Qwest Corp’s Network Divestiture and AI Ambitions Reshape Growth Prospects

The company’s sale of its Mass Markets Fiber-to-the-Home assets alongside strategic pivot to AI-driven enterprise networking redefines its revenue trajectory and capital priorities.

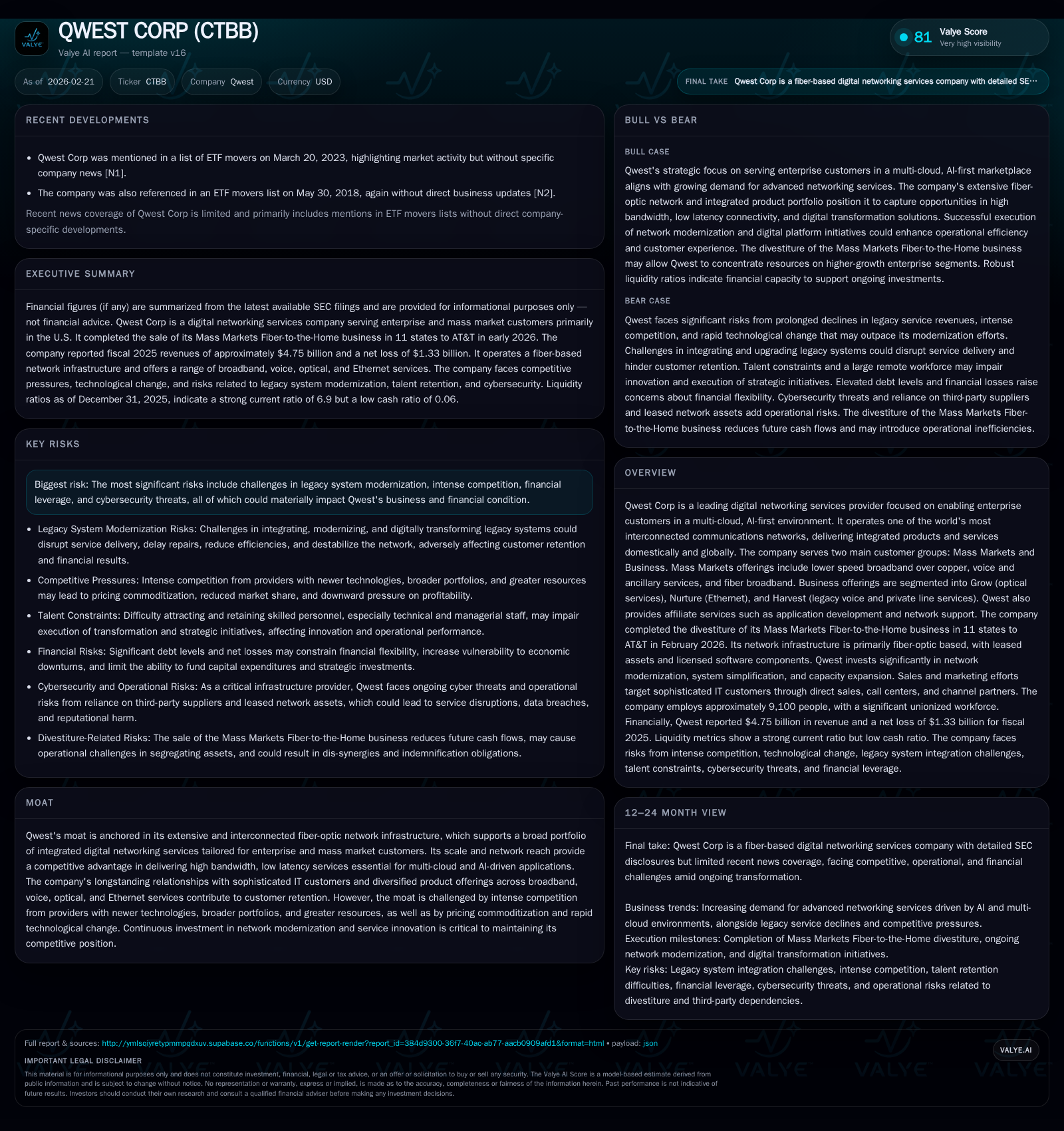

Between 2022 and 2025, Qwest Corp experienced a steep revenue decline from $6.45 billion to $4.75 billion, driven largely by structural shifts including the February 2026 divestiture of its Mass Markets Fiber-to-the-Home business for $5.75 billion. This divestiture has realigned Qwest’s operational focus toward enterprise customers with AI-enabled, multi-cloud digital networking services. While this strategy targets growth in optical and Ethernet segments, challenges persist around legacy system modernization amid intense competition and pricing pressures. Despite a significant operating loss of $1.01 billion in FY2025 and a negative ROE of approximately -12%, Qwest maintains solid cash flow generation and capital discipline as it navigates transition risks and cybersecurity concerns.

Historic Performance: Revenue Decline and Operating Volatility

Qwest Corp's recent financial trajectory reveals a stark contrast between prior growth years and a precipitous decline culminating in fiscal 2025. Revenue decreased substantially from $6.45 billion in 2022 to $4.75 billion in 2025, representing an approximate annual contraction rate of -13.8%. Notably, operating income swung from a robust positive $2.75 billion in 2022 down to a significant operating loss of $1.01 billion by year-end 2025 [F1]. This volatility underscores the impact of structural transitions including asset divestitures as well as operational challenges within legacy businesses.

Net income mirrors these trends with a decline from profitable territory into negative territory reaching -$1.33 billion by FY2025—a roughly -179.7% YoY change—and resulting in an indicative return on equity near -12%, signaling ongoing profitability pressures amid transformation [F1]. These shifts reflect intensified costs associated with divestiture activities, restructuring charges, and the shrinking base of legacy wireline revenues.

Historical performance (annual)

| FY | Rev ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 4.7 | 1.8 | -1.0 | 824 | -13.8% |

| 2024 | 5.5 | 2.2 | 2.1 | 1047 | -6.9% |

| 2023 | 5.9 | 2.4 | -0.2 | 1062 | -8.3% |

| 2022 | 6.4 | 2.6 | 2.8 | 849 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, Buybacks, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 0 | 938 |

| 2024 | 0 | 1147 |

| 2023 | 1980 | 1327 |

| 2022 | 0 | 1777 |

Source: SEC companyfacts cache [F1].

Note: Net income data prior to FY2024 are limited; buyback data unavailable.

Impact of Fiber-to-the-Home Divestiture on Business Model

A watershed moment occurred in February 2026 when Qwest completed the divestiture of its Mass Markets Fiber-to-the-Home (FTTH) business across eleven states to AT&T for net proceeds approximating $5.75 billion [S1][S5]. This transaction drastically reshaped Qwest's mass market footprint by transferring high-speed residential fiber broadband assets outside its control.

Operationally, the divestiture reduces recurring mass market broadband revenues but infuses the company with substantial liquidity to potentially fund strategic investments or debt reduction efforts [S2]. In parallel, Qwest reaffirmed its focus on enterprise networking products encompassing optical transport (‘Grow’) and Ethernet-based offerings (‘Nurture’), intending to leverage its established fiber-optic network infrastructure tailored for demanding multi-cloud and AI-first applications [S3][S16].

While the cash infusion mitigates immediate financial constraints, future cash flows will bear the enduring impact from lost retail broadband streams alongside potential stranded costs arising from transitioning operational systems and network responsibilities during separation [S2]. Furthermore, renegotiating interconnection agreements with third-party carriers becomes integral as service continuity obligations persist amid customer migration.

AI-First Strategy and Enterprise Services: Future Growth Vectors

Post-divestiture, Qwest aggressively pursues an AI-driven model emphasizing integrated digital networking products enabling multi-cloud environments optimized for scalable bandwidth demands and ultra-low latency essential for advanced AI workloads [S3][S17].

Focused mainly on enterprise clientele with sophisticated IT needs, their portfolio segregates into three principal enterprise categories: 'Grow' optical wavelength services delivering end-to-end high bandwidth connections; 'Nurture' mature Ethernet services facilitating metropolitan-scale point-to-point or multipoint transmissions; and 'Harvest' managed legacy voice/private line solutions providing stable—but contracting—income streams [S3].

This structured segmentation reflects deliberate layering designed to migrate clients onto higher value optical/Ethernet offerings while managing legacy attrition cautiously.

Sector-native terms underscore that seamless integration hinges heavily on optical transport technology capable of handling expansive wavelength multiplexing combined with agile Ethernet segmentation architecture—critical infrastructure components for meeting accelerated AI traffic proliferation demands.

Nevertheless, growth assumptions hinge precariously on sustained AI adoption momentum within targeted verticals coupled with continued customer willingness to upgrade networks amidst intensifying competition—a risk factor highlighted by management emphasizing potential misallocation if anticipated demand softens or evolves unpredictably [S17].

Modernizing Legacy Infrastructure Amid Intense Competition

Qwest confronts persistent headwinds upgrading aging copper-wireline infrastructures originally designed for traditional low-speed services while concurrently deploying cutting-edge automated digital platforms supporting virtualized networking functionalities responsive to real-time IT shifts [S1][S8].

Legacy system modernization involves extensive project management complexity including retiring obsolete hardware/software stacks, migrating master data management schemes, introducing self-service digital portals for customers, and embracing emerging technologies like AI internally for operational optimization—all coping with regulatory compliance demands that increase overhead expenses [S8][S12].

Competitive dynamics compound these challenges; many rivals deploy newer network architectures supported by broader product portfolios—ranging from wireless broadband substitutes that undercut copper offerings to hyperscale cloud providers developing proprietary connectivity solutions bypassing traditional carriers altogether [S7]. Such competitors often benefit from deeper balance sheets enabling aggressive R&D investment plus enhanced customer acquisition resources.

Consequently, effective network modernization is not merely technical upgrade but also critical competitively defensive move necessary to avoid further erosion through commoditized pricing pressure or customer churn.

Financial Health: Cash Flow Robustness and Capital Allocation

Amid operational turbulence, Qwest maintained commendable cash flow generation capacity—FY2025 operating cash flow tallied approximately $1.76 billion against capital expenditures constrained at roughly $824 million yielding free cash flow near $938 million for the year [F1]. This favorable cash conversion despite earnings losses reflects disciplined capex management focusing investments on sustaining core network capabilities while trimming non-essential spend.

However, capital allocation exhibits conservative posture given structural transition risks: dividends halted since FY2024 with no share repurchases reported in recent periods marking a shift away from distributing excess capital towards internal reinvestment or balance sheet fortification efforts [F1].

Equity levels remain sizeable at over $10.9 billion but are declining year-over-year consistent with losses absorbed during restructuring phases—further depressing returns equity reflective in negative ROE outcomes near -12% calculated using trailing net income versus equity balances last fiscal year [F1].

Consequently, investors should consider the strained profitability metrics juxtaposed against stable cash flows as emblematic of companies undergoing transformation while preserving liquidity buffers.

Risks: Legacy Systems, Competitive Pressures, and Cybersecurity

Several material risks temper optimism about Qwest's strategic pivot:

- Legacy System Execution Risk: Modernizing complex inherited infrastructure within cost/timing budgets remains uncertain with possible impacts on service stability leading to customer attrition or regulatory penalties if disruptions occur [S8][S9].

- Competitive Intensity: Rapid technological progress coupled with commoditization pressures threatens margin compression especially against competitors wielding superior scale or innovation velocity [S7][S17].

- Cybersecurity Vulnerabilities: As a critical communications provider entwined with federal contracts (including DoD requirements), exposure to sophisticated cyber-attacks escalates—the ongoing necessity to invest heavily in threat detection/remediation systems increases operating costs [S16][S25][S28].

- Labor Relations: Over 40% of workforce unionized creating negotiation complexities which could lead to strikes disrupting operations or increasing labor costs burdensome relative to peers [S4][S8].

- Regulatory Environment: Evolving data privacy laws plus contested legal environments regarding content liability remain persistent overlays shaping compliance expenditures and litigation risk profiles [S9][S12][S20].

Failure to mitigate these risks may significantly hamper ability to realize envisioned benefits from digital transformations ultimately affecting customer retention/revenue stability.

What to Watch: Execution on Digital Transformation and Market Response

Looking forward, close attention should be paid to several key forward milestones post-fiber divestiture:

- Revenue trajectory stabilization—in particular whether enterprise revenue growth offset lost mass market fiber subscriptions.

- Progress reports on legacy system retirements alongside successful deployment of automated digital platforms tailored specifically for AI-centric workloads.

- Any emergent disclosures around customer churn rates within wireline broadband segments affected by competitive displacement.

- Management communication clarifying timelines/budgets related to optical network expansions accommodating forecasted bandwidth surges.

- Capital deployment decisions balancing debt reduction versus innovation investment priorities.

- Cybersecurity incident frequency/severity developments given rising advanced threat environment.

Although explicit financial guidance remains limited at present, these factors collectively will provide meaningful insight into whether Qwest can convert its repositioning into sustainable mid-to-long term growth despite residual headwinds inherent in telecommunications sector disruption dynamics.

This analysis is based solely on publicly available data including SEC filings up to February 20, 2026 ([F1], [S#]) without any forward-looking projections beyond reported information or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments