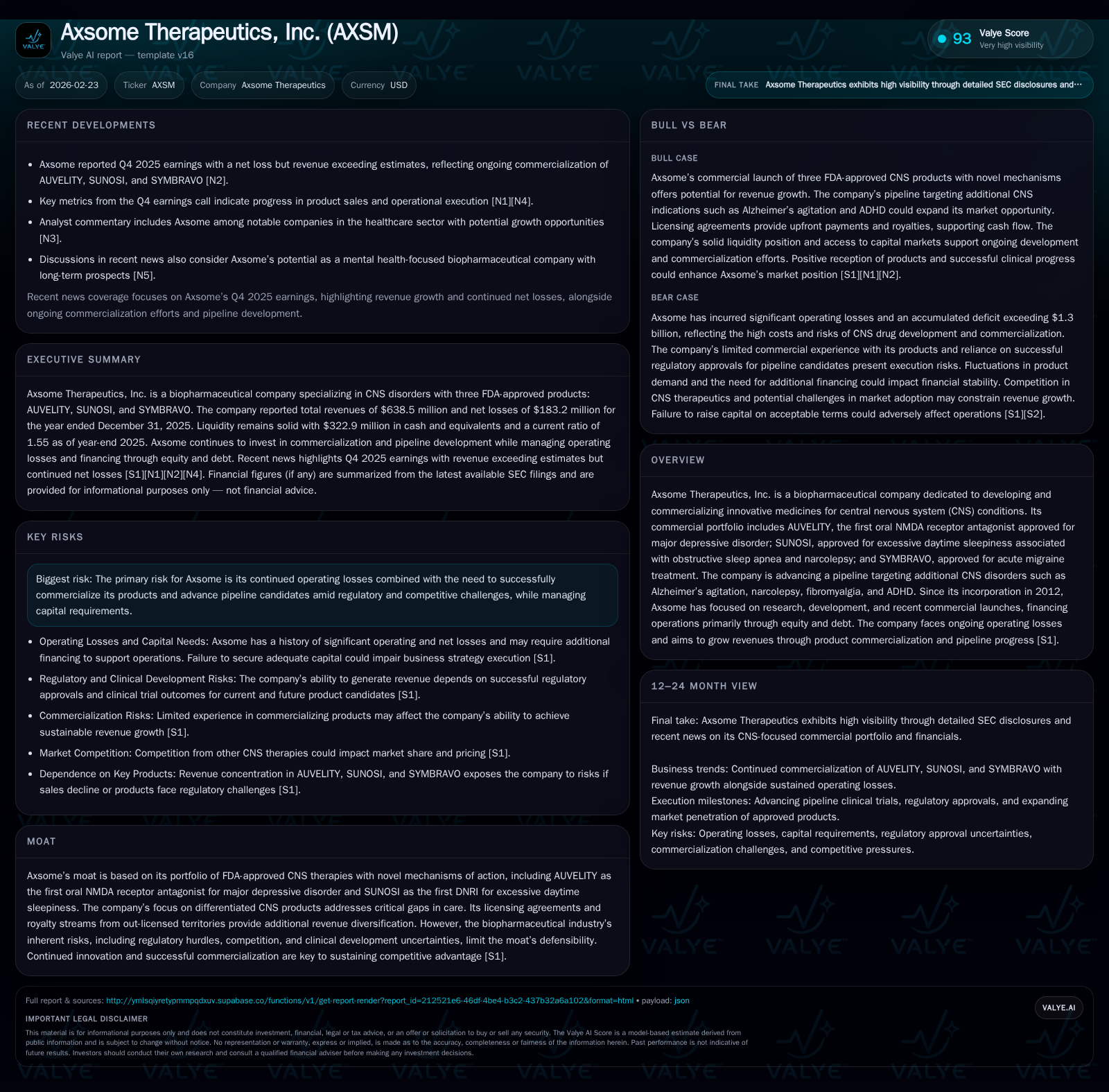

Axsome Therapeutics Charts Post-Launch Growth with Strategic Pipeline Expansion

Axsome advances from clinical-stage to commercial-stage with accelerating revenues from novel CNS therapies amid ongoing losses and capital management challenges.

Since its founding in 2012, Axsome Therapeutics has evolved into a commercial-stage biopharma focused on CNS disorders, propelled by pioneering FDA approvals including AUVELITY for major depressive disorder. Revenues jumped 65.5% from $385.7 million in 2024 to $638.5 million in 2025, driven primarily by product launches and ramping commercialization efforts. Despite this growth, the company remains unprofitable with a net loss of $183.2 million in 2025 and negative operating cash flow due to sustained R&D investments and commercial infrastructure build-out. Axsome’s pipeline targets high-unmet-need CNS conditions such as Alzheimer’s agitation and fibromyalgia, representing critical future growth drivers. Capital structure reflects active equity raises and new debt facilities supporting cash runway, although ongoing operating losses and legal proceedings impose execution risks. Monitoring quarterly demand trends, clinical trial readouts, and liquidity indicators is key for assessing near-term trajectory.

From Development to Market: Examining Axsome’s Historical Performance

Axsome Therapeutics’ financial evolution reveals a classic biotech transition from a development-focused enterprise burdened by heavy losses toward scaling commercial revenues amid persistent profitability pressures. Founded in 2012, the company prioritized innovation for central nervous system (CNS) disorders, culminating in the recent approvals of its differentiated portfolio products [S1].

The company reported revenues increasing robustly from $385.7 million in FY2024 to $638.5 million in FY2025—a year-over-year growth rate of approximately +65.5%—driven primarily by commercialization of its three approved products AUVELITY (an oral NMDA receptor antagonist), SUNOSI (a dopamine-norepinephrine reuptake inhibitor or DNRI), and SYMBRAVO (acute migraine treatment) [F1][S1]. This top-line expansion marks a key inflection after years of R&D investment.

Operating income demonstrated improvement but remains negative at -$166.8 million in 2025 compared to -$280.6 million the prior year, an approximate 40.6% reduction in operating loss magnitude illustrating gains from scale economies combined with refractory commercialization expenses still associated with nascent product launches [F1]. Net losses narrowed similarly from -$287.2 million to -$183.2 million during the same period.

The cash flow profile reflects continuing negative operating cash flow at -$93.4 million for FY25 versus -$128.4 million the previous year, consistent with increased but disciplined spending as Axsome ramps marketing efforts while investing heavily in pipeline clinical trials [F1]. Capital expenditures remain modest (~$480k in FY25), underscoring an asset-light business typical of specialty pharmaceuticals focused on drug development and commercialization without heavy manufacturing infrastructure.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -183 | -93 | -167 | 480000 | +36.2% |

| 2024 | -287 | -128 | -281 | 270000 | -20.1% |

| 2023 | -239 | -145 | -232 | 582000 | -27.8% |

| 2022 | -187 | -117 | -180 | 702109 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -94 | -207.5 |

| 2024 | -129 | -503.8 |

| 2023 | -146 | -125.3 |

| 2022 | -117 | -170.8 |

Source: SEC companyfacts cache [F1].

Notes: Operating income YoY calculated between FY24 and FY25 only due to data availability; FY23 revenue not disclosed; net CFO year-over-year computed where applicable.

Commercial Portfolio Momentum Driving Revenue Growth

Axsome's commercial traction originates from its uniquely positioned CNS therapies addressing substantial unmet needs through novel mechanisms of action [S1]. The flagship product, AUVELITY, stands out as the first FDA-approved oral NMDA receptor antagonist for major depressive disorder (MDD). This mechanistic innovation provides an alternative to traditionally prescribed antidepressants targeting monoaminergic systems.

SUNOSI complements this innovation set as the first dopamine-norepinephrine reuptake inhibitor authorized for excessive daytime sleepiness linked to obstructive sleep apnea and narcolepsy; its differentiated pharmacology addresses gaps left by stimulants historically used off-label.

SYMBRAVO recently entered the market as an oral fixed-dose combination approved for acute migraine treatment with or without aura—a prevalent yet often undertreated CNS condition.

The company discloses that quarterly demand volatility can be significant across these specialty pharma products due to insurance reimbursement dynamics and physician prescribing behaviors, necessitating careful management of supply chain — particularly chemical manufacturing controls which remain under scrutiny due to recent litigations surrounding NDA disclosures associated with SYMBRAVO’s manufacturing processes [S4][N3]. Nonetheless, revenue contributions from these agents have scaled substantially, underpinning top-line growth.

Operational Challenges and Profitability Headwinds

Despite impressive revenue gains, Axsome continues to confront extensive operating losses reflecting investments necessary for long-term competitiveness within the biopharmaceutical landscape [F1][S1]. The reported net loss of $183 million in FY25 aligns with elevated R&D expenditure supporting multiple pipeline candidates progressing through various stages of clinical trials — including ongoing Phase II/III studies requiring costly third-party contract research organizations.

Commercial expenses also balloon as shipping logistics expand beyond initial go-to-market phases toward broader physician outreach programs and patient support initiatives designed to foster adoption amidst competitive CNS therapy options.

Operating cash flow remains negative ($93 million), emphasizing the need for continuous funding alongside no dividend declarations or share repurchases observed historically [F1][N1]. The asset-light nature results in relatively low capex (~$480k), consistent with outsourcing much manufacturing and third-party service provision common among specialty pharma firms emphasizing molecule innovation over physical plant investment.

Pipeline Innovations Targeting CNS Disorders Beyond Current Labels

Axsome’s strategic focus on expanding indications beyond current approvals situates it at an intersection where robust unmet medical needs converge with opportunities for mechanistic breakthroughs [S1][N3]. Key pipeline candidates address diverse CNS indications including Alzheimer's disease-related agitation—a condition lacking effective FDA-approved treatments—which could represent significant commercial upside if regulatory hurdles are overcome.

Additional programs target fibromyalgia and attention deficit hyperactivity disorder (ADHD), complementing existing expertise while diversifying risk away from single asset dependency.

Successful clinical trial readouts and subsequent FDA filings will be decisive inflection points influencing valuation trajectories and potential licensing partnerships or acquisitions.

Capital Structure, Financing Activities, and Liquidity Position

Supporting Axsome’s operational ambitions is a capital structure balancing equity infusion and debt financing to provide ample runway through costly commercial scaling and clinical development phases [S6][F1]. In June-July 2023, the company completed an underwritten public offering netting approximately $243M gross proceeds ($211M plus exercised underwriters option), significantly enhancing liquidity vis-à-vis prior years’ offerings.

Throughout FY25, additional ATM equity issuances generated roughly $52 million, demonstrating active use of shelf registration flexibility for opportunistic capital raising without undue dilution shock.

Debt financing transitioned sharply following May 2025 when Axsome entered into a loan agreement with Blackstone Alternative Credit Advisors securing up to $570 million aggregate loans inclusive of term loans ($120 million drawn) and revolving credit facilities [$70 million revolver fully repaid early 2026] [S8][S9]. Loan instruments carry floating interest rates indexed to Term SOFR plus margins circa 4–4.75%, reducing overall cost compared with previous Hercules loan arrangements discontinued upon repayment.

At fiscal year-end December 31, 2025, consolidated liquidity stood at over $322 million in cash equivalents with a strong current ratio near 1.55 indicating adequate near-term solvency given anticipated expenditure profiles [F1]. However ongoing losses demand vigilant capital management amidst market uncertainties.

Equity holders’ book value reflected a moderate accumulation at ~$88 million end-FY25 relative to historical levels aligned with net loss offsets [F1]. No dividends or share buybacks evidence capital prioritization toward growth initiatives rather than shareholder returns currently.

Regulatory and Legal Risks Impacting Strategic Execution

Axsome faces notable regulatory compliance challenges rooted predominantly in securities litigation connected to disclosures about chemical manufacturing controls (CMC) associated with SYMBRAVO's New Drug Application filing process [S4][S5].

A securities class action initiated May 2022 alleges misleading omissions impacting investor assessment timelines; partial motions to dismiss succeeded though certain claims proceed toward potential settlement approvals anticipated imminently post-February 10, 2026 hearing outcomes [S4].

Concurrent stockholder derivative actions parallel these allegations focusing on fiduciary duty breaches among select officers; motions currently pending judgment affecting timing uncertainties meanwhile absorbing management attention [S4].

Risk factors also point to potential impacts on operational bandwidth amid resource diversion toward legal defense notwithstanding management affirming non-material impact on company financial position thus far.

Additional patent infringement litigation involving SYMBRAVO manufacturing patents introduces further uncertainty though believed manageable absent material adverse effects per disclosures [S24].

What to Watch: Upcoming Milestones and Analyst Perspectives

Looking forward, critical catalysts informing Axsome’s trajectory span both regulatory milestones—such as potential FDA submissions or decision dates tied to Alzheimer’s agitation programs—and commercial demand monitoring across core products sensitive to reimbursement dynamics prevalent in CNS pharma markets [N11][N14].[N2]

Analysts emphasize variability risks associated with quarterly prescribing patterns influenced by payer policy fluctuations while remaining cautiously optimistic given novel drug mechanisms addressing underserved patient subsets.

Legal settlement outcomes will bear significant influence over market sentiment given dilution risk concerns intertwined with potential settlement payments or structural governance changes.[N11]

Cash flow metrics subsequent quarters will signal durability of recent operational improvements amidst impending increased trial costs expected per guidance.[S2]

Valuation Considerations and Risks for Buy-Side Investors

From a valuation standpoint, Axsome Thermapuetics offers distinct exposure via its differentiated CNS franchise characterized by first-in-class mechanisms against major depressive disorder and sleep disorder indications underscored by FDA approvals ensuring tangible revenue streams today.[S1]

However, sustained operating losses translating into negative ROE estimated around -207%, alongside high clinical development execution risk common within biopharma sector genetics,[F1] temper risk-adjusted return expectations.[F1]

Capital dilution remains relevant given ongoing financing needs despite sizable recent equity raises complemented by structured debt replacing costlier borrowings.[S6][S8]

Pending legal proceedings reflect downside risk not fully priced yet requiring scrutiny particularly regarding timing uncertainty which could disrupt strategic focus.[S4]

Investors should monitor evolving competitive landscapes within CNS markets where novel pharmacology competes aggressively against established therapies while factoring volatile clinical trial outcomes intrinsic to drug pipelines targeting neuropsychiatric illnesses.

This analysis was prepared using widely available sources including SEC filings ([F1], [S#]) and recent news reports ([N#]). It is intended solely for informational purposes without providing investment recommendations or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments