BWX Technologies’ Growth Hinges on Government Contracts Amid Rising Capex and Debt Leverage

Specialized nuclear and defense technologies sustain BWXT’s moat while political funding risks and capital intensity weigh on future trajectory.

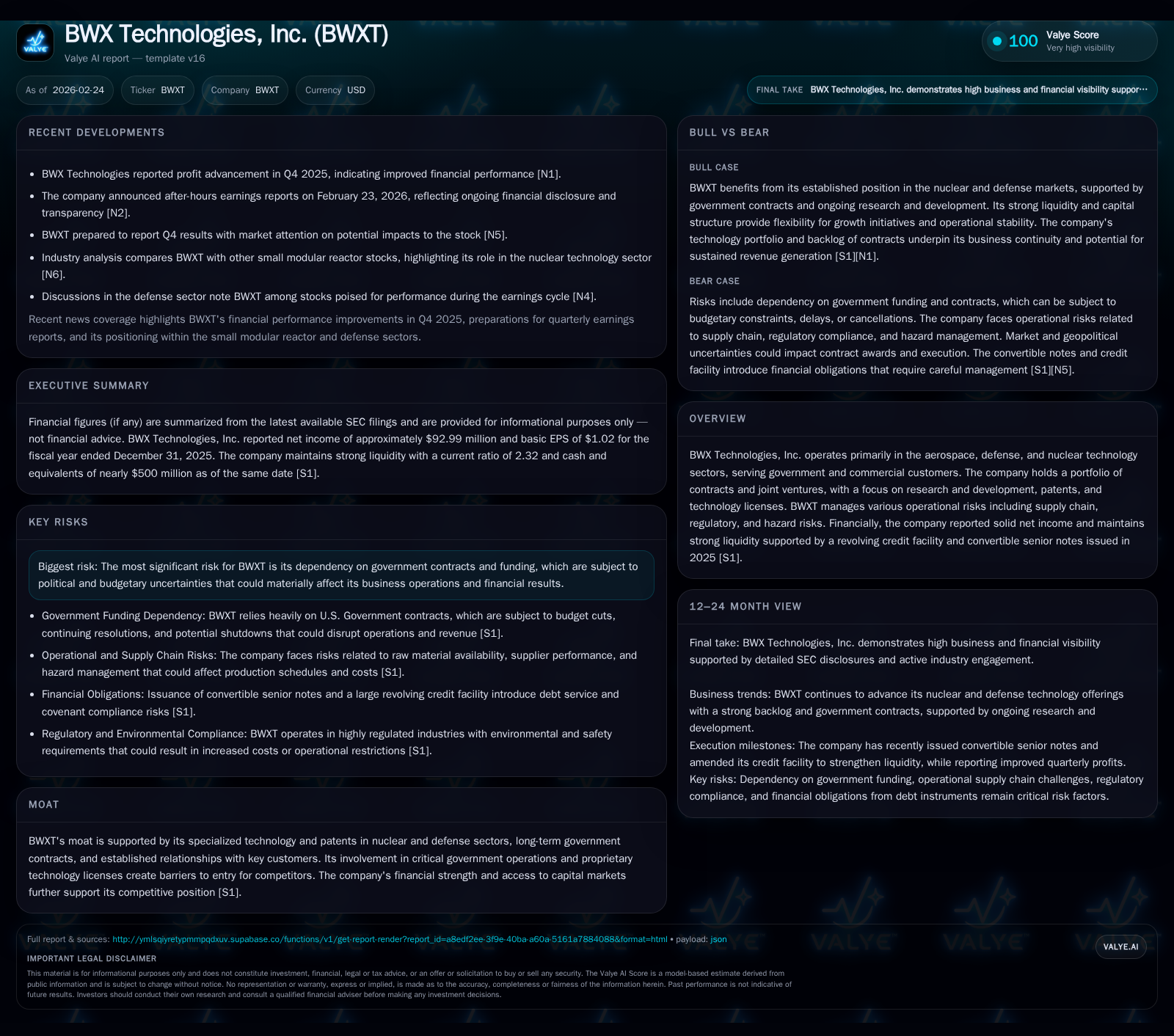

BWX Technologies, Inc. has demonstrated consistent revenue growth driven primarily by long-term government contracts and proprietary nuclear technologies. However, operating income has plateaued recently due to rising costs and increased capital expenditures, reflecting investments in innovation and capacity expansion. The company’s sizeable revolving credit facility and $1.25 billion convertible notes issued in late 2025 enhance liquidity but introduce leverage considerations. Future growth depends heavily on sustained government funding and successful commercialization of emerging nuclear tech, though political budget uncertainties remain a key risk.

Company Overview

BWX Technologies, Inc. (NYSE: BWXT) operates at the intersection of aerospace, defense, and nuclear technology sectors. The company specializes in manufacturing nuclear components for government propulsion programs and provides advanced technological solutions supported by an extensive portfolio of patents and licenses [S1]. Its core operations revolve around long-term contracts with the U.S. government, emphasizing military nuclear propulsion systems alongside commercial nuclear services.

Historical Financial Performance

BWXT delivered moderate but steady revenue growth over recent years despite challenging macroeconomic environments affecting defense spending profiles. Revenue expanded by approximately 6.5% from fiscal year (FY) 2024 to FY2025 reaching roughly $426 million [F1]. This growth has largely been supported by stable contract execution within its Government Operations segment.

While operating income peaked at $123 million in FY2023, it reverted closer to $92 million in FY2024–2025 indicating margin pressure likely from inflationary cost increases and supply chain complexities highlighted by management [S12]. Net income improved significantly by nearly 31% year-over-year to about $93 million for FY2025 as operational efficiencies and possibly beneficial tax impacts offset some cost headwinds.

Cash flow generation remains a bright spot for BWXT with operating cash flow rising consistently over four years to nearly $480 million in FY2025. Free cash flow after capital expenditures — which themselves increased sharply (+20%) to about $185 million reflecting capital investments in manufacturing capabilities and R&D — still amounted to a healthy ~$295 million [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 93 | 480 | 92 | 185 | +30.9% |

| 2024 | 71 | 408 | 92 | 154 | +7.8% |

| 2023 | 66 | 364 | 123 | 151 | +53.4% |

| 2022 | 43 | 245 | 102 | 198 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 30 | 295 | 7.5 |

| 2024 | 20 | 255 | 6.6 |

| 2023 | 0 | 212 | 7.1 |

| 2022 | 20 | 46 | 5.7 |

Source: SEC companyfacts cache [F1].

Note: Historical revenue for years prior to FY2024 not available from provided tags for YoY comparison.

Business Moat and Strategic Positioning

BWXT’s competitive advantage is deeply rooted in its specialized technology base centered on nuclear reactor design and critical defense components protected under numerous patents [S1]. It enjoys entrenched relationships with the U.S Department of Defense and other government agencies due to its unique capability set that few competitors can replicate.

Joint ventures within the sector augment innovation pipelines while long-term government contracts embed visibility into future revenues albeit contingent on governmental appropriation decisions [S6]. The company’s moat is reinforced by regulatory barriers typical of nuclear-related industries alongside proprietary licenses that restrict easy competition.

Growth Catalysts and Constraints

Looking ahead, BWXT’s growth prospects hinge largely on continued U.S government contract awards for naval nuclear propulsion systems — areas where technological upgrading cycles can sustain demand [S1]. Commercial development of small modular reactors (SMRs) is also a potential growth avenue given increasing interest in clean energy alternatives; however, market adoption remains nascent with regulatory approvals posing timelines uncertainty [N10].

Risks remain significant around the company’s heavy reliance on federal budgets subject to political flux including events such as government shutdowns or spending caps [S8][S18]. The debt ceiling debate that led to a partial shutdown in October 2025 illustrated these vulnerabilities could disrupt program timelines or cause payment deferrals impacting financial performance.

Capital Structure and Liquidity Positioning

In November 2025, BWXT issued $1.25 billion aggregate principal amount of zero-coupon convertible senior notes due in 2030 alongside establishing a secured revolving credit facility of equal size expiring in late 2030 [S15][S16]. These moves materially strengthened liquidity buffers enabling working capital flexibility amidst capital-intensive operations but also introduced additional leverage requiring careful covenant compliance.

As of December 31, 2025, the company reported roughly $500 million cash and equivalents with a strong current ratio exceeding 2x indicative of comfortable near-term liquidity coverage [F1]. Covenants tied to total net leverage ratios appear manageable given substantial EBITDA coverage assumptions embedded within the credit agreements but warrant ongoing scrutiny especially given sizable capex plans.

Returns Profile and Capital Allocation

BWXT exhibits an approximate return on equity near 7.5%, reflecting the highly specialized yet capital-heavy nature of its business model [F1]. Despite solid cash flow generation supporting robust internal investment capabilities, dividend distributions remain modest or nonexistent recently with shareholder returns primarily generated through share repurchases totaling $30 million in FY2025 up from lower levels previously.

The inclination towards buybacks over dividends may reflect management’s preference for flexible capital deployment aligned with uncertain federal contracting environments combined with growth reinvestment requirements.

What To Watch Forward (Analysis)

- Contract Awards: Timely receipt of new or renewal government contracts especially within naval propulsion will be critical monitoring points affecting revenue momentum.

- SMR Commercialization: Progress towards regulatory approvals and commercialization partnerships could unlock material new markets but entail technology execution risks.

- Government Budget & Policy: Political developments affecting defense spending levels or procurement cycles pose direct business risks including revenue deferrals or cancellations.

- Debt Metrics: Ongoing adherence to credit facility covenants amid ramping capex demands will impact strategic flexibility.

- Operating Margins: Management effectiveness in combating inflationary cost pressures through productivity improvements will determine profitability resilience.

Conclusion

BWX Technologies stands as a uniquely positioned player leveraging proprietary nuclear technology assets vital to national security missions while cautiously expanding into commercial spheres like SMRs. Solid historical financial performance underscores operational competence but is tempered by sector-specific risks predominantly linked to dependency on volatile federal budgets.

Its strengthened liquidity profile via recent debt issuances supports tactical maneuvers amid increased investment needs but warrants vigilant balance sheet management as macro uncertainties persist.

This analysis reflects data available as of February 24, 2026, sourced from SEC filings and public disclosures without any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments