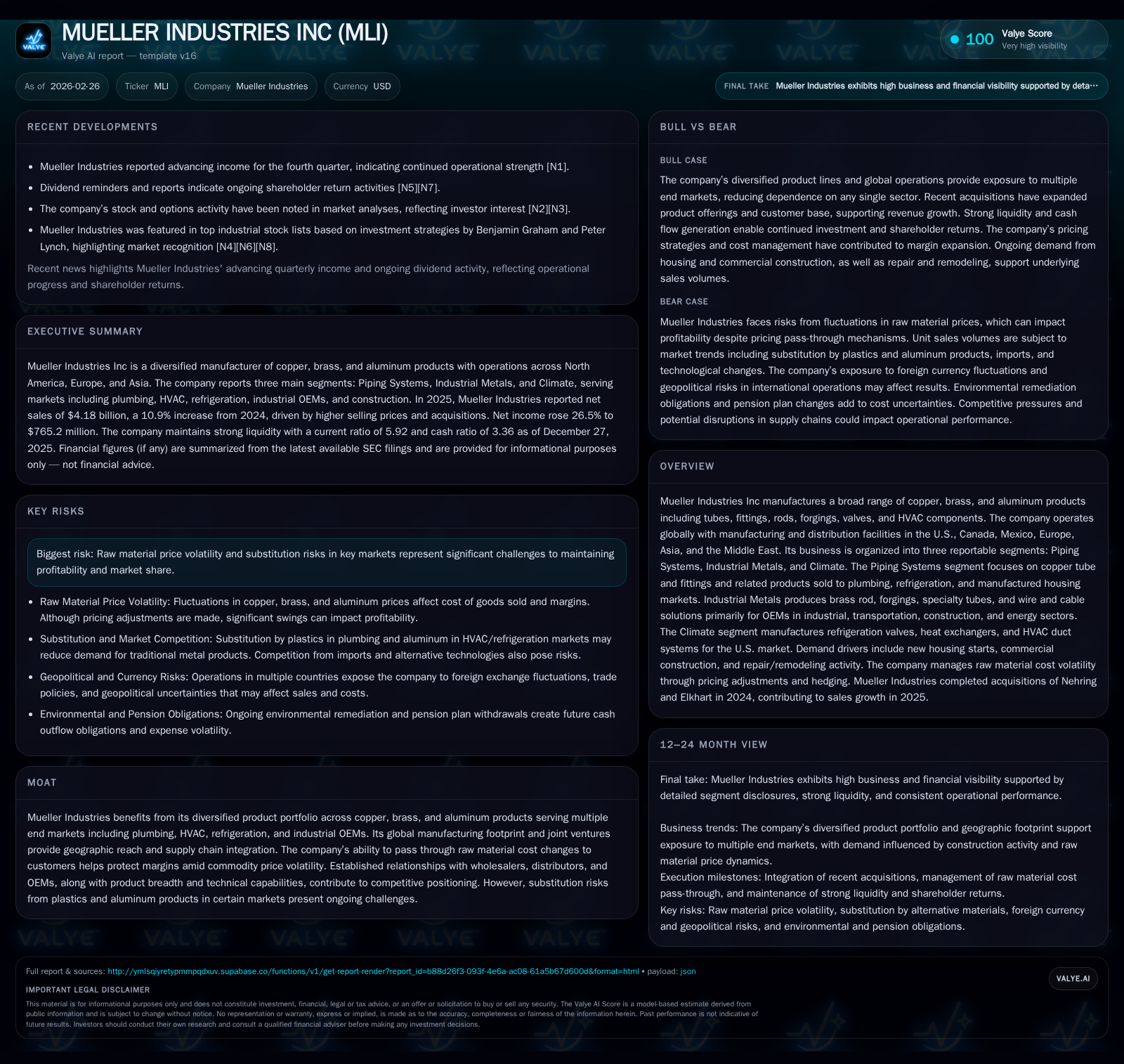

Mueller Industries Inc’s Strategic Expansion Through Diverse Metal Products and Global Reach

Mueller Industries leverages a broad metals product portfolio and global operations to drive strong earnings growth and resilient margins despite raw material volatility.

In 2025, Mueller Industries delivered a remarkable net income increase of over 455% year-over-year, fueled primarily by effective cost pass-through strategies amid fluctuating raw materials prices and strategic acquisitions. The company’s diversified segments—Piping Systems, Industrial Metals, and Climate products—each contributed to top-line expansion against a backdrop of cautious volume declines and price-driven revenue uplift. Its expansive global footprint and supply chain integration underpin competitive advantages, while capital allocation emphasizes aggressive share repurchases and steady dividend growth. Key risks center on tariff uncertainties and substitution threats from plastics and aluminum alternatives in core markets.

Historical Revenue and Profit Trajectory: A Closer Look at 2023–2025

Mueller Industries demonstrated outstanding financial progression over the past three fiscal years with a particularly striking leap in net income for 2025. Total revenues advanced from $3.42 billion in 2023 to $3.77 billion in 2024 (+10.2%) and further to $4.18 billion in 2025 (+10.9%) fueled predominantly by price increases rather than volume growth.[F1] Operating income maintained an upward trajectory with a jump from $756 million in 2023 to $770 million in 2024 (+1.8%), before accelerating to nearly $959 million (+24.4%) in 2025.

Most notably, net income skyrocketed from about $119 million in 2023 to approximately $138 million in 2024 (+15.8%), followed by an extraordinary surge to $765 million in 2025 — a staggering +455.9% increase year-over-year reflecting both operational leverage and favorable non-recurring impacts.[F1] This surge underscores Mueller’s robust margin management amid volatile commodity pricing.

Operating cash flow also illustrated solid fundamentals expanding from $673 million in 2023 to nearly $646 million in 2024 before jumping again to $755 million (+17%) in 2025.[F1] Conversely, capital expenditure outlays declined slightly from over $80 million in 2024 to roughly $69 million in the latest year (-14%), underscoring efficient use of capex amid growth.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 765 | 755 | 959 | 69 | +455.9% |

| 2024 | 138 | 646 | 770 | 80 | +15.4% |

| 2023 | 119 | 673 | 756 | 54 | -14.2% |

| 2022 | 139 | 724 | 877 | 38 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 244 | 687 | 23.8 |

| 2024 | 49 | 566 | 5.0 |

| 2023 | 19 | 619 | 5.1 |

| 2022 | 38 | 686 | 7.8 |

Source: SEC companyfacts cache [F1].

Table shows Mueller Industries’ revenue growth accelerating through pricing combined with net income outperforming substantially due to margin expansion and acquisition effects.

Cost Pass-Through Dynamics Amid Raw Material Volatility

Navigating copper, brass, aluminum, zinc prices—and energy inputs—has demanded dexterous cost management from Mueller Industries given years of commodity price volatility.[S1] The company’s dominant position in copper tube manufacturing implicitly ties its input costs closely to Comex copper spot price fluctuations.

Mueller implements dynamic 'price escalation clauses' embedded within customer contracts allowing regular adjustment of selling prices with changes in input costs to preserve spreads.[S1] This strategy effectively transfers most raw material cost increases downstream promptly yet requires close coordination across supply chain partners.

However, factors complicating cost pass-through include tariff impositions affecting import/export flows—such as U.S., Canada, Mexico tariffs imposed or threatened during policy shifts around mid-2020s—and local energy price shocks linked to utilities demand spikes like increased data center capacity expansions.[S1]

To buffer volatility effects, Mueller maintains 'supply chain buffer stock' inventory levels at key facilities that allow short-term smoothing of input dislocations.[S12] Commodity hedging is employed selectively but not as a core risk mitigation tool given the physical nature of metal products production.

Despite these strategies, the company acknowledges that failure to fully recover cost escalations would materially compress margins — underscoring persistent exposure inherent within metals manufacturing economics.[S1]

Segmented Growth Drivers: Piping Systems, Industrial Metals, and Climate Products

In shaping Mueller’s robust topline advance are three distinct reportable segments each addressing specific end markets with complementary product suites.[S4][N1]

Piping Systems maintains leadership through production of copper tubes and fittings used primarily by plumbing wholesalers and HVAC OEMs domestically and internationally.[S4] In FY2025 this segment posted approximately $2.7 billion in external sales reflecting +6% price-related increases despite a volume contraction (~$212 million lower units), highlighting strong unit value per shipment.[S7]

This segment benefits from stable end-market drivers such as new housing starts which remain positive albeit fluctuating seasonally—plumbing applications dominate tube demand here with limited substitution risk relative to industrial metals.[N1] Joint ventures like Jungwoo-Mueller expand regional presence into South Korea while Bahrain operations cover Middle East demand mitigating geographic concentration risk.[S4]

Industrial Metals grew significantly following the mid-2024 acquisition of Nehring Electrical Works which contributed an estimated incremental annual run-rate addition of over $200 million by late-2025.[S4][S20] The portfolio includes brass rods for plumbing components as well as aluminum forgings targeting industrial OEMs across automotive, construction equipment sectors important for diversified demand exposure.

Within this business mix sits specialty copper alloy tubes plus wire & cable solutions serving telecommunications infrastructure—areas benefiting from long-cycle infrastructure spend themes yet exposed more acutely to substitution threats particularly plastics or offshore sourcing competition.[S20]

Climate Segment serves heating, ventilation, air-conditioning (HVAC), refrigeration markets with insulated ducts and refrigeration valves concentrated primarily within U.S. operations producing ~$500 million of revenue annually.[S4][N1] Growth here aligns with broader HVAC system upgrades linked to energy efficiency drives visible within building retrofit markets.

Margin profiles are enhanced modestly by proprietary duct technologies plus manufacturing scale advantages at facilities such as Fulton MS reinforcing domestic competitive positioning.[S20]

Geographic Footprint and Supply Chain Integration as Competitive Advantages

Mueller’s broad geographic scope spans manufacturing hubs across North America (U.S., Canada, Mexico), UK Europe operations,[S4] Asia-Pacific via South Korea joint ventures,[S4] plus Middle East entities providing access into Northern Africa markets — establishing multi-regional coverage enabling tailored service models responding quickly to local customer requirements.[N1][F1]

This footprint supports efficient ‘price freight equalization’ across distribution centers reducing logistics friction despite metal weight sensitivities endemic within copper-based product shipping.[S12] Supply chain integration facilitated by intra-company transfer pricing supports nimble inventory allocation optimizing working capital usage.

Notably, foreign currency exposures linked to British Pound Sterling,-Canadian Dollar,-Mexican Peso,-and South Korean Won are factored carefully given translation risks potentially impacting reported results on consolidation; active currency hedging policies delimit volatility impacts.[S12][S9]

Furthermore,named joint ventures such as Jungwoo-Mueller enhance regional raw material sourcing agility aiding input cost control amidst global supply disruptions experienced since early-2020s geopolitical shifts.[S5]

Capital Allocation Strategy: Share Buybacks, Dividends, and Cash Flow Management

Demonstrating strong free cash flow generation capabilities—the company produced approximately $755 million operating cash flow offsetting capex outlays near $69 million yielding ~686 million USD free cash flow conversion for fiscal year ending December 27, 2025[F1].

Mueller’s Board embraced an assertive capital return posture bolstered by escalating share repurchase programs absorbing roughly $244 million shares retired during the year—a near fivefold increase compared with ~$49 million buybacks executed during prior year[S8].

Dividend policy reflects progressive quarterly increases consistent over recent years moving from $0.15 per share quarterly payments during CY23 stepped up to $0.25 per share during CY25 while the latest declared cash dividend remained at $0.35 per share quarterly payable March 27th 2026[N3][S3]. These payouts mirror confidence underpinned by approximate return on equity nearing an attractive ~23.8% level indicative of productive equity utilization[F1].

Liquidity remains robust evidenced by available revolving credit lines totaling $400 million currently undrawn providing flexible funding optionality should opportunistic acquisitions or market dislocations prompt capital needs [S5][S18].

Risk Factors: Tariff Impacts and Substitution Threats in Core Markets

Key operational risks emerge prominently around tariffs frequently reconfigured amid shifting U.S.-global trade policies introducing unpredictability into raw material import costs especially impacting copper—a major input[S1]. Recent Supreme Court rulings nullifying certain prior tariffs add further regulatory flux compounding planning challenges.Meanwhile retaliatory tariffs imposed by trading partners add layers increasing sourcing complexity.[S1]

Of critical concern is also mounting substitution risk particularly plastics replacing copper piping within plumbing applications—a trend gradually eroding traditional metal volumes requiring vigilant innovation adoption efforts alongside competitive cost discipline[S22]. Aluminum likewise gains traction as alternative refrigerant tubing material imposing incremental pressure on the Climate segment market shares[S22].

Material adverse outcomes could manifest as compressed margins stemming from inability to fully recover increased tariff or raw material costs or losing sales volumes due to switching behaviors toward imported or innovatively engineered substitutes.[S9]

Forward View: Indicators to Watch for Future Growth and Profitability

While explicit management guidance remains limited publicly,[N1][N2] several metrics merit monitoring closely:

- Pricing behavior adaptability tracking spreads between commodity metal prices versus selling price adjustments through ‘price-freight equalization’ mechanisms.

- Volume trends across core segments reflecting end-market health including new housing start rates influencing Piping Systems demand.

- Tariff developments including changes driven through evolving US trade policies or retaliatory actions potentially disrupting global supply chains.

- Acquisition assimilation success post-Nehring adding sustained contributions alongside pipeline visibility for future bolt-on expansions.

- Competitive responses regarding substitution product penetration gauged through shifts toward plastics or aluminum imports applying pressure on legacy copper/brass offerings.

- Capital expenditure plans projecting near-term investments target levels ($80m-$90m planned for FY26) signaling capacity expansion priorities confirming growth intent[S14].

Together these constitute barometers encapsulating Mueller's navigation amid ongoing commodity volatility balanced against strategic diversification cushioned by coordinated global reach.

This analysis synthesizes publicly filed SEC disclosures dated February 25th 2026 ([S1]-[S29]), recent NASDAQ news reports ([N1], [N2], [N3]) alongside company numerical filings via SEC XBRL ([F1]). All financial figures stated are historical performance metrics without predictive commentary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments