INVO Fertility’s Transition to Clinic-Based ART Services Gains Traction with Recent Acquisitions

Recent SEC filings reveal INVO Fertility's strategic shift from device manufacturing towards a clinic acquisition-led growth model, accompanied by financial restatements that clarify accounting and operational transparency.

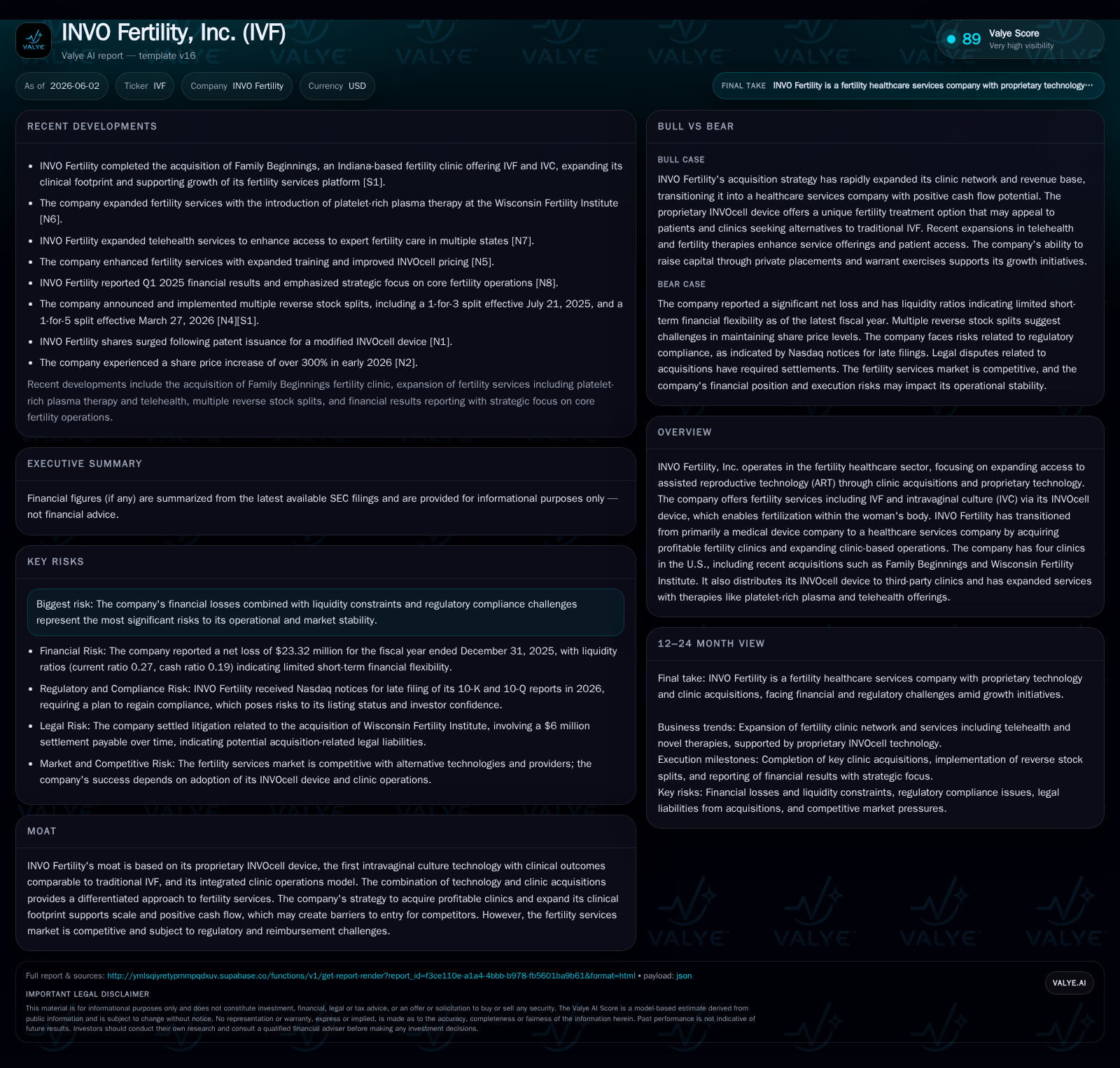

INVO Fertility continues its transformation from primarily a medical device company into a healthcare services provider focused on assisted reproductive technology (ART) clinics. The February 2026 acquisition of Family Beginnings marks another step in scaling its fertility clinic footprint, complementing prior acquisitions such as Wisconsin Fertility Institute. Recent SEC disclosures confirm a technical restatement of prior periods driven by derivative and preferred stock classification errors, which did not affect core revenue or operating losses. The firm’s proprietary INVOcell device underpins its differentiated approach in the competitive ART market, while expansion into ancillary fertility therapies and telehealth broadens service offerings. Liquidity challenges and regulatory risks remain material constraints as the company seeks to leverage clinic-based cash flows toward profitability.

Latest Operational Update: Accounting Restatement and Clinic Acquisition

INVO Fertility’s June 2, 2026 SEC filings highlight two pivotal recent developments shaping its near-term operating narrative. An internal review identified technical accounting errors in derivative instruments and preferred stock classifications during key quarters in 2025. These errors involved mezzanine equity classification for Series C-1 and C-2 Preferred Stock along with embedded derivative bifurcation. Although these restatements prompted corrections to previously issued unaudited financial statements for the March through September quarterly periods of 2025, they did not affect revenues or operating losses reported by the company [S3]. This distinction underscores that the accounting revisions reflect non-operational adjustments rather than fundamental business changes.

Operationally significant is the completed acquisition of Family Beginnings in February 2026, a well-established Indiana-based fertility clinic offering IVF alongside INVOcell-enabled IVC procedures [S6][S8]. The deal structure included purchase consideration partly paid in cash with a substantial portion financed through Series D Preferred Stock issuance. Notably, operational control follows an innovative management services agreement wherein Wood Violet Fertility provides comprehensive non-medical support over an initial decade-long term. This arrangement supports centralized oversight while leveraging existing local clinical expertise, effective March 2026 onward. Complemented by a long-term lease securing physical presence, this acquisition further scales INVO Fertility’s clinic network — vital for generating positive cash flow streams beyond device sales.

Evolving Business Model: From Medtech Device to Healthcare Services Provider

INVO Fertility has strategically transitioned from principally manufacturing and distributing its proprietary medical device to becoming an integrated healthcare services player within ART [S1][S6]. The Wisconsin Fertility Institute acquisition in August 2023 marked the first major pivot — tripling annual revenues by adding an established profitable clinic whose cash flows support operational sustainability. The firm continues acquiring or establishing clinics offering a full spectrum of reproductive technologies: traditional IVF complemented by IVC enabled via INVOcell.

This hybrid approach alters revenue mechanics substantially. Previously reliant on single-unit device sales yielding limited transaction values per patient cycle, the company now derives a larger revenue share from recurring fertility treatment procedures charged at thousands of dollars per cycle across owned clinics. Device distribution persists but occupies a smaller role as complementary rather than core. Additionally, telehealth programs and adjuvant therapies like platelet-rich plasma injections enhance patient engagement and extend the care continuum.

Operational integration also offers margin expansion opportunities since fixed costs associated with laboratory infrastructure can be better leveraged across higher procedural volumes within owned centers. This scalable services platform positions INVO Fertility closer to peer fertility clinic operators rather than typical medtech suppliers.

Product Offering Quality: INVOcell and Complementary Fertility Treatments

At the heart of INVO Fertility’s differentiation lies the patented INVOcell device enabling intravaginal culture (IVC) — an alternative to traditional IVF lab incubation involving fertilization occurring within the woman's vaginal cavity [S6][S13]. Critically, clinical studies have demonstrated pregnancy success rates equivalent to standard IVF with live birth outcomes matching those protocols. The technology avoids costly laboratory incubators thereby reducing overhead and enabling affordability gains.

Furthermore, INVOcell's design places it vaginally rather than intrauterine (in contrast to competing devices like AneVivo or UteroPod), translating into less invasiveness and potentially improved patient acceptance [S13]. In addition to IVC cycles enabled by INVOcell, the company bundles supplemental therapies targeting follicular stimulation optimization — notably platelet-rich plasma treatments — alongside virtual consultations enhancing care access.

This portfolio enriches patient choices while extending average revenue per user (ARPU) through value-added service layers beyond pure laboratory procedures.

Competitive Environment: Positioning Amid Fertility Service Providers

The fertility market is highly competitive comprising entrenched IVF clinics, emerging ART techniques, device makers, and growing telehealth plays [S13]. INVO Fertility competes at an intersection where proprietary technology is integrated into owned clinic operations — a hybrid not widely seen among peers predominantly focused singularly on devices or pure clinical care.

Advantages accrue from:

- Proven clinical equivalence of their unique IVC procedure validated by FDA clearances,

- Diversified procedural mix accommodating lower-cost options which may appeal broadly,

- Geographic targeting of underserved secondary markets where access barriers exist.

Challenges include:

- Maintaining pricing power amid reimbursement fluctuations influenced by managed care consolidations,

- Regulatory exposure tied to simultaneous medical device manufacturing responsibilities,

- Potential encroachment from larger multispecialty fertility providers boasting scale economies.

Overall, while not yet commanding broad market dominance, INVO Fertility’s combined technology plus services model establishes niche positioning that could create durable switching costs if execution succeeds.

Growth Drivers: Clinic Network Expansion, ART Procedure Demand, and Technology Uptake

Growth fundamentally hinges on accelerating high-margin fertility service volumes within acquired/operated clinics paired with selective expansion of INVOcell device adoption externally [S1][F1]. Key levers include:

- Profitable acquisitions such as Wisconsin Fertility Institute (tripled annual revenues upon closing) and Family Beginnings contributing immediate positive operating cash flow,

- Scaling outpatient procedure volumes by leveraging existing referral channels including OBGYN relationships augmented through digital marketing,

- Expanding telehealth penetration which lowers patient access friction while enhancing ancillary therapy uptake,

- Growth opportunities via management service agreements ensuring clinic-level operational scalability without heavy upfront capital investment.

These drivers support improving utilization rates at existing assets; given capacity constraints prevalent industry-wide due to embryologist shortages and lab infrastructure limitations, adding diversified IVC options may unlock incremental procedural throughput.

Risks and Constraints: Financial Stability, Regulatory Landscape, and Integration Challenges

Addressing these challenges is essential for converting scale gains into durable bottom-line improvements.

Monitoring Indicators: Financial Filings, Acquisition Integration Progress, Procedure Volumes, And Reimbursement Trends

Going forward stakeholders should closely watch:

- Timely compliance with Nasdaq-mandated SEC filings following restatement disclosures; submission plans keyed to October 13 deadline seeks to avoid delisting threats [S4][S5],

- Sequential revenue mix shifts emphasizing growing proportion derived from operating clinics versus device sales ticket size,

- Patient procedural volume increases at newly acquired Family Beginnings alongside Wisconsin Fertility Institute metrics,

- Effectiveness of management services agreements delivering operational efficiencies at new clinics without disproportionate costs,

- Changes in reimbursement policies driven by payor consolidation or legislative reform impacting fertility treatment affordability,

- Developments in regulatory environments particularly state-level embryo legislation influencing service provision scope.[F1]

These indicators provide early insight into execution quality supporting valuation rationales beyond headline earnings.

Financial Overview: Accounting Restatement Impact and Balance Sheet Health

Balance sheet liquidity remains strained: current assets totaling approximately $2.76 million against current liabilities exceeding $10 million yields a low current ratio (~0.27), though net debt figures indicate modest indebtedness near $0.9 million last reported accompanied by negative net debt when considering cash balances around $2 million [F1]. Financing arrangements include extended maturity dates on convertible notes facilitated via modifications approving monthly repayments supplemented by warrants issuance for share purchase rights exercisable over several years providing some capital flexibility [S5].

While leverage levels appear manageable relative to operational scale expansion efforts achieved through accretive acquisitions generating positive cash flows at clinic level initiatives remain critical to offset cumulative negative retained earnings nearing $91 million since inception that continue pressuring going concern status acknowledgment [S28].[F1]

Disclaimer: This report is intended solely for informational purposes based on publicly available SEC filings as of June 2, 2026. It does not constitute investment advice or research views.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments