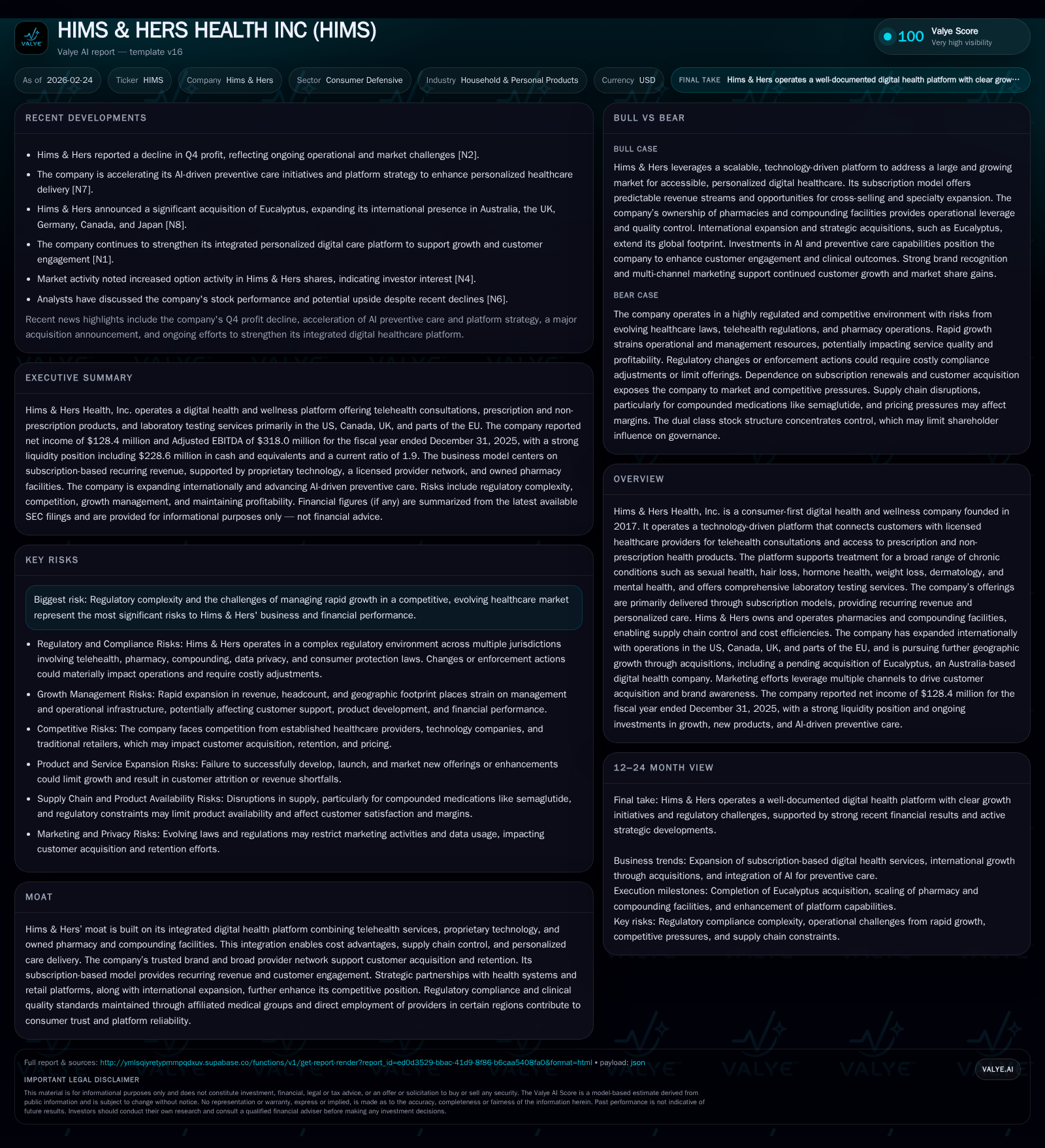

Hims & Hers Health’s Growth Accelerates with Regulatory and Operational Tradeoffs

Hims & Hers leverages an integrated telehealth platform and expanding product offerings while navigating intensifying regulatory scrutiny and capital allocation challenges.

Founded in 2017, Hims & Hers Health, Inc. has developed a digital-first, subscription-based telehealth platform that offers treatment for chronic conditions across sexual health, dermatology, mental health, and more. The company’s growth has accelerated, turning profitable in recent years despite regulatory headwinds and investments in AI-driven preventive care and acquisitions. Significant capex and stock buybacks reflect strategic reinvestment and shareholder return priorities. However, the evolving regulatory environment around compounded pharmaceuticals and telehealth practices presents ongoing risks that could influence future growth trajectories. Close attention to customer acquisition efficacy and regulatory developments will be key milestones.

Company Overview and Historical Performance

Hims & Hers Health, Inc. (ticker: HIMS), founded in 2017, operates a digitally integrated telehealth platform targeting a broad set of chronic health conditions such as sexual health, hair loss, hormone health, weight management, dermatology, and mental health. Leveraging licensed healthcare providers distributed across jurisdictions including the US, Canada, the UK, and parts of the EU (Germany, Ireland, France, Spain), the company conducts over fifty million telehealth consultations since inception [S4].

Unlike traditional healthcare models, Hims & Hers integrates telehealth consultation capabilities with proprietary electronic medical records systems, digital prescriptions fulfilled mostly through wholly owned pharmacies and compounding facilities. This vertical integration supports supply chain control advantages and cost efficiencies aimed at delivering affordable personalized care at scale.

Historically, Hims & Hers endured losses during its early expansion phase but transformed into profitability by FY2024-25. The company delivered operating income of $106M (up 71% YoY) and net income of $128M in FY2025 after swinging to positive territory from negative results in FY2023 (-$29M operating loss) and FY2022 (-$69M operating loss) [F1]. The net income marginally increased 1.8% year-over-year from FY2024 ($126M) to FY2025 [$F1].

Operating cash flow similarly escalated from a negative level (-$26.5M) in FY2022 to a robust $300M by FY2025 (~20% YoY increase). These strong cash flows support aggressive capital expenditures focused on advancing technology infrastructure and pharmacy operations that surged nearly 360% YoY to $243M in FY2025 [$F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 128 | 300 | 106 | 243 | +1.8% |

| 2024 | 126 | 251 | 62 | 53 | +635.3% |

| 2023 | -24 | 73 | -29 | +64.1% | |

| 2022 | -66 | -27 | -69 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 90 | 57 | 23.7 |

| 2024 | 83 | 198 | 26.4 |

| 2023 | 2 | -6.8 | |

| 2022 | 0 | -21.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; Dividends not declared.

Equity grew steadily to $541M by end-FY2025 from $312M in FY2022 reflecting retained earnings accumulation [$F1]. Approximate return on equity stands near 24%, indicative of improving efficiency amid growth.

Business Model and Competitive Positioning

At its core, Hims & Hers delivers consumer-accessible healthcare via a subscription model enabling ongoing recurring revenue streams—a critical financial lever enhancing predictability. Their platform is designed around convenience (mobile apps/websites), stigma reduction for sensitive conditions, evidence-based clinical guidelines adherence via a robust medical advisory board, and engagement tools such as personalized treatment plans supported by proprietary algorithms [S4][S13].

Notably differentiating Hims & Hers is its owned pharmacy network providing medications—including branded generics—and compounding facilities enabling creation of specialty products like semaglutide-based GLP-1 analogs tailored for weight management treatments [S4][N5]. This integration supports margin enhancement through supply chain control but also heightens regulatory exposure.

The brand resonates strongly among millennial consumers with heavy omnichannel marketing spanning social media influencers to traditional media driving new customer acquisition efficiently while reducing stigma barriers associated with conditions like erectile dysfunction or hair loss [S4][N2].

Competition is fierce within telehealth including behemoths like Teladoc/Livongo or dominant pharmacy chains expanding digital services plus tech giants entering healthcare spaces [S28]. Maintaining differentiation depends on brand trustworthiness supported by clinical standards alongside technology investments such as AI-based preventive care tools bolstered by recent acquisition of Eucalyptus Health [N4][N5].

Growth Prospects

Growth hinges primarily on successfully acquiring new customers leveraging expanding condition coverage—beyond core sexual health to dermatology and mental health—and deepening engagement through personalized subscription tiers offering additional wellness products or lab testing services [S4][N2]. International markets beyond current footprints represent incremental opportunity albeit subject to local regulation complexity.

The rollout of AI-driven preventive care platforms via Eucalyptus promises improved engagement through early intervention models potentially increasing Customer Lifetime Value (CLV) if adoption scales well [N5]. Cross-selling across product lines exemplifies market expansion strategy.

However, risks include regulatory scrutiny especially concerning compounded drugs containing GLP-1s like semaglutide where FDA has initiated investigations including referral to DOJ amid concerns about mass marketing unapproved compounded alternatives which may limit product availability or require operational changes impacting margins [S18][S20].

New or evolving telehealth regulations—such as restrictions on asynchronous consults or employment structures impacted by corporate practice of medicine laws—increase compliance complexities constraining scaling speed or adding costs [S9][S21]. Failure to navigate these effectively can impair growth trajectory.

Financial Outlook & What To Watch

While explicit future guidance was not disclosed recently [N1], key milestones include:

- Monitoring regulatory outcomes related to compounded pharmaceuticals enforcement actions which could materially affect product offerings.

- Customer acquisition cost trends amid continuing marketing investments signaled in recent calls suggest efficiency improvements or challenges.

- Integration success of Eucalyptus Health for AI-driven platform enhancements.

- Expansion pace into additional geographies beyond North America and Europe.

- Margins surveillance given significant capex outlays reflecting investment into scale.

- Ongoing evaluation of buyback programs reflecting balance between growth capital needs vs shareholder returns [F1].

Organic user growth metrics coupled with recurring revenue retention rates remain vital signs absent direct revenue disclosure.

Returns & Capital Allocation

Hims & Hers’ near-term financial discipline reflects transition from high-growth losses toward steady profitability with ROE ~24%. The company’s robust CFO generation supports substantial reinvestment: capex jumped to $243M in FY2025 from just $53M prior year driven by technology platform scaling and pharmacy assets buildout [$F1].

Concurrently management returned ~$90M via share repurchases during FY2025 indicating prioritization of cash return while maintaining a strong liquidity profile ($229M cash on hand) with healthy current ratio ~1.9x [$F1]. No dividends have been declared consistent with growth-phase internet-enabled healthcare peers.

Capital deployment balance therefore reflects dual priorities: fueling innovation/market expansion against optimizing capital structure amid competitive pressures.

Regulatory & Legal Risks

Healthcare delivery via digital platforms involves layered legal challenges including data privacy (HIPAA relevance contingent on reimbursements), complex licensing across states/jurisdictions due to corporate practice prohibitions necessitating affiliations rather than direct employment caused structural rigidity affecting speed/costs of provider onboarding [S9][S10][S14].

Significant ongoing investigations focus on promotion/marketing practices surrounding compounded pharmaceuticals particularly semaglutide-related GLP-1 products potentially leading to restrictions impacting supply chain economics [S18][S20]. Adverse rulings or heightened enforcement could require costly operational shifts or impact revenues due to reduction in offerings.

Class action lawsuits are not discounted given public statements from agencies such as FTC inquiries related to business practices; insurance coverage limits exist but may not fully shield against damages affecting financial results materially [S6][S11][S22].

Emerging privacy laws especially internationally around AI use augment compliance complexity; adverse incidents risk reputational harm critical for consumer trust central to brand positioning [S23][S24].

Industry Context (Analysis)

Digital therapeutics combined with telepharmacy are fast gaining prominence within consumer defensive healthcare sectors amidst rising chronic disease burden shifting patient preference towards virtual care models post-pandemic era trends. Subscription models capture higher wallet share than episodic payments but require steady innovation cycles as competitive intensity rises notably from retail giants integrating health services causing margin compression risks if scale efficiencies are not attained.

Growth levers often rely on expanding formulary diversity linking diagnostic capabilities with prescription delivery while optimizing checkout-to-treatment conversion funnels requiring sophisticated omni-channel marketing deploying personalization algorithms anchored on behavioral data — all focal points visible in Hims & Hers’ strategic investments.

Accessibility enabled by asynchronous consult regulations currently grants cost advantages but increased scrutiny introduces uncertainty potentially curtailing flexibility vital for agent scalability.

Conclusion

Hims & Hers stands at an inflection point transitioning from rapid top-line expansion funded by steep investments into a maturing operator balancing growth acceleration against operational execution amid intensified regulatory oversight primarily focused on compounded pharmaceutical offerings related to groundbreaking yet controversial GLP-1 compounds central to weight management therapy gradients.

Their differentiated vertically integrated model combined with strong brand resonance across multiple wellness verticals underpinned sustained profitability metric improvements underscoring robust cash flow generating capability enabling significant reinvestment alongside shareholder returns via buybacks.

Going forward sustained success depends heavily on adept navigation of multi-jurisdictional regulatory challenges, monitoring outcomes of ongoing federal examinations particularly around FDA compound drug oversight plus maintaining disciplined capital allocation balancing innovation spend against margin preservation within an increasingly competitive landscape reshaped by incumbents' digital initiatives.

Disclaimer: This report is for informational purposes only without any investment advice or solicitation implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments