Iron Horse Acquisition II Corp.: Navigating SPAC Structural Complexities Amid Liquidity Pressures

A critical examination of IRHO’s precarious SPAC framework and financial vulnerabilities as the company races to complete its transformative business combination.

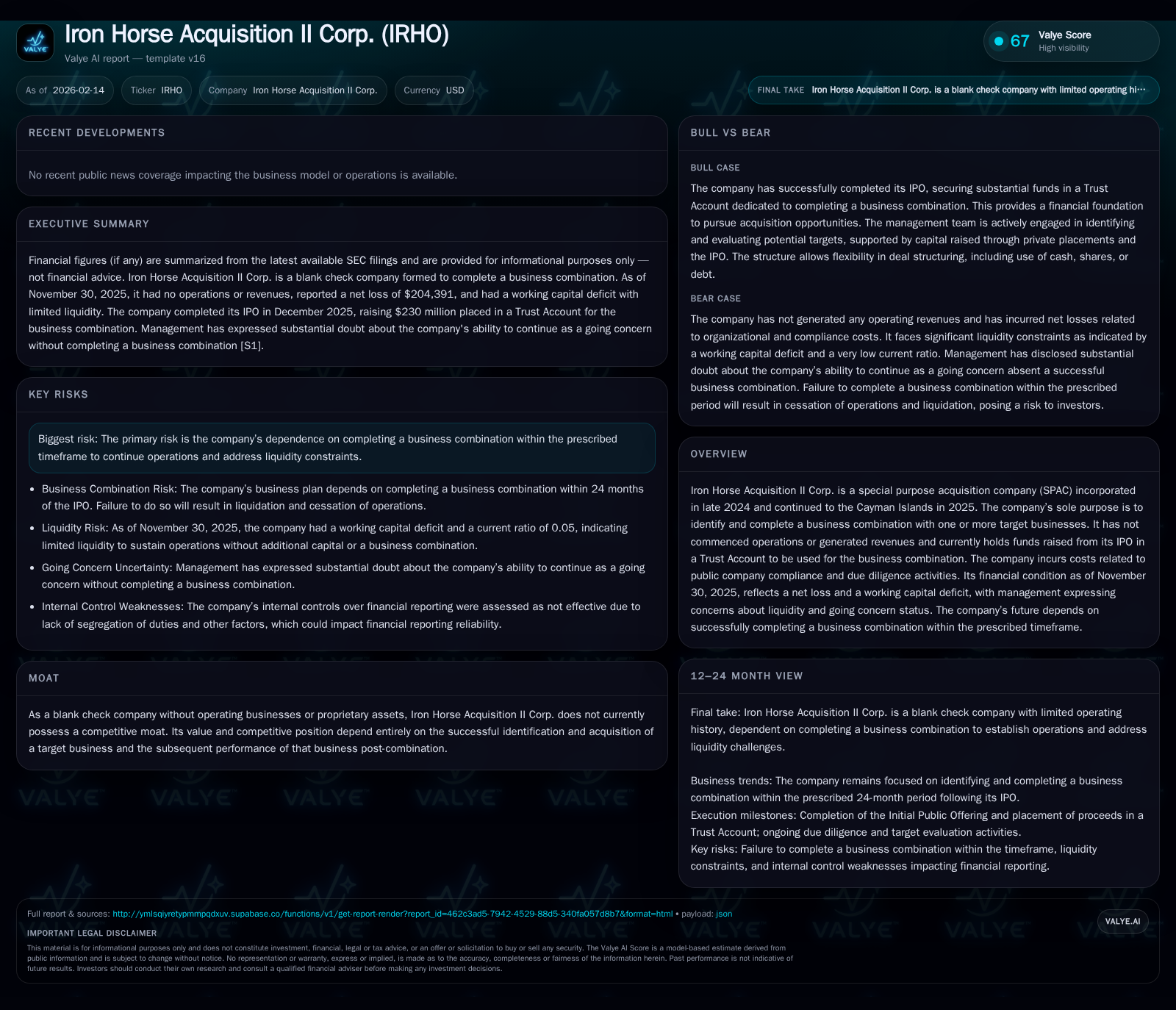

Iron Horse Acquisition II Corp. (IRHO), a blank check company formed in late 2024, operates under significant pressure to consummate a business combination within the regulatory timeline to avoid liquidation. Having transitioned its incorporation from Delaware to the Cayman Islands by mid-2025, IRHO currently exhibits a stark financial profile marked by early net losses and an acute working capital deficit. Despite holding $230 million in a trust account sourced from its IPO and private placement proceeds, operational liquidity remains a concern as these funds are restricted pending deal closure. Management faces the daunting challenge of identifying an acquisition target while navigating the high-stakes SPAC timetable, with no inherent competitive moat until such a transaction transpires.

Iron Horse’s Genesis and Structural Evolution: From Delaware to the Cayman Islands

Iron Horse Acquisition II Corp. was incorporated initially in Delaware on November 26, 2024, marking its entry into the crowded SPAC market as a blank check vehicle designed solely for effecting a transformative business combination[S1]. Merely eight months later, on July 25, 2025, it executed a transfer by continuation to the Cayman Islands—a jurisdiction favored for flexible corporate governance structures and tax efficiencies common among SPACs targeting diverse global acquisitions. Following this strategic shift, on September 12, 2025, Iron Horse Acquisition II Corp. was incorporated anew in the Cayman Islands. Just weeks later, on September 30, it merged with its Cayman-incorporated iteration, with this latter entity surviving as the continuing company[S1]. This series of transactions resulted in IRHO operating as an exempted company under Cayman Islands law.

While seemingly procedural, this move implies deliberate positioning toward regulatory environments conducive to cross-border deals or investor preferences. The transition may afford streamlined corporate flexibility but simultaneously subjects shareholders to different regulatory regimes than initial U.S.-only incorporation would entail. Thus far, this structural evolution primarily shapes IRHO’s legal framework rather than operational capabilities given its pre-combination status.

Financial Snapshot: The Stark Realities Behind the Numbers

IRHO’s first financial year through November 30, 2025 reveals an uncompromisingly fragile economic footing. The company recorded an operational net loss totaling approximately $204,000 despite conducting no revenue-generating activities[S1][F1]. Expenses overwhelmingly encompass general administrative costs typical for public companies performing extensive due diligence and compliance functions—legal fees, auditing expenses, underwriting commissions—and organizational overhead.

More striking is the working capital deficit evident on IRHO’s balance sheet: current assets totaled roughly $25,000 juxtaposed against current liabilities exceeding half a million dollars[F1]. This yields an eyeball-grabbing current ratio near 0.05—indicative of alarming short-term liquidity challenges absent external support or capital inflows outside of the trust funds. In essence, day-to-day operational liquidity is strained from inception; any ongoing costs expendable beyond trust-related funds exacerbate negative cash flow pressures.

This snapshot underscores that despite robust investor capital secured through IPO mechanisms (discussed next), the company itself bears severe internal funding gaps. Without revenue or operating assets, IRHO relies exclusively on planned transactional events for survival.

Trust Account: Fortress of Funds or Funding Fetter?

Central to IRHO’s capital structure is the $230 million placed promptly into a trust account upon closing its IPO in December 2025[S1]. This figure aggregates proceeds from sale of units priced at $10 each alongside private placement units subscribed by sponsors and financial intermediaries.

By design and regulatory necessity governing SPAC structures post-2019 reforms, these funds are segregated from general corporate spending and are invested conservatively—limited to short-duration U.S. Treasury instruments or highly liquid money market funds conforming to Rule 2a-7 standards under the Investment Company Act[S1]. The primary intent is preservation of investor capital pending realization via approved business combinations.

However, while this safeguard protects capital earmarked for acquisition activities at minimum principal value plus modest interest gains, it also curtails managerial discretion over liquidity deployment for routine corporate expenses or underwriting reimbursements beyond predetermined allowances. Notably, interest income accrued on these investments contributes marginally to available resources but cannot be liberally accessed without diluting acquisition funds[S1].

This dichotomy creates an operational paradox: although large sums exist nominally on paper within the trust account “fortress,” they effectively fetter immediate commonsense liquidity needs essential for sustained deal sourcing efforts or incremental preparatory spending absent external cash injections.

Inherent Risks: Liquidity Constraints and Operational Void

The reliance on successful transaction closure within stipulated timelines amplifies numerous risks accentuated within IRHO’s official risk disclosures[S1]. The audit indicates management's explicit concerns regarding going concern viability tied directly to failure scenarios where no qualifying business combination is consummated within prescribed timeframes.

Given absolute absence of revenues—the company has yet to initiate operations beyond pre-IPO activities—and sizeable ongoing administrative outlays combined with suboptimal working capital metrics[F1], these factors collectively heighten existential insecurity for stakeholders.

Furthermore, uncertainties around target identification complicate proactive budgetary forecasts as due diligence expenditures fluctuate inherently with candidate complexity and market competition dynamics. Every delay intensifies liquidity hemorrhaging outside secured trust funds while compressing remaining advisory runway.

Such circumstances demand acute management focus not only on strategic deal execution but also meticulous financial stewardship just to avoid premature wind-downs without shareholder returns.

The High-Stakes SPAC Timeline and What It Means for IRHO

Iron Horse Acquisition II Corp.’s operating mandate aligns strictly with typical SPAC temporal guardrails mandating consummation of at least one qualifying business combination within 24 months following IPO closure[S1]. Failure triggers automatic redemption protocols where unit holders have rights to withdraw invested capital plus accrued interest from trust accounts leading typically to dissolution without residual equity value proposition.

This finite window imparts urgent momentum yet intense pressure upon management teams who must rapidly source viable targets amid an increasingly saturated SPAC marketplace with evolving investor expectations.

Time compression further compounds valuation challenges as buyer willingness diminishes approaching deadlines risking either necessitated concessions or deal abandonment altogether. For IRHO specifically — having inaugurated trading only recently post-IPO — clock time dwindles visibly toward forced decision points.

Thus performing under duress while balancing thoroughness against haste forms one of the defining managerial stressors shaping prospective outcomes here.

Evaluating Management’s Path Forward: Plans Amid Uncertainty

Management discloses intentions geared primarily toward aggressive evaluation of potential acquisition candidates leveraging IPO proceeds alongside available sponsor capital[S1]. Expenditures already accrued include underwriting fees totaling nearly $15.6 million along with various offering-related expenses reflecting upfront commitments.[S1]

Nevertheless, outlined strategies remain broad—focused on comprehensive due diligence processes consonant with standard M&A protocols within financial sponsors’ toolkit—but lack specificity regarding sector targets or geographies pending commercial confidentiality norms.[S1]

Financial transparency regarding current burn rates compared against available working capital outside trust accounts signals cautionary notes illuminating possible future financing necessities if transactions lag materially beyond forecast horizons.

Such ambiguity parallels common SPAC challenges differentiating skilled operator teams effectively deploying raised funds versus those encountering protracted deal origination phases impairing momentum.

SPAC Dynamics: The Competitive Moat That Does Not Exist

As with most blank check entities pre-business combination phase, Iron Horse Acquisition II Corp. operates devoid of any distinguishing competitive advantages or proprietary operational assets["valye_report_excerpt"]. Its entire valuation premise rests fundamentally upon executing an accretive deal bringing forward profitable growth trajectories driven by acquired companies' future results.["valye_report_excerpt"]

Without such realized synergies or differentiation through innovation nor customer bases generating organic cash flows at this juncture—the enterprise sits as pure shell entity reliant singularly on sponsor expertise and timing luck.["valye_report_excerpt"]

This absence of moat underscores fundamental risk exposure typical among newly public SPACs compounded here by liquidity strains elucidated earlier—in essence making thorough diligence imperative for prospective stakeholders before engagement.["valye_report_excerpt"]

Investor Implications: Weighing Potential Against Precarity

For investors contemplating exposure in IRHO units or shares post-IPO closure(S1), evaluation must balance clearly defined upside drawn from significant locked-in IPO proceeds (~$230M)[S1] against critical caveats enumerated throughout filings.["valye_report_excerpt"]

While monetary sufficiency exists nominally supporting contemplated acquisitions theoretically enabling substantial value creation, the constrained window coupled with immediate operating liquidity gaps (evidenced by razor-thin current ratio <0.05)[F1] present non-trivial existential threats absent rapid transactional success.

Moreover, absence of diversified revenue streams places overarching reliance on sponsor networks and market conditions favoring rapid deployment; economic headwinds or shifting sector emphases threaten feasibility disrupting planned strategies.[S1]["valye_report_excerpt"]

Hence potential shareholders need nuanced appreciation that while IRHO benefits from structural safeguards protecting principal invested via trusts,[S1] residual equity upside depends highly on high-stakes execution events occurring timely without compromising terms amidst relentless timeline pressures.

Conclusion: Can Iron Horse Find Its Target and Secure Its Future?

Iron Horse Acquisition II Corp exemplifies many defining features—and perils—of contemporary SPAC enterprises forged amid bullish capital markets but challenged by exacting operational realities.[S1]["valye_report_excerpt"] Formed only recently yet rapidly repositioned jurisdictionally to optimize governance parameters,[S1] it now faces compressed deadlines exigent for transformative deals fundamental to survival.

Its fragile financial position at November FY-end characterized by operating losses absent revenues paired with straitened working capital metrics paints cautionary markers underscoring heavy dependence on trust account-protected IPO proceeds earmarked exclusively for combinations.[F1][S1]

Management’s pathway forward remains focused yet ambiguous amid competitive pressures intensified across the saturated blank-check universe seeking differentiated value propositions quickly.[S1]

In aggregate IRHO stands poised at an inflection point emblematic of broader sector dynamics where timing acumen intertwines critically with strategic clarity—determining whether it can ultimately transcend its shell status into an operating enterprise creating sustainable stakeholder wealth or succumb prematurely to regulatory-mandated liquidation outcomes.[S1]["valye_report_excerpt"]

This analysis reflects information available as of early February 2026 based solely on publicly filed documents including Iron Horse Acquisition II Corp.’s latest SEC Form 10-K (filed February 13, 2026) and proprietary Valye reports. It does not constitute investment advice or recommendations but aims to provide detailed understanding grounded in disclosed facts about this specific SPAC's business model and financial condition.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments