IRIDEX CORP: Laser Innovation and Financial Recovery in Ophthalmic Devices

IRIDEX leverages proprietary laser technologies to advance ophthalmic treatments while navigating a path toward financial stabilization amid market and operational challenges.

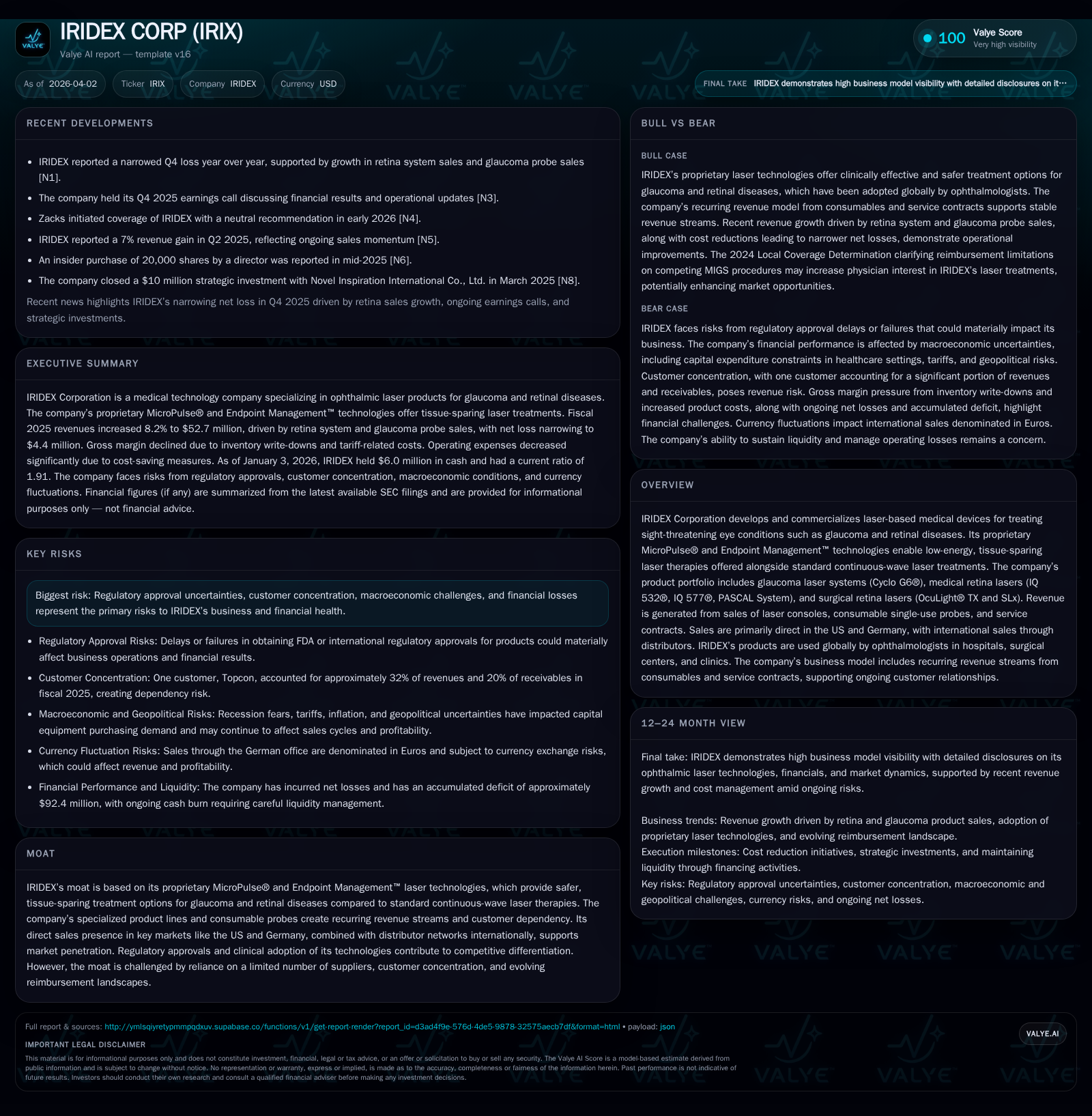

IRIDEX Corporation has developed patented MicroPulse® and Endpoint Management™ technologies that provide safer, tissue-sparing laser therapies for glaucoma and retinal conditions, generating recurring revenue through consumables. The company reported revenue growth driven largely by the retina segment with improved operating profitability and narrower net losses in fiscal 2025–2026. However, IRIDEX faces risks from concentration on a single large customer and regulatory approval uncertainties, compounded by ongoing operating cash flow deficits. Maintaining liquidity and expanding clinical adoption remain critical as it balances growth opportunities with capital constraints.

Historical Financial Trajectory and Growth Drivers

IRIDEX Corporation (IRIX) has experienced a mixed financial trajectory spanning recent fiscal years. According to its latest SEC filings [F1] covering up to fiscal year ended January 3, 2026, total revenues climbed to approximately $52.7 million in FY2025 from $48.7 million in FY2024 — an increase of nearly 8%. This growth was primarily driven by higher sales within the retina segment, which reached $30.3 million compared to $27.8 million prior year [S6]. Additionally, glaucoma system sales (Cyclo G6®) rose modestly to $13.8 million from $12.7 million.

Despite top-line expansion, profitability remained challenged with operating income losses narrowing significantly from negative $8.3 million in 2024 to just negative $2.6 million in 2025 — an approximately 69% reduction in operating losses [F1]. Correspondingly, net losses halved from approximately $8.9 million to $4.4 million year-over-year [F1], with these improvements linked closely to operational efficiencies and cost-saving initiatives including reductions in R&D spending and sales & marketing expenses [S9]. However, cash flows from operations continued in deficit, though improving from negative $7.3 million in FY24 to approximately negative $2.1 million most recently [F1]. Capital expenditures remained generally modest but increased tenfold compared with prior periods signaling selective investments [F1].

This performance reflects IRIDEX's efforts to grow recurring revenues tied to consumable laser probes alongside system sales mainly concentrated within direct sales markets such as the US and Germany supported by distributors internationally [S6], [S10]. The shift toward consumables reflects a classic business model leveraging proprietary product ecosystems for sustained revenue inflows.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -4 | -2 | -3 | 143000 | |

| 2024 | -9 | -7 | -8 | 13000 | +6.9% |

| 2023 | -10 | -7 | -10 | 109000 | -26.8% |

| 2022 | -8 | -10 | -8 | 286000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2026 | -2 | -90.1 |

| 2024 | -7 | -424.9 |

| 2023 | -7 | -100.5 |

| 2022 | -10 | -43.8 |

Source: SEC companyfacts cache [F1].

Data as per latest annual filings reflecting fiscal years ended Jan 3, 2026 and Dec 28, 2024 [F1]

Innovative Technologies Powering Market Differentiation

The core of IRIDEX’s competitive advantage lies in its proprietary MicroPulse® and Endpoint Management™ laser technologies designed to treat sight-threatening conditions such as glaucoma and retinal vascular diseases [S1]. Both differ fundamentally from standard continuous-wave (CW) photocoagulation lasers.

MicroPulse technology emits subvisible laser pulses lasting microseconds, allowing tissue cooling intervals between pulses which confers precise thermal control minimizing collateral damage – a critical feature addressing safety concerns inherent to traditional CW lasers that apply continuous thermal energy risking vision loss due to overtreatment.[S1] Endpoint Management employs an energy delivery algorithm that titrates laser dosage finely based on real-time feedback enhancing treatment accuracy further.

Clinically these innovations result in tissue-sparing therapies that slow disease progression while preserving retinal function better than conventional high-energy CW treatments — readily adopted by ophthalmologists worldwide seeking effective yet safer interventions.[S1]

Product offerings span:

- Cyclo G6® glaucoma laser systems using MicroPulse for intraocular pressure management.

- Retina laser consoles such as IQ532®, IQ577®, PASCAL System supporting Endpoint Management modes.

- Surgical retina lasers like OcuLight® TX and SLx.

The company strategically integrates recurring revenue streams through consumable single-use probes (MicroPulse P3®, G-Probe® family), creating continued demand post-console sale fostering durable customer relationships.[S1] This combination of proprietary technology plus consumable lock-in lines is emblematic of successful med-tech commercialization models sustaining long-term revenues.

Recent Quarter Performance Highlights and Revenue Dynamics

In Q4 FY2025 communications [N1], quarterly earnings showcased further narrowing of operating losses attributed chiefly to robust retina segment growth propelled partly by Pascal System deployments. Sales momentum benefitted from both direct market penetration in key geographies such as the US/Germany and expanding distributor-led international channels.[N2][N3][S6]

While revenue recognition remained consistent with prior periods across product categories—including service contracts—the company noted a material reduction (~69%) in operating income loss relative to Q4 prior year indicating improved operational discipline.[N2]

However, customer concentration remains pronounced with Topcon comprising around one-third of total sales (32%) during FY25 down slightly from previous years [S4][S10]. This dependence amplifies credit risk as Topcon also represents a significant share of accounts receivable (20%). The dynamic interplay between direct sales strength domestically versus reliance on distributors internationally factors into quarterly revenue variability.

Risks from Customer Concentration and Regulatory Environment

IRIDEX reports substantial concentration risk stemming from relying heavily on a single customer—Topcon—which accounted for roughly one-third of annual revenues for consecutive fiscal years ending January 3, 2026 [S4]. Such dependency introduces vulnerability should contract terms change or if Topcon's purchasing patterns fluctuate given its exclusive distribution agreements outside the US.[S21]

Furthermore, regulatory approval pathways pose material uncertainties affecting timing or feasibility of new product launches globally given stringent FDA requirements alongside international agencies overseeing medical devices compliance [S4],[S5],[S27]. Delays or failure obtaining clearances could hinder competitively critical innovations impacting future revenue streams.

Supplier concentration also presents operational risk given limited vendors providing specialized components necessary for manufacturing laser systems [S14]. The company’s ability to mitigate these dependences remains essential for supply chain continuity.

Capital Structure, Cash Flow, and Returns Analysis

IRIDEX began FY26 with liquidity totaling approximately $6.0 million in cash and equivalents complemented by current assets near $25.3 million against current liabilities about $13.2 million yielding a current ratio around 1.9—indicative of short-term solvency continuity [F1],[S7],[S19].

The company maintains an accumulated deficit exceeding $92 million reflecting years of cumulative net losses linked primarily to R&D investments alongside scaling efforts.[F1] Operating cash flows remain negative at approximately ($2.1M) for FY26 despite marked improvement over historical outflows surpassing ($7M) annually.[F1]

Notably capex spending expanded substantially but modestly overall (~$143k), possibly directed toward vital manufacturing upgrades or IT infrastructure aligning with reported cloud ERP investments [S12],[S15].[F1]

No dividends have been issued historically as all available capital continues funding innovation pipelines along with operational needs — consistent with typical med-tech development-stage companies aiming at eventual profitability rather than shareholder payouts.[S25]

Return on equity remains deeply negative at approximately -90%, underscoring ongoing erosion due to net losses despite equity base rebuilding efforts via private placements or convertible note transactions documented recently [F1],[S16],[S20].

Strategic Outlook: Balancing Growth Prospects with Market Constraints

Looking ahead — analysis based on recent earnings calls [N1],[N2] plus fiscal disclosures [S12] — IRIDEX faces a nuanced path balancing promising technology-driven growth against operational constraints including capital access needs.

Key indicators warranting attention include:

- Uptake trajectories for MicroPulse upgrades embedded within existing installed base lasers particularly among glaucoma specialists globally.

- Regulatory approvals pending for expanded geographical markets beyond direct US/Germany focus enhancing distributor networks presence.

- Evolving reimbursement frameworks treating innovative laser therapies incentivizing greater adoption within hospital outpatient departments.

- Potential incremental financing rounds linked either via convertible promissory notes or equity issuance aimed at bolstering working capital amid negative free cash flow phases.

- Sustained efforts controlling R&D spending without stifling pipeline advancement critical given previous cutbacks yet core dependence on differentiated tech innovation.

Overall IRIDEX embodies a classic med-tech profile where proprietary device innovation undergirds commercial progress but must be carefully navigated amidst funding constraints plus concentrated customer risk factors currently constraining margins despite tepid topline growth momentum.

This report synthesizes information exclusively from public filings up to fiscal year end January 3, 2026 ([F1], [S#]) and publicly available news transcripts ([N#]). It is intended solely for informational purposes without investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments