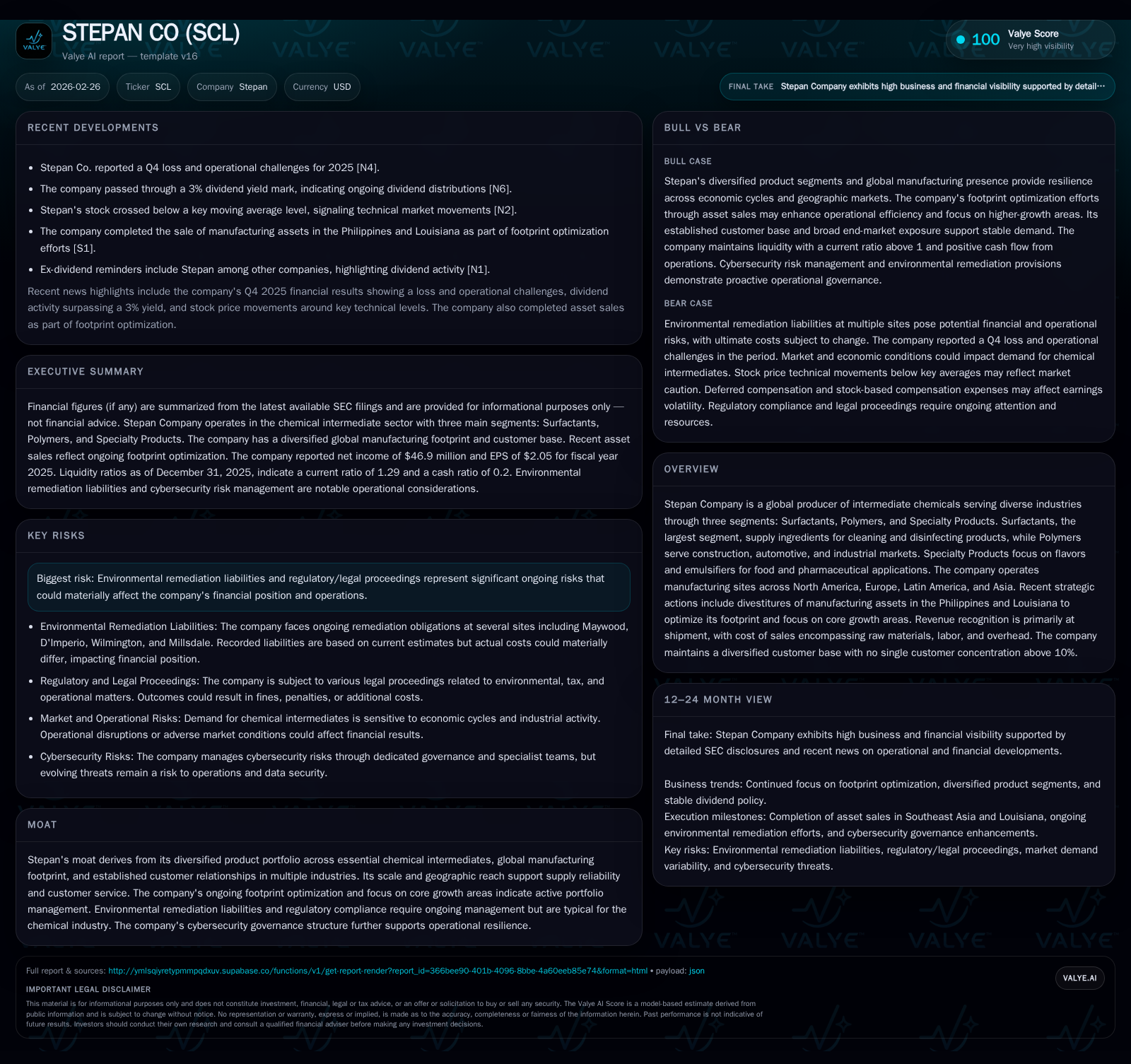

STEPAN CO’s Balancing Act: Growth Constraints and Capital Discipline Shape 2025 Performance

Stepan Company’s diverse chemical intermediates portfolio supports stable revenue, while environmental and operational factors temper earnings growth.

Stepan Company, a global player in chemical intermediates, reported moderate operating income growth but a slight net income decline in 2025, driven by elevated expenses despite steady revenue. The company’s strategic divestitures and footprint optimizations aim to focus on core growth segments—primarily surfactants supported by global manufacturing sites. Environmental remediation costs and regulatory compliance remain persistent risks, while capital allocation emphasizes steady dividends and controlled capex. Liquidity metrics reflect manageable leverage and ample cash flow, with share repurchases paused as the company preserves financial flexibility. Going forward, Stepans’ growth depends on its ability to navigate industry cyclicalities and regulatory pressures without compromising operational resilience.

Company Overview and Historical Performance

Stepan Company specializes in intermediate chemicals spanning three main segments: Surfactants, Polymers, and Specialty Products [S1]. Surfactants constitute the largest segment, supplying critical ingredients for cleaning and disinfecting products globally. Polymers address construction, automotive, and industrial markets, while Specialty Products target flavors and emulsifiers primarily for food and pharmaceuticals. The company operates production facilities across North America (notably Millsdale in Illinois and Winder in Georgia), Europe (France), Latin America (Brazil, Mexico), and Asia (China) [S1].

From a financial standpoint, Stepan has demonstrated stable revenue streams supported by its diversified product portfolio. Although precise revenue figures for the latest fiscal years are not fully disclosed here, operating income provides insight into profitability trends. Operating income increased from approximately $70.5 million in 2024 to $78.5 million in 2025—a healthy 11.4% rise [F1]. This reflects better operational efficiencies amid flat-to-modest revenue growth.

Net income tells a more nuanced story; it declined nearly 7%, from roughly $50.4 million in 2024 to $46.9 million in 2025 [F1]. This decline is attributable primarily to rising administrative costs, which includes increased spending on environmental remediation activities—a known recurring cost given the company’s regulatory context [S14][S15].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 47 | 148 | 79 | 123 | -6.9% |

| 2024 | 50 | 162 | 70 | 123 | +25.3% |

| 2023 | 40 | 175 | 59 | 260 | -72.7% |

| 2022 | 147 | 161 | 207 | 302 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 35 | 25 | |

| 2024 | 34 | 25 | 39 |

| 2023 | 33 | 25 | -85 |

| 2022 | 31 | 25 | -141 |

Source: SEC companyfacts cache [F1].

Note: ROE calculated as net income divided by equity ($1.24B at end-2025).

Operating cash flow has weakened modestly over three years but remains robust at nearly $148 million in 2025 [F1], enabling continued capital expenditures of approximately $122 million focused on modernizing operations.

Industry Positioning and Moat

Stepan’s competitive advantages derive from its broad portfolio of essential chemical intermediates that enjoy end-market demand stability—from household cleaning products to automotive parts manufacturing . The company's expansive manufacturing network underpins reliable supply chains across multiple continents, reinforcing customer loyalty.

Its global footprint has seen recent strategic pruning via divestitures of non-core assets such as plants in the Philippines and Louisiana , aligning operations more tightly with profitable product lines within surfactants and polymers.

Environmental liabilities represent a significant source of risk but also moat barriers against potential new entrants lacking regulatory experience or capacity for ongoing compliance [S14][S15]. The company maintains provisions for cleanup costs estimated between $19 million to $46 million reflecting ongoing remediation activity primarily concentrated at historically contaminated U.S sites including Maywood (NJ), Millsdale (IL) and Fieldsboro (NJ) [S14][S25].

Cybersecurity governance overseen by experienced leadership further enhances operational resilience amid rising industry threats [S1].

Growth Prospects and Limitations

Stepan’s organic growth hinges on sustained demand from its surfactants segment linked closely to consumer hygiene trends post-pandemic as well as targeted industrial polymers applications.

Innovation through R&D investments (~$35 million annually) enables new product formulations catering to evolving market needs such as greener surfactants or bio-based polymers [S16]. However, growth may be constrained by:

- Regulatory pressures increasing environmental compliance costs.

- Cyclical fluctuations in raw material prices impacting margins.

- Geopolitical tensions affecting supply chains or export markets.

- Limited scope for large-scale acquisitions given current strategic focus on footprint optimization .

Increased productivity via operational improvements remains a key leverage point for earnings gains amid modest volume growth.

Outlook & Key Milestones To Watch (Analysis)

While explicit guidance was absent in recently filed documents or earnings releases [N1][S3], investors should monitor:

- Quarterly operating results for margin trajectory—specifically how cost controls offset raw material inflation.

- Progress on environmental remediation projects which can impact expense volatility.

- Capital expenditure adherence within the $100–110 million guidance range for the upcoming fiscal year mentioned by management [S13].

- Potential resumption or expansion of share repurchase programs depending on liquidity trends.

- Regulatory developments domestically (USEPA actions) or internationally that could alter compliance cost structures.

Sector peers' earnings trajectories (e.g., Huntsman, Albemarle) provide comparative context given similar exposure to raw materials cycles and specialty chemical markets [N4][N6].

Capital Allocation & Returns

The company maintains a balanced capital allocation approach emphasizing shareholder returns alongside reinvestment:

- Dividends paid rose modestly from $33.9 million in 2024 to $35 million in 2025 reflecting incremental payout increases consistent with cash flow generation [F1][S8]. The declared quarterly dividend per share was recently affirmed at $0.395 [N3][N11].

- No open market share repurchases occurred during calendar year 2025; however, approximately $125 million remains authorized under an ongoing plan initiated in October 2021 — indicating flexibility for future buybacks when conditions warrant [S8][S13].

- Steady capex investments ($122 million plus projected $100–110 million guidance for next year) focus on modernization rather than aggressive expansion [S13][S16].

- Debt levels were essentially stable at around $627 million year-end with maturities staggered through the next decade; all debt covenants regarding interest coverage (minimum ratio of 3.50x) and leverage (max ratio of ~3.50x) were met comfortably as of December 31, 2025 [S4][S10].

- Cash & equivalents have grown year-over-year from about $99.7 million to roughly $132.7 million with significant balances held outside the U.S., enhancing liquidity management options internationally [F1][S6][S9].

The approximate return on equity was a modest ~3.8% in fiscal year 2025 based on reported net income vs shareholders’ equity levels—indicative of conservative financial stewardship rather than aggressive profit maximization [F1].

Risks & Regulatory Environment

The company faces ongoing environmental exposure inherent to chemical manufacturers, with numerous government proceedings concerning contamination requiring remediation efforts expected to continue over multiple years [S14][S15][S25]. While reserves have been established prudently at the low end of probable ranges ($19m accrued vs up to ~$46m possible) this liability could fluctuate materially depending on government action developments or newly discovered contamination sites.

Legal proceedings related mostly to environmental assessment dominate risk disclosures alongside typical trade, labor, tax issues that occur routinely within industrial companies [S14][S15]. A notable recent regulatory penalty was a $1.1 million USEPA fine related to alleged biocide product violations — partially offset by recovery from third parties during H2’25 [S17].

Brazilian tax disputes concerning PIS/COFINS indirect tax credits remain unsettled but provisioned conservatively per company disclosures due to complex judicial backlog dynamics affecting recognition timing [S17][S18][S25].

Cybersecurity risks are mitigated through structured governance involving senior management oversight supported by certified specialists maintaining threat detection capabilities aligned with industry best practices [S1].

Conclusion

Stepan Company’s performance in FY2025 reflects the tightrope walk many specialty chemical producers face – balancing necessity-driven demand stability with elevated compliance costs and cautious capital deployment amid uncertain macroeconomic factors. Its diversified product portfolio spanning surfactants through specialty emulsifiers supports consistent revenues globally.

Operational improvements lifted operating income appreciably while net profits slipped principally due to intensified administrative costs notably environmental remediation activities mandated by stringent regulations—a theme likely persistent long term.

Capital allocation remains disciplined prioritizing dividends plus measured capex over aggressive share repurchases signaling conservative stewardship designed to preserve balance sheet strength addressing legacy liabilities alongside growth initiatives.

Monitoring progress on remediation projects coupled with evolving regulatory environments will be critical milestones shaping financial outcomes going forward alongside management’s ability to sustain product innovation within core segment focus areas.

This analysis is based solely on publicly available information including SEC filings ([F1]–[S29]) and recent news articles ([N1]–[N12]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments