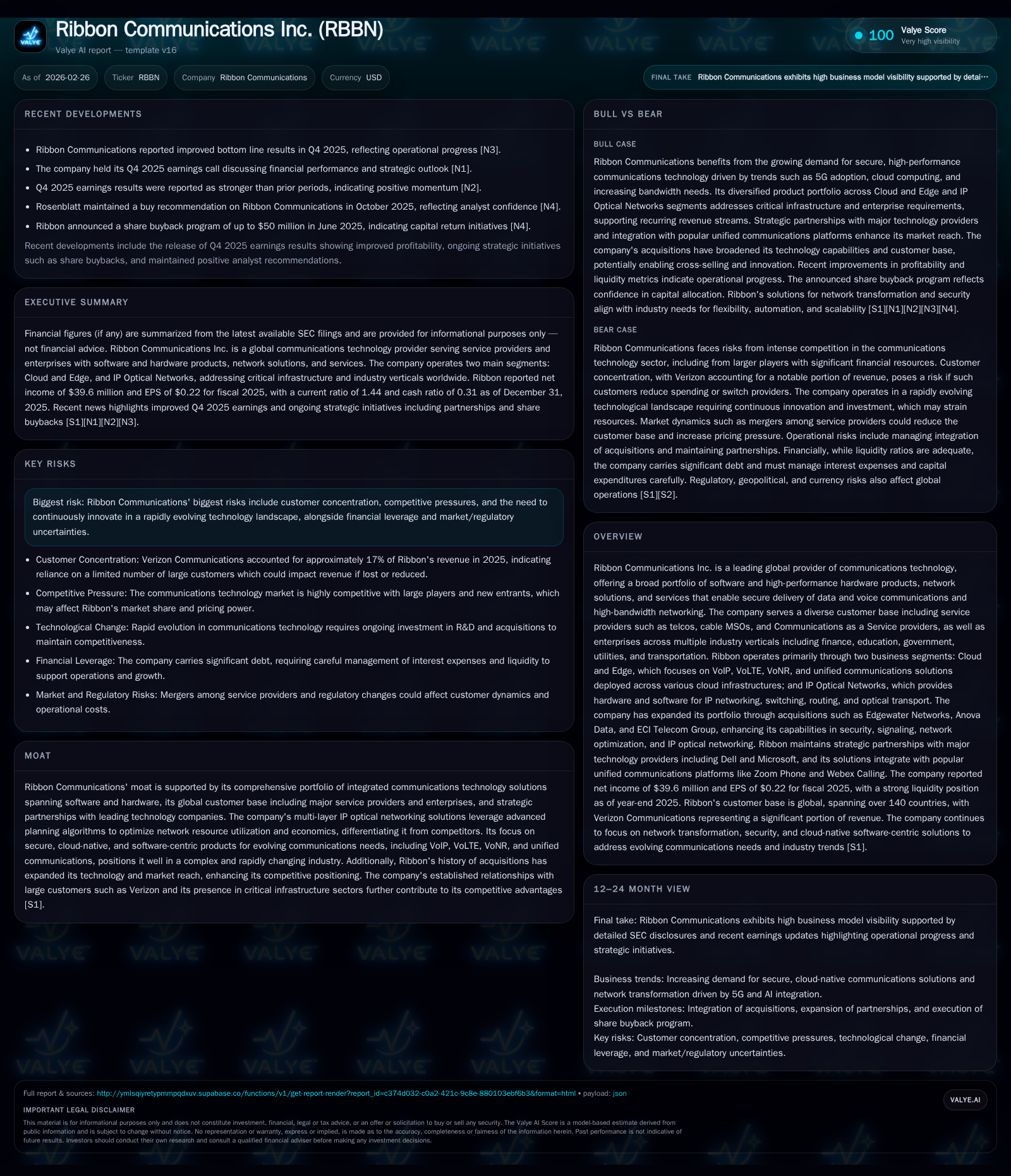

Ribbon Communications Battles Growth Pressures While Leveraging Multi-Layer IP Optical Networks

Ribbon Communications' 2025 financials reflect sharp profit swings amid strategic refocus on cloud-native voice and optical networking solutions.

Ribbon Communications Inc. operates two primary business segments — Cloud and Edge, and IP Optical Networks — serving telecom providers and enterprises globally. While revenue showed a slight decline in recent years, the company delivered a notable net income rebound in 2025 driven by operational efficiencies and a diversified product portfolio. Ribbon’s comprehensive solutions in VoIP, 5G voice services, and integrated IP optical networks place it well to capitalize on evolving carrier network modernization trends, though competitive intensity and customer concentration remain critical challenges. Capital allocation remains prudent with ongoing investments into R&D and modest share repurchases.

Company Overview

Ribbon Communications Inc. stands as a global provider specializing in telecommunications technology that enables secure data and voice exchanges alongside high-bandwidth networking. The company primarily operates through two business segments: Cloud and Edge — focusing on cloud-native VoIP services such as VoLTE (Voice over LTE), VoNR (Voice over New Radio/5G), unified communications (UC), and IP Optical Networks — delivering hardware/software solutions for IP switching/routing and optical transport tailored for service providers and enterprise clients [S7][S8].

With clientele spanning over 140 countries, Ribbon serves major tier-1 carriers like Verizon (accounting for ~17% of company revenue in FY2025) alongside cable MSOs, communications service providers (CSPs), enterprises across sectors like finance, utilities, government agencies, and transportation [S4][S5]. This diverse base underscores reliance on a concentrated but broad portfolio.

Historical Financial Performance

Ribbon's revenue trajectory over recent years reflects industry cyclicality with moderate declines aligned with technological transitions among customers from legacy TDM/MPLS networks toward cloud-centric infrastructures:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 40 | 51 | -3 | +173.1% | ||

| 2024 | -54 | 50 | 17 | -866.1% | ||

| 2023 | 226 | 7 | 17 | 17 | -3.1% | -65.4% |

| 2022 | 234 | 20 | -26 | 1 | +1.3% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 26 | 8.8 |

| 2024 | 28 | -13.4 |

| 2023 | 8 | 1.6 |

| 2022 | -37 | 4.0 |

Source: SEC companyfacts cache [F1].

Revenue is only available through FY2023 per last audited figures [F1]. Operating income declined markedly between FY2024-25 even as net income rebounded substantially likely due to non-operational items or tax benefits not detailed here [F1].

Profitability fluctuations mirror investments into product development alongside effects from integrating acquired businesses such as ECI Telecom Group (acquired March 2020). Operating cash flow improvement between FY2023-25 illustrates stronger working capital management or operating efficiencies despite capex increases to expand cloud-native architecture capabilities [F1].

Business Segments & Market Dynamics

Cloud and Edge Segment

This division focuses on software-driven voice solutions enabling service providers’ transitions from legacy voice infrastructure to modern VoIP-based systems securely deployed in private/public/hybrid clouds [S4]. Products address network transformation needs including:

- Supporting Voice over LTE/5G (VoNR) via IMS core implementations.

- Enhancing interconnect security among telecom operators.

- Enabling secure UC platforms interfaced with Microsoft Teams, Zoom Phone, Webex Calling.

- Protecting premises-based/contact center applications leveraging vendors such as Five9 or Genesys.

Industry tailwinds include CSP efforts to reduce total cost of ownership by virtualizing network functions while maintaining strict security compliance especially among government sectors [S7][S10]. Competition arises from incumbent telecom giants pivoting to cloud-native offerings alongside emerging pure-play software vendors [S15].

IP Optical Networks Segment

Focused on hardware/software combinations facilitating IP routing, metro-regional-long haul optical transport via technologies like DWDM-based OTN (Optical Transport Network), the segment addresses burgeoning data traffic demands from video streaming, e-commerce, connected devices, and increasingly AI/LLM-powered applications [S8][S19].

The segment competes with heavyweights like Ciena, Cisco, Juniper Networks but differentiates through:

- Multi-layer integrated optimization combining control plane intelligence across IP/optical layers.

- Cloud-compatible SDN orchestration enabling automated service provisioning.

- Advanced service lifecycle management geared towards accelerating time-to-revenue.

The segment targets growing regional carriers supported by US federal funding aimed at improving underserved market connectivity [S10].

Strategic Initiatives & Industry Positioning

The company's corporate strategy emphasizes operational integration post acquisition with centralized leadership over sales, R&D, customer support aiming for cross-selling synergies across expanded product sets [S11]. Notable points include:

- Targeting modernization of service provider networks displaced by aging TDM-centric equipment.

- Expanding recurring revenue streams tied to SaaS/cloud deployments.

- Broadening partnerships with key platforms such as Dell Technologies and Microsoft complementing their UC&C products.

- Growing brand awareness amidst stiff legacy vendor competition shifting into software-centric paradigms.

Ribbon also leverages industry standards leadership such as STIR/SHAKEN for call authentication combating robocalls helping improve service provider customer experiences [S15][S23].

Risks & Competitive Challenges

Key risk factors remain customer concentration with the top five clients accounting for roughly two-fifths of sales [S4][F1], coupled with intense rivalry from entrenched global suppliers including Ericsson, Huawei, Nokia adapting rapidly to cloud native needs [S19]. Regulatory shifts affecting telecom infrastructure procurement alongside rapid technological change require sustained innovation investments risking margin pressure.

Financially, managing leverage through credit facilities maturing beyond FY2024 provides runway but mandates prudent capital allocation [S6][S12][F1].

Capital Allocation & Returns

While direct dividend payments are not noted in filings or news sources within the provided information set, Ribbon has actively engaged in share repurchase programs recently amounting to $8.9 million in FY2025 which supports share price stabilization efforts amid volatile earnings [F1]. Capital expenditures rose moderately supporting technology upgrades essential for competitive positioning especially around cloud-native software platforms.

Operating cash flow has shown resilience at over $51 million most recently enabling positive free cash flow (~$26 million) which underpins continued R&D spend alongside shareholder-oriented actions without excessive reliance on external financing [F1]. Return on equity approximates near 9%, indicating reasonable capital efficiency given operating environment challenges.

Outlook & Indicators To Watch (Analysis)

No explicit forward guidance or milestones were disclosed within the reference documents or recent news call summaries up through Q4 FY2025 earnings reports [N1][N2][N3], leaving investors reliant on monitoring:

- Revenue stabilization or growth signals particularly within Cloud & Edge recurring revenue expansion amid Telco Cloud deployments.

- Margins recovery post negative operating results seen in FY2025 driven by product mix shift or operating leverage gains.

- Customer concentration dynamics – any diversification beyond Verizon dominance could materially affect risk profile.

- Market adoption pace of new AIOps automation suites improving network operations efficiency where Ribbon competes against broader ecosystem players.

- Success integrating previous acquisitions fully unlocking synergies especially in optical transport hardware/software business lines.

Conclusion

Ribbon Communications situates itself at a challenging inflection point within telecommunications evolution — balancing simultaneous demands of sustaining legacy revenues while aggressively innovating cloud-native voice/data networking solutions tailored for next-generation carriers and enterprises alike. Its rich portfolio spanning software-defined networking orchestration atop integrated multi-layer IP optical networks constitutes a defensible position amidst ongoing industry disruption.

Financially exhibiting mixed signals yet underpinned by solid cash flows supports this transition phase although risks linked to client concentration plus robust competition remain pivotal watch points making execution critical going forward.

This analysis is based solely on publicly disclosed information up to February 26, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments