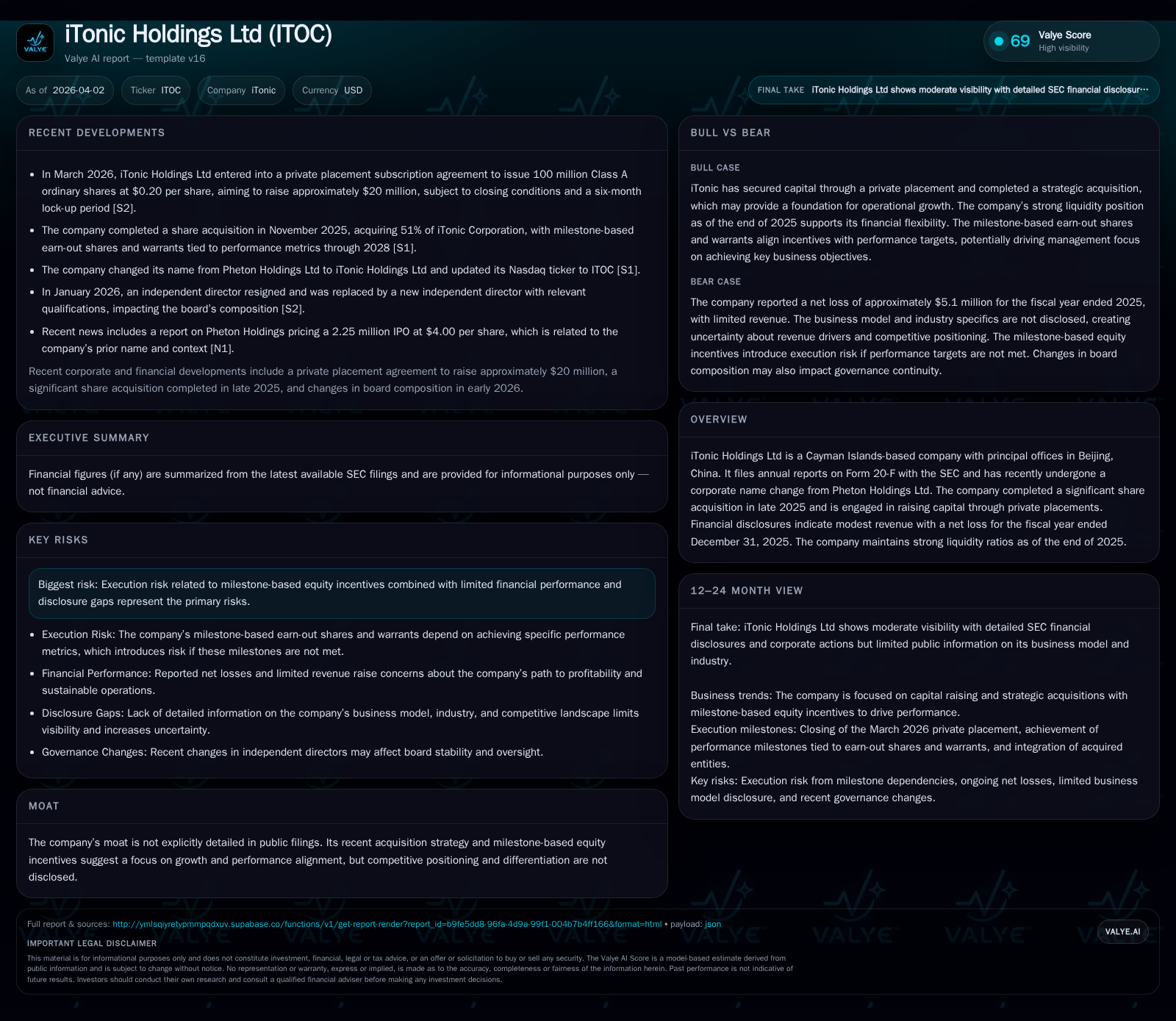

iTonic Holdings’ Volatile Financial Trajectory and Strategic Capital Moves in 2025-2026

iTonic Holdings Ltd's financial results for 2025 reveal a challenging year marked by modest revenue growth but sharply increased losses, alongside key capital initiatives designed to support liquidity and growth.

In 2025, iTonic Holdings reported a 16.7% revenue increase to $523K, contrasted by operating losses exceeding $5 million. The company completed a controlling acquisition late in 2025 with milestone-based equity incentives extending to 2028. A planned private placement in early 2026 aims to raise approximately $20 million to bolster liquidity. Governance changes include independent director turnover and new committee leadership. Despite significant operational cash burn, iTonic maintains strong liquidity supported by a current ratio of 8.83 at year-end. Conservative capital allocation reflects minimal dividends and capex amid ongoing operational challenges.

Revenue Growth Amid Rising Cost Pressures

iTonic Holdings saw its revenues increase by 16.7% from $448K in fiscal year 2024 to $523K in fiscal year 2025, primarily driven by a more than doubling (+103.7%) of sales of Medical Auxiliary Supplies which offset a slight decline (-1.8%) in FTTPS product sales as detailed in the company’s annual report [F1], [S1]. However, gross profit contracted by approximately 14.1%, impacted by cost of revenues rising nearly threefold (+191.9%), suggesting margin pressure from higher input costs or scaling inefficiencies.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 523031 | -5 | -3 | -5 | +16.7% | -671.7% |

| 2024 | 448196 | -1 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 8907 | -3 | -83.3 |

| 2024 | 398444 | -1 | -10.7 |

Source: SEC companyfacts cache [F1].

Table: Revenue and gross profit trends reflect growth tempered by rising costs [F1], [S1].

Escalating Operating Expenses Drive Deepening Losses

Operating expenses increased sharply from approximately $1.15 million in 2024 to over $5.5 million in 2025 (+379%), with general and administrative expenses surging over fivefold (+549%). Selling & marketing and research & development expenses also rose moderately by ~15% and +10%, respectively, contributing to an operating loss that widened from about $770K to more than $5 million year-over-year [F1], [S1]. These trends highlight significant operational leverage challenges amid expansion efforts.

Acquisition and Milestone-Based Equity Incentives

iTonic acquired a controlling interest (51%) in an undisclosed target company during late 2025, structured with milestone-based earn-out shares and warrants exercisable through November 2030 contingent upon performance milestones measured through December 31, 2028 [S6], [S8], [S9]. This framework aligns incentives but introduces execution risk given the extended measurement periods and conditions for equity awards.

Capital Raising via Private Placement

In March 2026, iTonic entered into a private placement agreement to issue up to 100 million Class A ordinary shares at $0.20 per share for aggregate gross proceeds near $20 million, expected to close subject to standard conditions including a six-month lock-up period on issued shares [S2], [S5], [S7]. This capital raise supports liquidity needs amid ongoing losses and funds growth initiatives.

Liquidity Position Remains Robust Despite Operating Cash Burn

iTonic ended fiscal year 2025 with cash and equivalents totaling approximately $1.49 million and current assets around $4.09 million against current liabilities near $0.46 million, resulting in a strong current ratio of about 8.83 signaling solid short-term liquidity despite operating cash flow outflows exceeding $3 million for the year [F1].

Governance Enhancements Amid Transition

The board experienced independent director turnover early in calendar year 2026 with Mr. Yun Fai Wong resigning for personal reasons and Mr. Bin Wu appointed both as his successor on the board and as chair of the Corporate Governance Committee, enhancing oversight capacity during this period characterized by financial stress and strategic transactions [S3], [S12], [S13].

Conservative Capital Allocation Amid Financial Challenges

Capital allocation reflects restraint with nominal dividends paid ($9K) and minimal capital expenditures ($3.8K) during fiscal year 2025 consistent with preserving cash resources amid deep operating losses; no share repurchases are disclosed indicating prioritization of growth funding over shareholder returns currently [F1], [S4], [S6], [S8], [S9], [S10], [S12], [S14].

Outlook Considerations: Key Monitoring Points

Investors should monitor progress on acquisition integration including achievement of performance milestones triggering warrant exercise rights; successful closing and deployment of proceeds from the March private placement; expansion efforts into new medical markets domestically and internationally; evolving governance effectiveness; cost structure optimization; as well as regulatory or competitive developments affecting product adoption dynamics.

This analysis is based entirely on SEC filings up to April 2, 2026 without extrapolation beyond documented figures or disclosures from referenced public sources including filings S1-S17 and companyfacts cache F1.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments