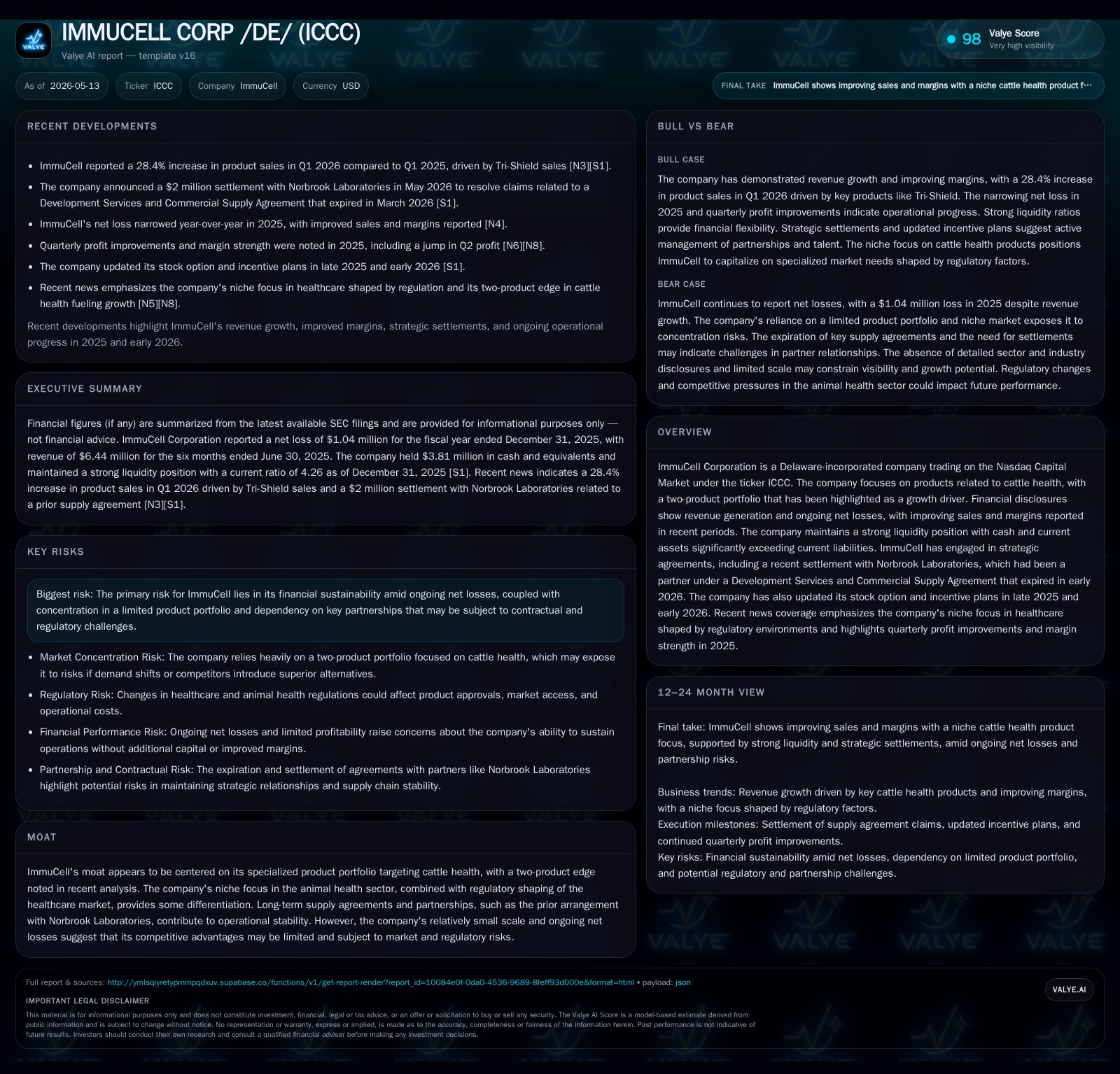

ImmuCell Corp Resolves Key Partnership Dispute, Bolsters Path to Revenue Growth

The settlement with Norbrook Laboratories concludes a pivotal contractual chapter, catalyzing clearer strategic control and supporting recent sales momentum in ImmuCell's niche cattle health segment.

In May 2026, ImmuCell Corporation finalized a $2 million settlement with Norbrook Laboratories related to their expired Development Services and Commercial Supply Agreement, removing significant legal overhang. This resolution repositions ImmuCell for independent commercialization while recent preliminary Q1 2026 results showed strong revenue growth (+28.4%), driven largely by its flagship Tri-Shield product. Despite ongoing net losses and modest scale limiting competitive power, the company’s improved margins and a robust current ratio underscore operational resilience amid evolving market dynamics. The exit from the Norbrook partnership marks a strategic inflection point with execution on direct sales channels now under scrutiny.

Settlement Deed with Norbrook Laboratories: Strategic Implications

On May 8, 2026, ImmuCell Corporation and Norbrook Laboratories Limited reached a Settlement Deed resolving all outstanding claims tied to their former Development Services and Commercial Supply Agreement dated September 2019, which expired on March 31, 2026 [S3]. Under the agreement terms, Norbrook paid ImmuCell $2 million without any admission of wrongdoing by either party. This settlement eliminates prior contractual uncertainties that had shadowed ImmuCell’s operations and clears the path for the company to pursue a more autonomous commercialization approach going forward.

The significance of this event lies in the closure of a nearly seven-year partnership that had defined supply and development arrangements for ImmuCell’s leading products. Removing this legal overhang allows management to better focus on direct sales execution and strategic business model adjustments without distraction or incremental negotiation risk.

Business Model and Product Portfolio Quality

ImmuCell’s revenue is principally derived from two immunological cattle health products designed to improve herd immunity and reduce disease incidence [S1]. Their flagship product, Tri-Shield, targets calf scours prevention through maternal antibody transfer enhancement—a critical health challenge in the beef and dairy industries. Scientific trials underpinning product efficacy help support customer confidence among veterinarians and producers.

Revenue generation depends heavily on product volume sold through veterinary channels who act as both influencers and direct buyers. The revenue mechanics involve recurring usage patterns aligned with calving cycles, creating somewhat seasonal demand peaks. Pricing is subject to competitive pressures but benefits from the specialized nature of the immunological products which have relatively high value-add compared to commodity feed additives.

Customer retention is supported by product effectiveness evidence combined with longstanding industry relationships. However, the company’s narrow portfolio inherently concentrates risk around these core offerings; expansion into adjacent cattle health segments remains limited at this stage.

Competitive Positioning within the Animal Health Market

Operating in a niche segment of the broader animal health industry—specifically bovine immunologicals—ImmuCell faces competition from larger multinational animal pharma firms as well as smaller specialty producers [S1]. The company’s modest scale tempers pricing power and restricts bargaining leverage with distribution partners.

Regulatory factors exert important influence over product approvals, manufacturing standards, and marketing claims, constraining agility but also creating barriers to entry against less specialized competitors. Previously partnering with Norbrook granted ImmuCell broader commercial reach; post-termination, it may face challenges rebuilding or expanding distribution independently.

Supply chain reliability remains vital given the biological nature of its products that require stringent quality controls. The settlement enables ImmuCell to reassess supply arrangements while maintaining proprietary formulations.

Growth Drivers Anchored in Product Sales and Market Penetration

Recent preliminary data indicate robust momentum: Q1 2026 reported product sales growth of 28.4% year-over-year driven primarily by Tri-Shield adoption [N1][S2]. Such acceleration suggests growing acceptability among veterinarians responding positively to demonstrated clinical benefits amid heightened focus on disease prevention management.

Structural demand drivers include ongoing modernization in livestock farming practices emphasizing herd health economics and antibiotic stewardship programs increasing reliance on immunological interventions. Geographic expansion potential exists but is unquantified in current disclosures.

Sustained growth depends on broadening veterinarian endorsements and incremental increases in treated herd populations, closely linked to macro factors such as cattle inventory cycles and market prices affecting producer spending behavior.

Risks and Constraints Reflecting Financial and Market Dynamics

Despite top-line improvement, ImmuCell recorded a net loss nearing $1 million for fiscal year 2025 while reporting positive operating income reflecting narrow profitability trends [F1][S1]. These losses highlight ongoing challenges maintaining financial sustainability given investment needs in commercialization offset by constrained revenue scale.

The termination of the Norbrook agreement necessitates restructuring marketing and logistics functions potentially raising cost bases before scaled efficiency gains materialize [S3]. Concentration risks remain high due to dependence on a limited number of products within a specialized market.

Balance sheet considerations underscore risk as total debt stood at approximately $9.54 million against cash reserves around $3.8 million as of late 2025; after accounting for cash holdings, net debt was about $5.7 million [F1].

Regulatory or competitive disruptions could impair market access or pricing ability given limited product breadth; any failure to maintain veterinarian confidence might slow adoption ramp.

Key Upcoming Catalysts and Monitoring Points

Investors and observers should track subsequent quarterly reports following the May settlement to verify if revenue growth sustains or expands beyond initial Q1 figures [N1][S2]. Metrics such as gross margin trends will provide signals about cost-of-sales optimization post-partnership exit.

The implementation impact of newly approved stock option and incentive plans (updated late 2025/early 2026) will shape personnel costs going forward [S1], pertinent for evaluating operating leverage improvements.

Management commentary regarding strategic roadmap execution will be crucial as independent commercialization efforts accelerate; renewed partnerships or expanded direct sales initiatives will serve as indicators of adaptability.

Corporate governance changes—with new directors bringing seasoned animal health sector experience—also warrant attention for how they influence strategy refinement [S15].

Current Financial Profile Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.8mm | |

| 2025-12-31 | ||

| Current assets | $17mm | |

| 2025-12-31 | ||

| Current liabilities | $4mm | |

| 2025-12-31 | ||

| Current ratio | 4.26x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Liquid assets comfortably cover near-term obligations while acknowledging ongoing negative net earnings even as small operating profits appear [F1][S2][S3]. Monitoring free cash flow generation capacity relative to debt amortization schedules will be critical amid efforts to sustain operations without dilutive capital raises.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding ImmuCell Corporation securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments