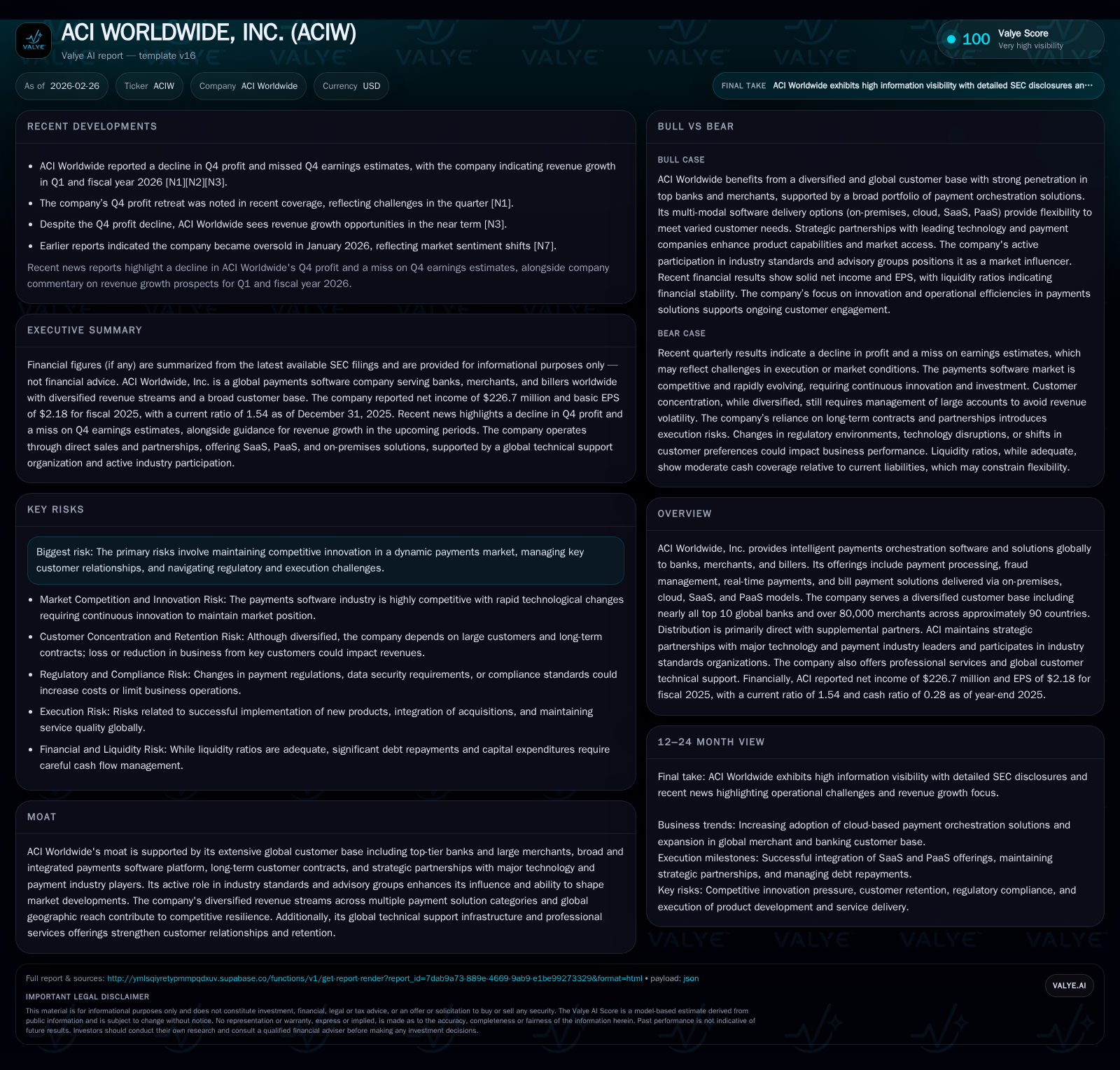

ACI Worldwide’s Growth and Profitability Tested by Competitive Dynamics and Innovation Demands

ACI Worldwide's extensive global footprint and diverse payment solutions underpin solid financials but face pressure from evolving market and regulatory dynamics.

ACI Worldwide, a leading provider of payments orchestration software and services, reported steady revenue growth and improving operating income in fiscal 2025, supported by its diversified client base spanning major global banks and merchants. Its moat is anchored in integrated solutions, strategic partnerships, and recurring revenue streams, though sustaining innovation and managing regulatory complexity remain ongoing challenges. Debt refinancing actions have extended maturities, supporting liquidity, while capital allocation includes significant share repurchases. Monitoring ACI's ability to capitalize on real-time payments expansion and maintain customer loyalty amid intensifying competition will be critical for future growth trajectories.

Company Overview

ACI Worldwide, Inc. delivers comprehensive payment orchestration software globally to banks, merchants, and billers through on-premises, cloud, SaaS, and PaaS deployment models [S1][S16]. The company boasts one of the largest footprints in payments technology servicing nearly all of the top ten global banks by asset size alongside over 80,000 merchants across roughly 90 countries [S4]. Its product suite spans payment processing, fraud management, real-time payments capabilities, bill payment platforms, and professional services including implementation consulting and technical support via its Global HELP24 organization [S16].

Historical Performance and Growth Drivers

ACI’s revenue growth has historically been fueled by expanding digital payments adoption among financial institutions and merchants worldwide alongside innovation in fraud prevention and real-time payments [N2][S21]. The integration of multiple payment solutions into cohesive platforms allows clients to streamline complex transaction flows and manage multi-channel payment infrastructure more efficiently.

Financially, the company delivered operating income of $329.9 million in fiscal year 2025 representing a year-over-year increase of approximately 7.1%, while net income rose 11.6% to $226.7 million [F1]. Operating cash flow stood at $322.8 million but declined about 10% versus prior year; however free cash flow remains robust at around $310 million after accounting for modest capex spending [F1]. This operational efficiency highlights disciplined cost control amid ongoing investment in product development.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 227 | 323 | 330 | 13 | +11.6% |

| 2024 | 203 | 359 | 308 | 15 | +67.2% |

| 2023 | 122 | 169 | 220 | 9 | -14.5% |

| 2022 | 142 | 143 | 204 | 13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 203 | 310 | 14.9 |

| 2024 | 128 | 343 | 14.3 |

| 2023 | 28 | 160 | 9.2 |

| 2022 | 207 | 130 | 11.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures for recent years were not disclosed in the available data.

The notable increase in operating income from FY23 to FY25 stems from broader adoption of subscription-based SaaS/PaaS offerings alongside recurring license and maintenance revenues as well as growing penetration within emerging payment rails like real-time clearing systems [S16][N2]. Meanwhile increasing demand for fraud management solutions supports upselling opportunities.

Business Model and Segment Details

Post a reporting structure change implemented in early FY2025 reflecting shifts in leadership focus [S25], ACI reports two main operating segments:

- Payment Software: Encompasses products serving large/mid-sized banks and merchant clients globally across retail banking digital channels and merchant acquiring verticals. Solutions include issuing/acquiring capabilities along with real-time payments orchestration.

- Biller: Focused on electronic bill presentment & payment solutions targeting utility providers, consumer finance companies diverse sectors including insurance & healthcare [S17][S21].

In the first half of calendar year 2025 reporting periods available: Payment Software revenues showed a steady uplift driven by merchant payments and issuing/acquiring lines while biller segment delivered consistent bill pay revenues supported by embedded AI fraud detection tools [S17][S22].

Capital Structure & Liquidity

ACI demonstrated prudent capital management through an amendment of its Credit Agreement extending senior secured term loan facilities totaling $500 million plus revolving credit capacity up to $600 million maturing February 2029 [S5][S14]. This refinance effort notably redeemed the outstanding $400 million senior notes due August 2026 early in June FY25 [S6][S7]. As of latest reports there was approximately $873 million total debt outstanding dominated by term loans with revolving borrowings elevated during periods [S8][S10][F1].

On liquidity measures at December fiscal year-end:

- Current ratio: ~1.54 reflects adequate coverage of near-term liabilities by current assets [F1]

- Cash & equivalents balance was around $196 million supporting operational flexibility [F1]

Such a balance sheet composition positions ACI to maintain investment-grade posture while preserving capacity for strategic investments or capital returns.

Capital Allocation & Returns

ACI’s cash deployment strategy emphasizes balanced capital return with substantial share repurchases evident with over $200 million executed in FY2025 compared to about $128 million the prior year [F1]. Dividend data was not explicitly disclosed but historically dividends have been modest relative to buybacks.

Return on equity approximates around 15%, indicating effective leverage of shareholders’ equity towards profitability given current net income levels against reported equity base exceeding $1.5 billion as of last filing [F1]. Operating cash flows support consistent funding of R&D investments along with shareholder distributions.

Future Growth Prospects & Challenges

Looking forward several vectors could catalyze growth:

- Expansion in real-time payment schemes worldwide continues providing growth runway as banks rely on ACI’s platform integrations to navigate multiplicity of protocols.

- Increasing concerns around fraud risk underscore demand for enhanced AI-driven fraud detection embedded within core payment processing environments.

- Broader adoption of cloud-native SaaS/PaaS delivery models aligns with client preferences seeking scalability and lower total cost of ownership.

- Ongoing investments in professional services complement product sales generating recurring consulting revenues tied to implementations.

On the flip side notable constraints include:

- Intensifying competition both from established fintech vendors and newer cloud-first entrants requiring relentless innovation pace.

- Regulatory changes affecting cross-border payments necessitate agility in compliance solutions embedding potentially higher costs or delayed deployments.

- Dependence on key banking relationships demands continued excellence in service quality paired with evolving feature enhancements to avoid client attrition risks.

ACI's latest earnings release indicated some profit declines on a quarterly basis although expecting sequential revenue growth into Q1 FY26 hinting at cautious near-term outlook [N1][N2]. Monitoring execution against product roadmap milestones for the remainder of FY26 will be crucial since guidance was broadly framed without specific numeric targets publicly provided.

Competitive Moat Analysis

ACI’s moat stems from its entrenched presence within major banking institutions globally alongside broad merchant networks fostering high switching costs given integrated platform deployments supporting multi-channel payment flows . Strategic alliances with leading technology companies enhance interoperability advantages while participation in industry standard bodies safeguards adaptation to ecosystem evolutions.

Moreover its Global HELP24 technical support infrastructure underpins rapid issue resolution which is vital considering mission-critical nature of payment operations for customers worldwide [S16]. Deep domain expertise embedded within R&D fosters sustained innovation albeit balanced carefully against cost discipline observed recently.

Summary Observations & Watch Points

Finance results reflect stable underlying business momentum fused with steady profitability improvement despite sector headwinds. Robust free cash flow generation enables both reinvestment into next-generation products and meaningful shareholder returns via buybacks. Yet the competitive landscape remains crowded with new entrants vying aggressively especially leveraging cloud-first models.

Key aspects investors should track include:

- Quarterly earnings trends vis-à-vis analyst expectations especially on margins since Q4 results missed estimates initially reported [N1][N5].

- Updates on product adoption curves particularly around real-time payments facilitation capabilities that form a core element of strategic emphasis.

- Progression on expanding professional services sales which act as a differentiation lever enhancing client stickiness beyond pure software licensing.

- Any material changes in leverage or funding costs following debt refinancings which will impact financial flexibility going forward.

- Regulatory developments influencing cross-border settlements where ACI has legacy infrastructure exposure needing modernization.

Overall ACI Worldwide remains well positioned given its scale advantage and diversified solution set but must continuously innovate while managing execution risks intrinsic to highly regulated global payments ecosystem dynamics.

This analysis is based solely on public filings and news reports without any investment recommendation or price forecast. Please consider all risks carefully before making any investment-related decision regarding ACI Worldwide.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments