Block, Inc. Accelerates Cost Efficiency and Ecosystem Integration Amid Strategic Retrenchment

Block’s 2025 performance reflects steady revenue growth tempered by workforce reduction and ongoing regulatory and capital challenges.

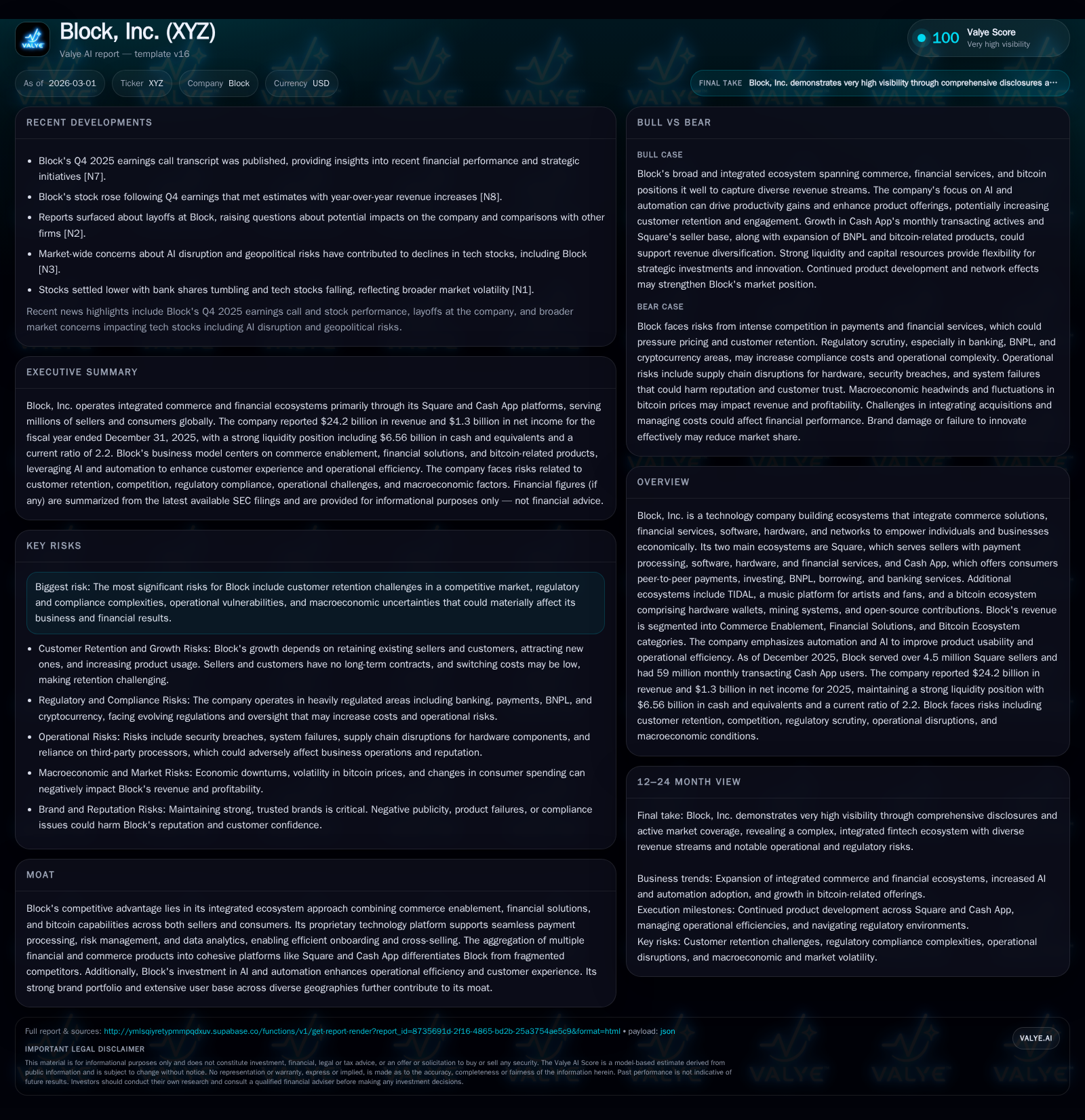

Block, Inc. reported a modest 0.3% increase in revenue to $24.2 billion for fiscal 2025, driven by growth in its Cash App and Square ecosystems. Operating income nearly doubled year-over-year to $1.7 billion, reflecting improved operational efficiency despite net income declining due to one-time tax benefits in 2024 not recurring. The company announced a significant workforce reduction of over 40% to better align structure with strategic priorities and plans continued AI-driven efficiency gains. Capital allocation included $2.3 billion in share repurchases and $2.2 billion in senior notes issuances, while liquidity remains robust at $9.2 billion. Regulatory compliance, competition, and macroeconomic conditions remain material risk factors.

Historical Financial Performance

Block, Inc.'s top-line revenue growth has been steady but moderating over recent years. Fiscal year (FY) revenues reached approximately $24.19 billion in 2025, showing only a marginal increase of about 0.3% compared to FY2024's $24.12 billion [F1]. This follows a historical trend of strong increases earlier in the period, including a notable step-up from $17.53 billion in FY2022.

The company's operating income rebounded meaningfully after prior losses recorded in FY2022 and FY2023, rising to approximately $1.71 billion for FY2025—a near doubling from FY2024 levels of about $892 million [F1]. The correction from prior negative operating income reflected enhanced cost controls and margin improvements across Block's ecosystems.

Net income showed high volatility influenced by significant tax items; FY2025 net income was approximately $1.31 billion but declined by nearly 55% against FY2024’s reported $2.90 billion, which included large one-time deferred tax asset recognitions [F1][S1]. This divergence underscores the impact of non-recurring accounting effects masking underlying core profitability changes.

Cash flow from operations climbed robustly by over 50%, reaching about $2.58 billion in FY2025 versus roughly $1.71 billion the prior year [F1], supporting continued investments despite stable capital expenditures near ~$155 million annually [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 24.2 | 1.3 | 2.6 | 1708 | +0.3% | -54.9% |

| 2024 | 24.1 | 2.9 | 1.7 | 892 | +10.1% | +29546.4% |

| 2023 | 21.9 | 0.0 | 0.1 | -279 | +25.0% | +101.8% |

| 2022 | 17.5 | -0.5 | 0.2 | -625 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 2.3 | 2.4 | 5.9 |

| 2024 | 1.2 | 1.6 | 13.6 |

| 2023 | 0.2 | -0.1 | 0.1 |

| 2022 | 0.0 | -3.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue shown in billions; other figures are millions or billions as noted.

Business Model and Ecosystem Strategy

Block operates multiple interconnected ecosystems anchored principally around its Square and Cash App platforms [S1]. Square targets sellers with integrated payment processing hardware/software combined with lending (notably Square Loans) and other business tools—an evolution from its original role enabling card acceptance for small businesses since its founding in early-2009.

Cash App offers financial services direct to consumers including peer-to-peer payments, debit cards linked to stored funds (Cash App Card), investing options, BNPL products, borrowing through Cash App Borrow, and bitcoin trading capabilities [S1]. These dual ecosystems are designed with shared infrastructure emphasizing payments processing, risk management, data analytics, and AI-powered automation.

Nascent ventures include TIDAL for music streaming and various bitcoin-oriented assets like hardware wallets and mining platforms that bolster Block's positioning at the intersection of fintech innovation [S1].

Drivers of Past Growth

Revenue growth was propelled chiefly by expanding services within both Cash App Borrow and Square Loans products, alongside broader adoption of payment technology by sellers under Square’s umbrella [S1]. Gross profit for cash app grew ~21% year-over-year driven prominently by borrowings while square ecosystem gross profit rose about ~9%, powered mostly by financial solutions expansion [S1].

Cross-selling within the integrated ecosystems enhanced unit economics allowing Block to deepen engagement across its customer base exceeding millions of sellers (over 4.5 million as of late-2025) and tens of millions of end-users on consumer side (59 million customers for Cash App) [S1].

Operational improvements were aided by stepped-up focus on cost efficiencies beginning circa FY2023 — efforts that expanded through FY2025 including severance spend rising from roughly $27 million to nearly $79 million as part of streamlining initiatives [S1].

Challenges Impacting Results

Despite operational progress, Block faces heightened challenges including intense competition among fintech providers offering fragmented payment or lending services that Block uniquely addresses via ecosystem integration but must defend vigorously [S8][S22]. Furthermore, regulatory scrutiny has intensified notably: multistate Attorneys General investigations related specifically to Cash App customer service practices led to ongoing settlement discussions that may yet impose penalties or operational constraints [S22][S24].

Additionally, prior-year one-off tax valuation releases created earnings comparability issues contributing significantly to depressed net income YoY despite improving operating fundamentals [F1][S1]. Exposure to bitcoin market volatility poses continued risk given Block's crypto asset holdings (~8,883 bitcoins valued at approximately $777 million end-2025 on balance sheet) [S13].

Future Growth Prospects

Growth opportunities lie primarily in further penetration of existing ecosystems plus leveraging AI automation for scaling efficiency gains per management commentary [S1]. Continued development of embedded financial services within both seller- and consumer-facing apps aims at increasing wallet share via lending expansion (BNPL/Cash App Borrow), investment product enhancements, bank partnerships through Square Financial Services bank charter leverage, and accelerating bitcoin-related services adoption with open protocol strategies.

Additional avenues include monetization potential within TIDAL streaming platforms aligned with crypto integration initiatives albeit currently categorized as nascent businesses requiring capital deployment before material contribution [N1][S26]. However, successfully executing on these fronts requires navigating complex regulatory environments spanning multiple jurisdictions coupled with maintaining user trust amid data privacy/security concerns under evolving laws such as GDPR/CCPA frameworks [S8][S12].

Capital Structure & Liquidity Position

Block maintains a robust liquidity position with total available funds around $9.2 billion at end-December-2025 consisting predominantly of cash equivalents ($6.56 billion), restricted cash ($1.07 billion short-term plus ~$74 million long-term), investments in marketable debt securities ($706 million combined), plus an undrawn revolving credit facility now increased to $900 million from prior commitments of $775 million following amendments signed January-14-2026 [S13][S14][S15][S25].

Debt issuance included new senior unsecured notes totaling approximately $2.2 billion split between maturities due in 2030 ($1.2B) and 2033 ($1B), facilitating refinancing activities and optimizing maturity profile [S10][S15]. The facility covenants remain manageable with no breaches reported.

Warehouse financing facilities totaling an aggregate capacity of ~$1.7 billion support BNPL funding needs; drawn amounts stood at ~$1.4 billion secured against consumer receivables held within off-balance sheet special purpose entities structured specifically for receivables financing purposes [S7][S15].

Capital Allocation & Returns

A prioritized capital return strategy is evident with share repurchases expanding markedly—to approximately $2.33 billion executed during fiscal year FY2025 up from roughly half that amount the previous year—under an authorized repurchase program raised recently to a total capacity of up to $9 billion shares outstanding [S17][F1]. No dividends have been declared historically.

Return on equity is moderate; estimated ROE as net income divided by equity stands near ~5.9% for FY2025 reflecting subdued profitability relative to shareholders' equity base exceeding $22 billion [F1]. Ongoing restructuring aims may enhance this going forward although elevated regulatory/legal risk premiums could weigh on effective returns.

Operational Changes & Workforce Reduction Efforts

In February-2026 Block announced a substantial workforce reduction initiative aimed at cutting headcount by more than forty percent ahead of mid-2026 closing milestone dates [N6][S10]. These measures align with an overarching drive towards streamlined organizational structures leveraging artificial intelligence-driven automation tools intended both as productivity enhancers and duplication minimizers across corporate functions.

Severance charges reflect accelerating costs related to this downsizing (from ~$27 million in FY24 to nearly ~$79 million recorded officially for FY25), indicating upfront investment pain offsetting longer-term operating leverage prospects [S10]. Management anticipates operational efficiencies derived here will compound benefits over subsequent periods although near-term expense profile will remain elevated.

Industry Context & Competitive Positioning (Analysis)

The payment processing industry continues evolving rapidly toward integrated fintech platforms combining payments acceptance technology with embedded banking/lending plus broad consumer finance functionality including crypto participation—a sector where incumbents face competition not only from traditional banks but also nimble digital entrants targeting distinct verticals or demographics.

Block’s competitive moat stems largely from its ability to provide cohesive cross-platform experiences integrating commerce enablement through Square’s hardware-software stack alongside pervasive consumer financial services delivered via Cash App combined with deep bitcoin ecosystem investments creating differentiated credibility among digital-first users seeking seamless money management tools across use cases—often described as 'super app' characteristics uncommon outside select emerging markets.

However regulatory risks tied particularly to money transmission licenses across states/countries plus potential fallout from legal actions heighten operational uncertainties relative to less regulated rivals or niche fintech apps focused narrowly on payments or lending without banking supervision burdens.

Risks Summary

Key risks involve:

- Customer retention vulnerabilities heightened by intense competition particularly where single-feature fintechs can undercut pricing or promote niche innovations faster than incumbents).

- Complex multi-jurisdictional regulatory environments raising compliance costs inclusive of privacy/data security regimes,

- Macro-economic factors influencing credit quality especially within loan portfolios backing BNPL and Square Loans,

- Legal exposures arising from ongoing class action suits plus state/federal investigations into Cash App customer dispute handling,

- Operational risks including systems outages or security breaches impacting trust critical for payment incumbents,

- Cryptocurrency market volatility impacting balance sheet fair value fluctuations given sizeable bitcoin holdings,

- Execution challenges around timely realization of anticipated cost savings through workforce cuts plus technological integration.[S8][S22][N6]

What To Watch Going Forward (Analysis)

Absent explicit long-term guidance disclosures beyond announced restructuring milestones [N1], investor attention should focus on several key metrics:

- Revenue trends particularly organic growth rates within core Cash App borrowings + financial services,

- Operating margin trajectory post-restructuring including impact of AI automation adoption,

- Regulatory/legal developments notably any outcomes relating disclosures involving the CFPB consent orders or multi-state attorney general negotiations,

- Balance sheet health tracking liquidity usage versus debt maturities,

- Share repurchase program execution pace providing insight into capital return priorities versus potential acquisition capacity,

- Progress updates on TIDAL scaling efforts or new ecosystem expansions which could represent optionality balanced against near-term cost pressures.

Continuous monitoring will be critical given evolving fintech competitive dynamics shaped both by technological innovation cycles such as generative AI penetration into financial workflows plus shifting regulatory landscapes globally.

This analysis aims solely to provide an informed perspective based on recent public disclosures without offering investment advice or recommendations regarding Block, Inc.’s securities or strategy.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments