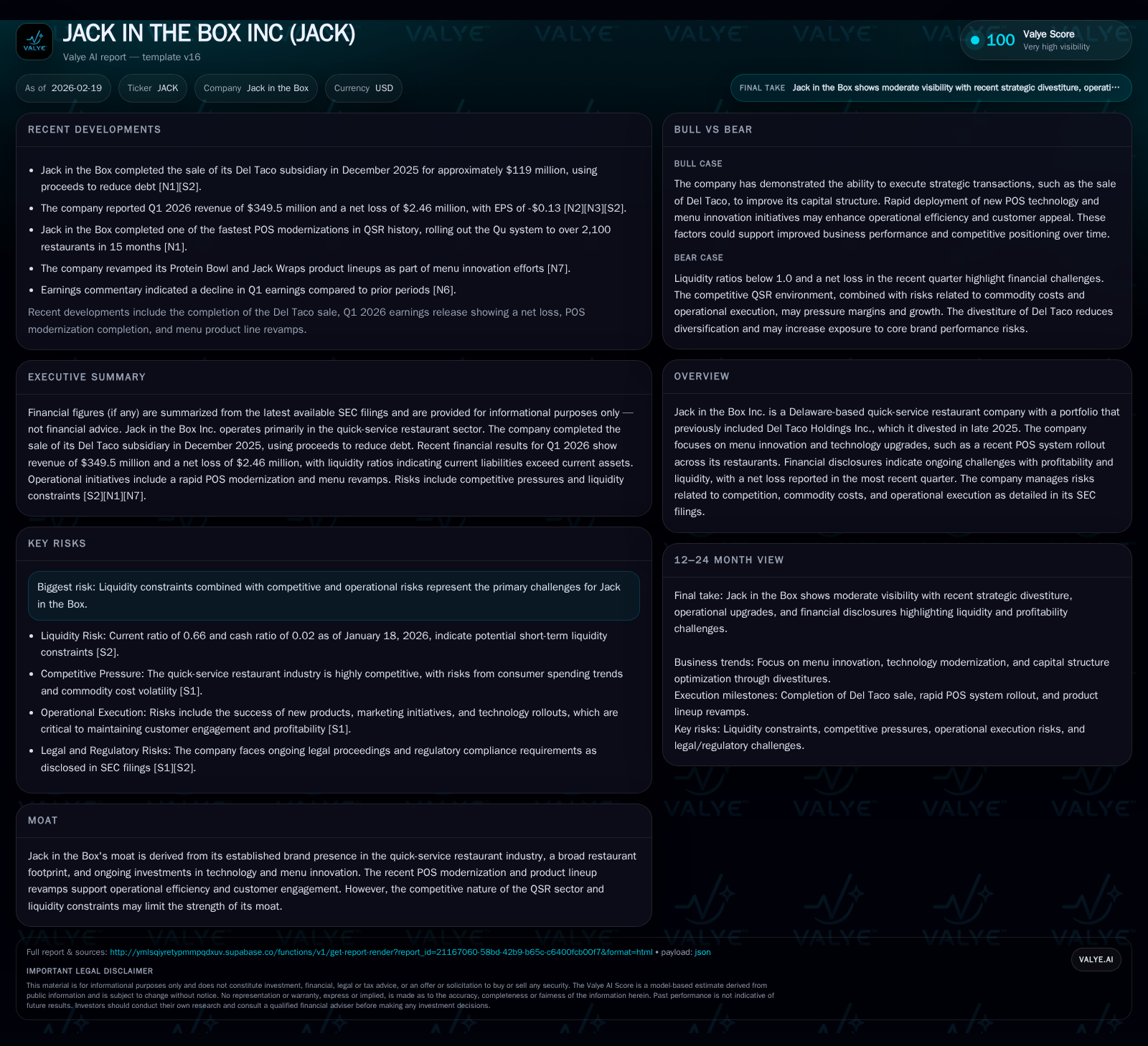

Jack in the Box Faces Profitability and Liquidity Challenges Post-Del Taco Divestiture

The company’s recent divestment of Del Taco and ongoing operational investments shape its growth trajectory amid intensifying QSR competition.

Jack in the Box Inc. has recently completed divesting its Del Taco Holdings stake, focusing solely on its core quick-service restaurant brand. The company’s financials reveal continued pressure on profitability, reflected in a net loss in the latest quarter, despite revenue resilience driven by menu innovation and technology upgrades such as a rapid POS system rollout. Liquidity remains constrained, accentuated by current liabilities exceeding current assets. Capital allocation priorities have shifted towards stabilizing balance sheet leverage and funding menu and digital platform enhancements. Going forward, key growth drivers include operational execution of new product lines and cost management amid a competitive QSR environment.

Historical Financial Performance

Jack in the Box’s top-line revenue experienced a downward trajectory over the past three fiscal years, primarily influenced by significant portfolio changes including the spin-off of Del Taco Holdings Inc. The company’s annual revenue declined from $1.69 billion in FY2023 to $1.57 billion in FY2024 and further down to approximately $1.47 billion in FY2025 — a roughly 6.7% drop year-over-year as reported in SEC filings and company disclosures [F1]. This contraction corresponds with divestitures and a challenging macroeconomic environment.

Operating income showed acute volatility: after peaking at $278.8 million in FY2023, it fell sharply to $82.5 million in FY2024 before turning negative at -$18.1 million in FY2025 [F1]. The swing to operating losses reflects elevated costs likely associated with restructuring post-divestment, inflationary pressures on commodity inputs, and investment ramp-ups particularly in technology upgrades.

Similarly, net income mirrored this adverse pattern, shifting from positive earnings of $130.8 million in FY2023 to losses of -$36.7 million in FY2024 and deepening into -$80.7 million for FY2025 [F1]. Despite headline losses, operating cash flow demonstrated resilience — surging from $68.8 million in FY2024 to $162.4 million in FY2025 due to working capital management improvements and non-cash charges [F1].

Capital expenditures remained material though moderated from previous levels ($115.5 million in FY2024 down to $88.2 million in FY2025), signaling continued reinvestment albeit with greater caution [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1465 | -81 | 162 | -18 | -6.7% | -120.0% |

| 2024 | 1571 | -37 | 69 | 83 | -7.2% | -128.0% |

| 2023 | 1692 | 131 | 215 | 279 | +15.3% | +13.0% |

| 2022 | 1468 | 116 | 163 | 248 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 17 | 5 | 74 |

| 2024 | 34 | 70 | -47 |

| 2023 | 36 | 90 | 140 |

| 2022 | 37 | 25 | 116 |

Source: SEC companyfacts cache [F1].

Note: ROE not included due to negative equity values.

Strategic Shifts: Del Taco Divestiture and Focus Refinement

Late calendar year 2025 marked a pivotal moment with Jack in the Box divesting Del Taco Holdings Inc., receiving approximately $119 million in cash consideration [S25], effectively simplifying its brand portfolio while raising near-term liquidity to service debt issuance tied to securitization structures [S19][S21]. This strategic retrenchment signals an intent to sharpen focus on its core Jack brand amidst competitive pressure.

Concurrent with this corporate action, Jack accelerated technology investments: completing one of the fastest POS modernizations across over 2,100 stores within just fifteen months [N12], aiming to enhance order throughput and data capture capabilities—an essential modernization step given rising consumer expectations for seamless digital interfaces amid omnichannel foodservice trends.

Menu dynamics also received attention: notable revamps of their protein bowl and JackWraps product lines have been launched to invigorate consumer interest with health-forward and variety-oriented options [N13], underscoring innovation as a key battleground for market share gains.

Current Financial Position and Risks

The liquidity profile remains a concern highlighted by current liabilities (approximately $352 million) materially exceeding current assets ($232 million), resulting in a constrained current ratio around 0.66 as per recent quarterly disclosures ending January 18, 2026 [F1][S2]. This configuration poses risks around short-term financing flexibility requiring vigilant working capital management.

Despite operational cash flow strength enabling some capital expenditure support without additional external funding, management curtailed share repurchases drastically—down to about $5 million from historical multi-tens-of-millions—and reduced dividend payouts significantly as part of preserving financial flexibility amidst uncertainty [F1][S14].

The company's risk disclosures emphasize exposure to volatile commodity prices impacting food cost inflation; fierce competition within the quick-service restaurant segment which compresses pricing power; and operational execution risks tied both to integrating technological upgrades smoothly and absorbing shocks related to portfolio realignment post-Del Taco sale [S4]. Potential litigation or regulatory complexities further add layers of uncertainty.

Industry Context Analysis

In the broader quick-service restaurant space where Jack competes against giants like McDonald's, Wendy's, and regional players such as Domino's Pizza ([N4]), sustaining favorable margins demands continuous innovation alongside tight cost controls amid inflationary pressures on labor and commodities — notably beef prices affecting burger-centric menus like Jack’s core offerings.

Technology adoption—such as loyalty apps, mobile ordering platforms integrated with modern POS systems—and drive-thru efficiency initiatives become pivotal differentiators; Jack’s rapid POS deployment serves as a critical enabler here but also raises near-term capital intensity concerns.

Future Growth Catalysts and Constraints

Growth prospects pivot on successfully leveraging new menu items' acceptance while enhancing operational execution efficiency through technology-driven improvements that can reduce wait times and labor costs.

A key constraint will be managing liquidity prudently while balancing investments required for staying competitive against intensified market offerings and potential wage inflation pressures.

No explicit forward guidance or milestones were disclosed beyond commentary on strategic actions; thus investors should monitor quarterly sales trends of revamped products, same-store sales performance excluding Del Taco impact, margin recovery patterns as cost efficiencies materialize, and shifts in capital allocation priorities for updated buyback or dividend plans [N2][N3][S2][S28].

Capital Allocation: Returns Focus Under Pressure

Jack’s return metrics have deteriorated along with earnings losses; approximate equity values are deeply negative (around -$938 million) due largely to accumulated deficit balances post operational losses, complicating traditional ROE calculation but indicating recapitalization needs are pressing [F1].

Operating cash flow strength relative to capital spending provides some buffer (estimated free cash flow roughly $74 million for FY2025) enabling manageable debt servicing given adequate refinancing terms yet posing limits on discretionary shareholder returns currently [F1].

Shifts away from aggressive buybacks toward preserving liquidity underscore the company’s cautious stance – dividends too have been scaled back markedly signaling prioritization of balance sheet stabilization over shareholder payouts at this juncture [F1][S14].

Summary: Balancing Innovation with Financial Stability Post-Divestiture

Jack In The Box faces a nuanced tradeoff between bolstering top-line growth via menu innovation and operational upgrades against mounting profitability pressures exacerbated by structural portfolio realignments following its Del Taco sale.

Rapid POS system modernization marks a clear commitment toward digital transformation aligning with broader QSR industry trends emphasizing convenience and speed.

However, liquidity constraints compel measured capital deployment amid ongoing competitive headwinds; future value creation depends critically on restoring sustainable profits through adept cost control and successful customer engagement with refreshed product offerings.

Stakeholders should track upcoming quarterly reports for clearer signals on margin recovery trajectories, capital structure adjustments (particularly debt maturities), and effectiveness of new menu launches as indicators shaping JACK's strategic path forward.

This analysis is based solely on public disclosures including SEC filings up to February 19th, 2026 ([S1]-[S28]) and recent news articles ([N1]-[N13]) along with companyfacts numerical summaries ([F1]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments