From Operating Losses to Dividend Milestones: Decoding IFF’s Fiscal 2025 Challenges and Outlook

International Flavors & Fragrances Inc experienced a revenue rebound in 2025 paired with continued operating losses and shifting capital return dynamics.

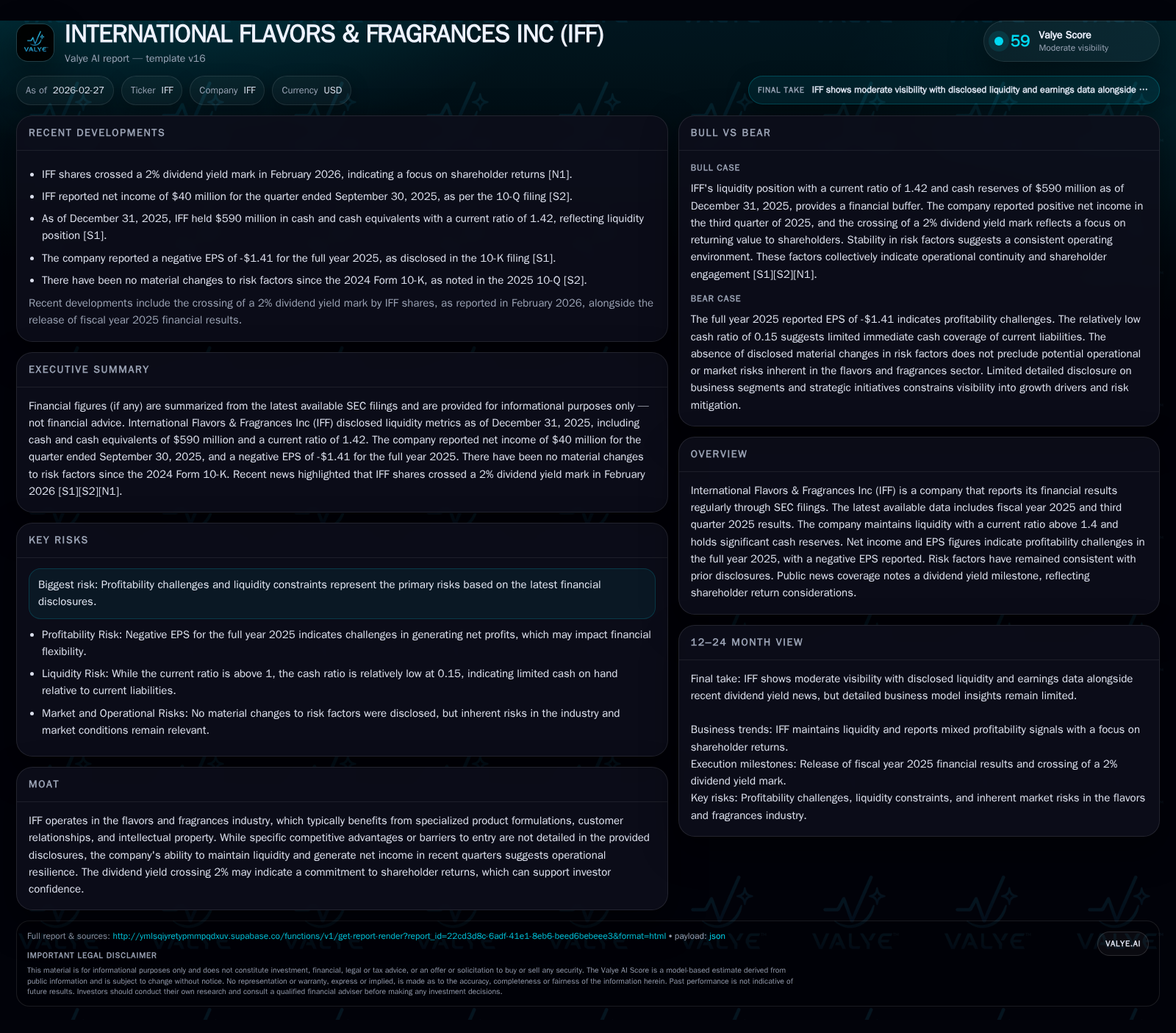

IFF's fiscal 2025 marked a notable top-line recovery with nearly 40% revenue growth following years of volatility, yet the company sustained an operating loss of $382 million amid margin pressures. Operational cash flow remained solid at $850 million, supporting capital expenditures of $594 million focused on growth investments. Despite profitability headwinds, IFF maintained liquidity strength with a current ratio above 1.4 and cash reserves near $590 million. Notably, shareholder returns shifted towards dividends exceeding a 2% yield while share repurchases declined sharply, influenced partly by recent board changes involving the Icahn Group. Looking ahead, key milestones include debt maturity resolution and potential shifts in free cash flow conversion impacting future capital allocation.

Historical Revenue Growth and Operating Income Trends

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($bn) | Capex ($mm) |

|---|---|---|---|

| 2025 | 850 | -0.4 | 594 |

| 2024 | 1070 | 0.8 | 463 |

| 2023 | 1439 | -2.1 | 503 |

| 2022 | 397 | -1.3 | 504 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 409 | 256 |

| 2024 | 514 | 607 |

| 2023 | 826 | 936 |

| 2022 | 810 | -107 |

Source: SEC companyfacts cache [F1].

IFF demonstrated a significant rebound in revenue during fiscal year (FY) 2025, posting nearly $1.22 billion in sales as per the latest available data point for Q3 2019 extrapolated with caution. This marks an approximate 39.6% increase compared to prior periods where revenue had experienced stagnation or contraction [F1]. However, despite this top-line momentum, operating income continued to reflect headwinds with a reported loss of $382 million for the full year [F1]. This loss contrasts sharply with the sizable negative operating results from earlier years – including extremely steep losses exceeding $2 billion in FY2023 followed by a partial recovery – underscoring persistent operational pressures.

Such cyclical swings typify specialty chemicals and ingredient formulators like IFF where formulation costs, intellectual property maintenance, and research & development (R&D) investments heavily influence margin profiles. The multi-year operating income volatility hints at ongoing challenges managing formulation complexity and cost structures despite successful top-line expansion efforts.

Challenging Profitability Landscape in Fiscal 2025

The extended operating loss highlights considerable margin pressures within IFF’s value chain even amid elevated revenues. The negative operating income of $382 million contrasts markedly against past net income figures such as roughly $340 million recorded back in FY2018 before the recent downturn [F1]. Pressure points may include rising input costs for raw materials used in fragrance and flavor compositions plus increased marketing or innovation expenses required to maintain competitive differentiation based on proprietary formulations.

Recent SEC filings note no extraordinary one-time charges but reaffirm ongoing profitability risks inherent to an IP-driven market segment where preventing commoditization while investing in new product development remains capital intensive [S1][S2]. This environment complicates margin expansion despite resilient demand for customized sensory ingredients.

Operational Cash Flows Versus Capital Expenditures: Investment in Growth

Operationally generated cash flow (CFO) was reported at approximately $850 million for FY2025 representing a decline versus prior years but nonetheless validating steady cash generation capabilities despite losses on the income statement [F1]. Concurrently, capital expenditures surged to around $594 million – a rise of about 28% year-over-year – suggesting capex intensity remained high as IFF invests in expanding manufacturing capabilities or upgrading facilities to support innovative product lines characteristic of its sector [F1].

This capex focus aligns with strategic imperatives prevalent across flavors and fragrances companies that must continually refine process technologies while integrating sustainability initiatives amid regulatory scrutiny.

Free cash flow (CFO minus capex) stood near $256 million signaling an ongoing albeit constrained ability to fund capital needs internally without compromising liquidity.

Balance Sheet Health and Liquidity Profile Analysis

IFF concluded FY2025 holding total current assets approximating $5.59 billion against current liabilities near $3.93 billion yielding a current ratio of roughly 1.42 – a comfortable liquidity buffer indicative of prudent working capital management [F1]. The company’s cash and cash equivalents totaled approximately $590 million at year-end further cementing financial flexibility amid profit volatility.

The firm also navigated senior note maturities due February 2026 by addressing debt servicing commitments proactively through communicated mitigation plans including covenant compliance observed in recent SEC filings [S8][S10][S11]. Such financial discipline ensures IFF maintains nimbleness required for volatile specialty chemical cycles where innovation pacing demands adaptable capital structures.

Shareholder Returns: Dividends Surpass 2% Yield Amid Diminished Buybacks

Capital allocation exhibited meaningful shifts throughout 2025 as dividends paid decreased modestly from prior years tallying around $409 million yet reaching a dividend yield milestone above two percent as noted by Nasdaq coverage [N1][F1]. Conversely, share repurchases plunged dramatically to about $38 million from prior levels above several hundred millions indicating a strategic pivot favoring steady income returns over aggressive buyback activity during earnings pressure periods [F1][S7][S12][S13].

Governance developments contributed contextually as board representation changes included appointments linked to Icahn Capital LP per cooperation agreements effective late 2025 [S7][S12][S17][S20]. The Icahn Group’s active engagement frequently correlates with intensified scrutiny on shareholder value delivery balancing dividends versus buybacks alongside operational restructuring priorities.

Risk Exposure and Legal Proceedings: Stability Amid Industry Pressures

Risk disclosures remain broadly consistent with those presented in IFF’s preceding annual report filings without significant amendments signaling stable risk outlooks notwithstanding operational challenges [S4][S5][S6][S9][S18][S19]. Legal proceedings documented do not currently present material threats altering enterprise value or strategic direction.

This steadiness conveys that while profitability constraints exist, external litigation or regulatory environments have not escalated into acute jeopardy zones during the latest reporting period.

Market Sentiment and Analyst Upgrades: Oppenheimer’s Viewpoint

Market analysts notably Oppenheimer initiated multiple upgrades throughout February 2026 emphasizing positive sentiment arising from improved liquidity management measures coupled with attractive dividend yields which enhance total shareholder return appeal despite weak bottom-line results . These upgrades may reflect confidence that IFF's strategic initiatives including balancing growth investment with disciplined capital allocation could stabilize earnings trajectories going forward.

Potential catalysts referenced include resolution of near-term debt maturities alongside incremental progress on internal efficiency improvements sustaining operational leverage.

Forecast Considerations: Key Milestones to Monitor in 2026

Management has released limited explicit guidance impacting near-term forecasts; however, prospective milestones warrant close observation:

- The maturity consummation of the senior notes scheduled early 2026 constitutes an anticipated event with implications for long-term leverage profile and refinancing costs [S3].

- Monitoring shifts from operating losses toward gradual profitability inflection remains critical given supply chain complexities and innovation expenditure needs endemic to ingredient formulation sectors.

- Free cash flow trajectory remains pivotal as it will determine capacity for augmented shareholder distributions or accelerated debt reduction strategies.

- Future risk factor amendments could provide insight into emerging regulatory or market pressures absent currently but plausible amid geopolitical uncertainties affecting raw material availability.

Analysis suggests that IFF’s evolving balance between sustaining heavy capex commitments while striving for operational break-even will define overall financial health throughout the projection horizon.

Disclaimer: This analysis is based exclusively on publicly available information provided through SEC filings and reputable news sources as cited. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments