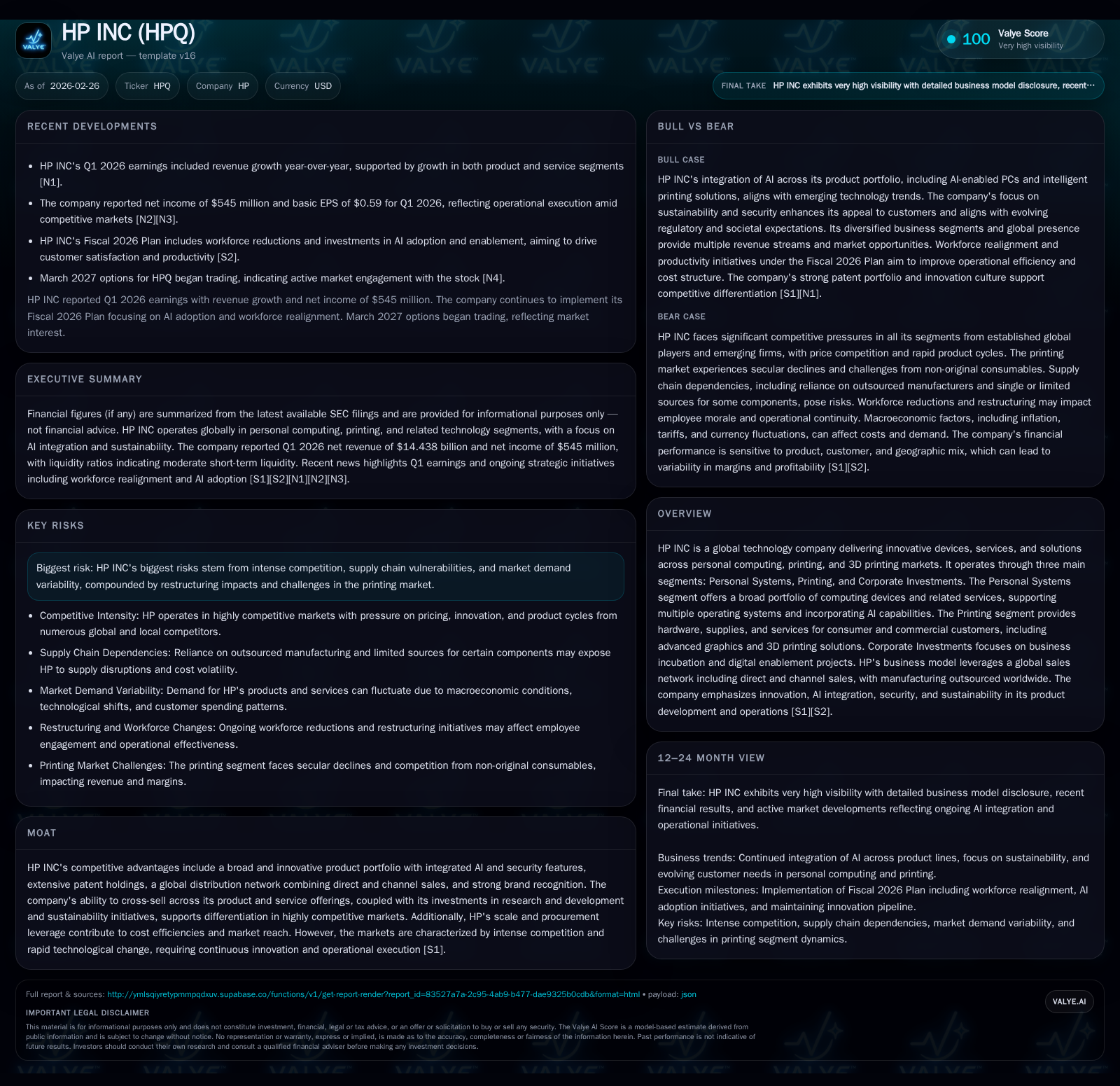

HP Inc's Growth Moderates with Margin Pressure and Strategic AI Investments Weighing on Returns

HP Inc sustains modest revenue growth while grappling with operating income declines amid competitive and structural challenges.

HP Inc reported a 3.2% revenue increase in fiscal 2025, reaching $55.3 billion, driven by innovation and AI integration across personal systems and printing segments. However, operating income declined nearly 17%, pressured by cost inflation and market headwinds, particularly in printing. The company continues focusing on expanding AI-enabled products, subscription services, and sustainability initiatives to drive future growth. Capital returns slowed with buybacks down sharply to $850 million from prior years. While free cash flow remains positive, HP’s equity position is negative, reflecting balance sheet considerations that may impact capital allocation decisions.

Historical Performance

HP Inc has experienced variable financial performance over recent years with top-line resilience but increasing profitability pressures. Fiscal year (FY) 2025 revenue reached $55.3 billion, up 3.2% from FY2024's $53.6 billion yet below FY2022’s peak of $62.9 billion [F1]. This moderate growth reflects HP's capacity to sustain demand across its broad portfolio despite market headwinds.

Operating income for FY2025 declined sharply by nearly 17% year-over-year to about $3.17 billion from $3.82 billion the year prior [F1]. This erosion signals margin pressure stemming from elevated costs—particularly memory and storage components—and intense price competition in both personal systems and printing markets [S1][S24]. Net income similarly fell by almost 9% to approximately $2.53 billion [F1], tracing impacts of higher operating expenses alongside strategic investment spending.

Cash flow generation remained solid though slightly down; operating cash flow stood at around $3.7 billion compared with nearly $3.75 billion previously [F1]. After capital expenditures aligned with ongoing supply chain investments and product development, free cash flow was positive at an estimated $948 million [F1]. However, shareholder equity was negative at minus $346 million for the latest reported fiscal year end [F1], highlighting liabilities or accumulated deficit issues requiring management attention.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 55.3 | 2.5 | 3.7 | 3.2 | +3.2% | -8.9% |

| 2024 | 53.6 | 2.8 | 3.7 | 3.8 | -0.3% | -15.0% |

| 2023 | 53.7 | 3.3 | 3.6 | 3.5 | -14.6% | +4.2% |

| 2022 | 62.9 | 3.1 | 4.5 | 4.6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | ROE% |

|---|---|---|

| 2025 | 0.8 | -730.9 |

| 2024 | 2.1 | -209.8 |

| 2023 | 0.1 | -305.2 |

| 2022 | 4.3 | -103.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY is sequential fiscal year change; negative values noted where applicable.

Business Overview and Competitive Positioning

HP Inc operates principally through three segments: Personal Systems (PS), Printing, and Corporate Investments focused on emerging technologies and digital enablement [S1][S4]. The company caters to broad customer bases covering consumers, small-to-medium businesses (SMBs), large enterprises, public sector clients, and industrial customers globally across more than 170 countries.

The Personal Systems segment offers a wide range of notebooks, desktops, workstations—including AI-enabled models for local processing acceleration—and hybrid systems supporting Microsoft Windows and Chrome OS platforms [S19]. This segment includes distinct business units for commercial (enterprise/public sector/SMBs) and consumer users, featuring HP’s Dragonfly, Pro, Elite lines on commercial side; Omni consumer PCs; Omen gaming devices; Spectre, Envy family among others [S11][S17].

Printing addresses hardware sales along with consumables like ink cartridges historically central to profitability but now transitioning amid industry-wide declines due to digitization trends and hybrid work habits reducing print volumes [S1][S24]. The portfolio now integrates big tank printers offering refillable ink solutions with higher margins upfront but lower lifetime device profitability compared to cartridge models [S1]. The printing business also targets growth in managed print services (subscription-based), graphics printing, packaging converters, industrial and commercial digital personalization including additive manufacturing or 3D printing capabilities promoted through collaborative ecosystems [S11][S17].

Corporate Investments develop incubated projects supporting HP’s broader evolution toward hybrid consumption models enhanced by AI integration and sustainability-focused offerings [S1][S19].

Competitive advantages include HP’s extensive intellectual property portfolio exceeding 16,000 patents that safeguard innovations in AI-powered devices and print security features [S4]. The global sales network spans direct sales combined with vast channel partnerships—retailers predominantly serving consumers/SMBs while resellers focus on mid-market/public/large enterprises—facilitating broad market coverage tailored geographically [S4][S6][S14]. HP leverages scale efficiencies in procurement plus differentiated product design emphasizing security layers including containment/isolation tech assisted by AI deep learning malware detection integrated into hardware/software stacks across PCs and printers [S19].

Nonetheless, aggressive price competition persists against major multinational rivals such as Lenovo, Dell, Canon (for printing), Apple (consumer hardware premium tier), as well as regional OEMs pushing generic products at lower cost points impacting margins [S24][S15]. Supply chain complexities exacerbate cost challenges given component shortages especially memory/storage areas alongside inflationary wage/material cost trends within outsourced manufacturing partners located globally [S14][S21].

Future Growth Prospects

HP continues investing heavily in research & development targeting key growth vectors: embedding AI capabilities broadly within PC architectures for speed/security enhancements; cultivating subscription/managed services within printing offsetting declines in consumables; expanding graphics/industrial printing segments leveraging digital personalization advances; enhancing sustainability credentials via recyclable materials/designs; and embracing new business models aligned with evolving workplace/hybrid work dynamics [S1][S4][S19].

The newly launched AI PC lineup powered by Intel/AMD processors featuring integrated AI acceleration alongside NVIDIA GPUs aims to deliver significant performance differentiation for workloads such as local inference tasks not reliant solely on cloud infrastructure—a potential future-proofing element given privacy/security trends [S19]. Similarly, advanced printer features applying intelligent software are improving user experiences while optimally managing operating expenses for SMBs and office clients.

Subscription-based approaches including device-as-a-service bundles that combine hardware with software support constitute an area of strategic emphasis though transition risks persist including potential upfront revenue deferral impacting near-term financials as customers shift from transactional purchase models toward recurring fee structures [S12][S22]. HP seeks to capture cross-selling synergies across its ecosystem especially integrating endpoint security solutions throughout devices/systems enhancing value propositions vis-à-vis competitors.

Nonetheless growth could be capped by continued secular headwinds in legacy print supply consumption exacerbated by macroeconomic uncertainties affecting corporate IT spend patterns or further component cost escalations forcing pricier configurations beyond some buyers’ budgets [S1][S22]. Geopolitical trade disruptions or regulatory changes related to AI governance frameworks might also introduce compliance complexities thereby increasing operational costs or delaying product launches.

Forecasts & Expectations

While explicit forward guidance was reaffirmed following recent Q1 earnings announcements that beat expectations on revenues but showed mixed profit trends [N1][N2], management flagged cautious outlook statements relating to competitive intensity especially in printing supplies segments amid digitization-related demand shifts [N12]. Monitoring will focus on HP’s ability to grow its subscription/recurring revenue streams successfully plus expansion in emerging enterprise markets which typically exhibit higher margins but slower volume ramp-ups.

Further earnings calls scheduled will provide insight into execution against the FY26 restructuring plan aimed at optimizing cost structures without sacrificing innovation pipeline vitality—whether these initiatives achieve targeted margin expansions remains critical for restoring durable profitability growth trajectories given recent operating income softness [N5][N6][N7].

Returns & Capital Allocation

HP generated roughly $3.7 billion in operating cash flow during FY25 while free cash flow approximated just under $1 billion after investing for capital expenditures supporting technology/material sourcing improvements [F1]. This indicates continued solid internal funding capacity despite headwinds.

Capital return activity moderated noticeably with share repurchases totaling only about $850 million versus $2.1 billion the previous fiscal year—a reduction likely reflecting management caution amid profitability pressures and balance sheet constraints marked by the first recorded negative equity since separation from Hewlett Packard Enterprise several years ago [F1][S8] . Dividends remain a key component of the total shareholder return strategy but data limitations preclude detailed yield analysis here.

Return on equity is a negative metric currently given shareholder deficit positioning (approximate ROE is -730%) signaling financial leverage or accumulated losses may weigh on investor perception; this also underscores potential challenges in deploying incremental capital for aggressive buybacks or other growth initiatives without first stabilizing balance sheet fundamentals more effectively [F1].

Industry Context Analysis

The broader PC and printing industries continue grappling with rapid technological shifts including AI-driven workload demands reshaping device architectures alongside ongoing commoditization pressure especially in mature markets fighting saturation effects compounded by pandemic-induced buying pattern normalization post-2020 peak spikes.

Printing consumables face long-term secular decline driven by digitization adoption accelerated by hybrid working models reducing home/office paper usage just as supply chain disruptions inflate costs of ink/cartridge manufacturing components globally ensuring persistent margin contraction risks despite countermeasures such as shifting customers toward subscription-based replenishment models or bigger ink tank printers which shift profit profiles rather than fully recapturing historic revenue pools.

Competition intensifies as better-capitalized rivals harness proprietary cloud ecosystems restricting access or embedding vertically integrated security stacks limiting third-party participation—a serious strategic consideration given HP’s heavy reliance on broad OEM partnerships plus channel distribution networks needing constant modernization amidst evolving customer buying preferences towards online omnichannel purchasing environments.

Conclusion

In sum, HP Inc navigates a nuanced inflection point balancing modest revenue growth stimulated by transformational efforts around AI integration and service evolution against constraining cost escalations amplified by fierce competition primarily impacting operating income margins across both personal systems and printing units.

The company's focus on innovation areas such as AI PCs/workstations coupled with push into subscription services demonstrate forward-looking pathway logic but require continuous execution rigour amid external risks like component price inflation plus evolving regulatory landscapes challenging global supply chains.

Capital discipline appears increasingly prudent given negative equity dynamics although sustained free cash flow generation provides flexibility if underlying operating margin improvements materialize from restructuring efforts planned through FY26.

Investors should observe upcoming quarterly updates closely monitoring mix shifts—especially recurring revenue take rates—and cost control effectiveness alongside additional clarity regarding balance sheet remediation strategies potentially influencing future capital return policies.

This analysis offers a comprehensive overview grounded strictly in disclosed financial data and firm-specific disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments