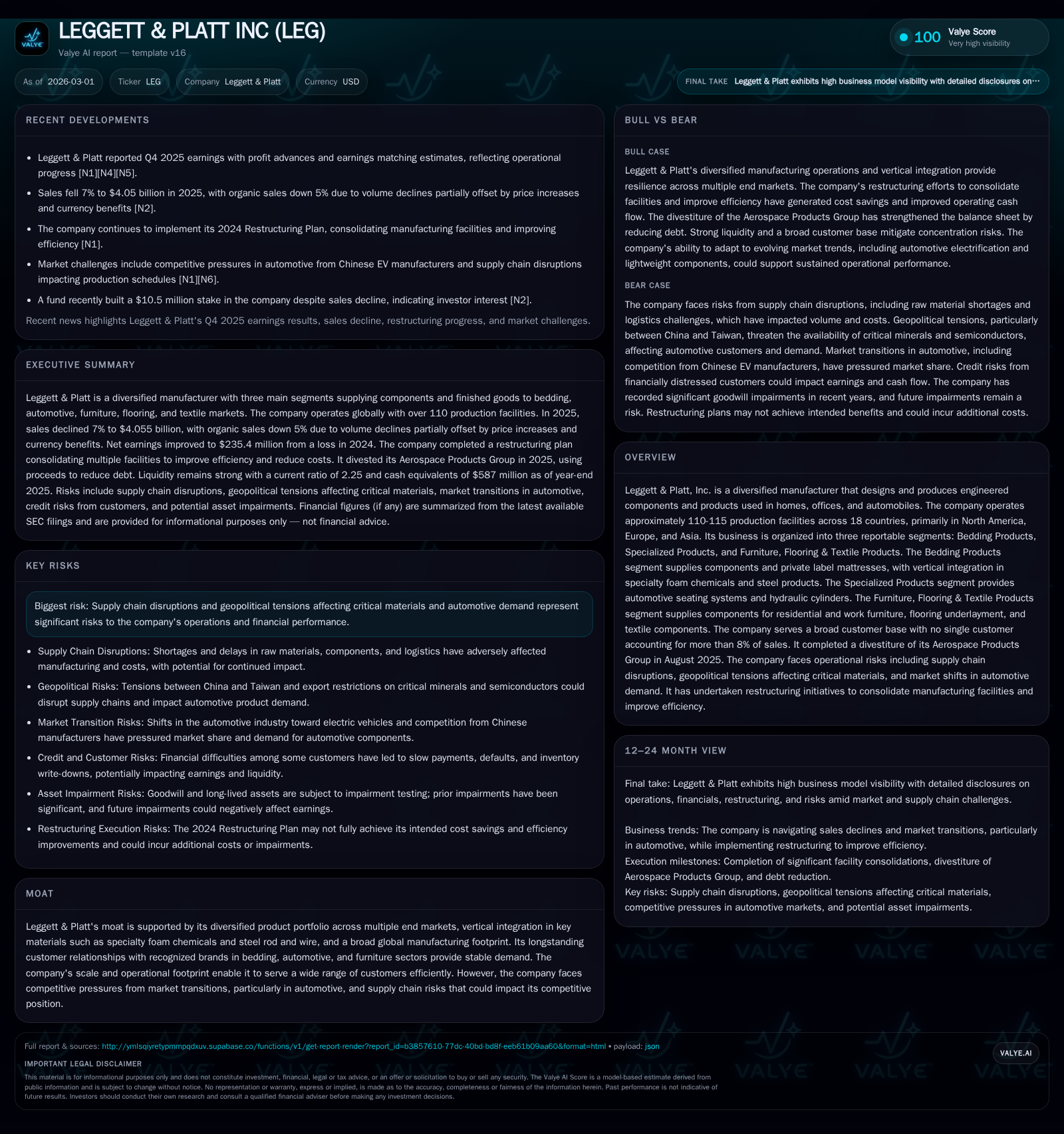

Leggett & Platt’s Revenue Resilience and Margin Recovery Fuel 2025 Turnaround

After years of losses, Leggett & Platt sharply rebounded in 2025 driven by operational improvements, strategic divestitures, and supply chain management.

Leggett & Platt reversed its multi-year net income losses with a $235 million profit in fiscal 2025 supported by improved operating margins and operating cash flow growth. The bedding segment’s vertical integration into steel rod and specialty foam chemicals insulated input costs amid tariff-driven supply disruptions. Key restructuring initiatives including the aerospace group divestiture bolstered margin recovery and debt reduction. However, ongoing challenges remain with anti-dumping litigation and global supply chain volatility. Capital allocation favored deleveraging and dividend conservatism despite improving free cash flow.

Financial Performance Evolution: From Losses to Profit

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 235 | 338 | 57 | +146.0% |

| 2024 | -511 | 306 | 82 | -273.9% |

| 2023 | -137 | 497 | 114 | -144.2% |

| 2022 | 310 | 441 | 100 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 27 | 2 | 281 |

| 2024 | 136 | 5 | 224 |

| 2023 | 239 | 6 | 383 |

| 2022 | 229 | 60 | 341 |

Source: SEC companyfacts cache [F1].

Leggett & Platt’s financial trajectory from FY2023 through FY2025 exhibits a marked turnaround. After registering net losses of approximately $137 million in FY2023 and a much steeper loss of $511 million in FY2024, the company swung to a solid net income of $235 million in FY2025 [F1]. This jump represents a dramatic recovery both operationally and financially. Revenue remained relatively stable at around $5.2 billion during this period, with FY2025 showing a slight 1.4% increase over FY2024 [F1]. Operating cash flow improved by roughly 10.6% year-over-year, reaching $338 million in FY2025 despite a strategic cutback on capital expenditures by nearly 30% to about $57 million [F1].

A significant portion of the elevated profitability was backed by non-recurring gains, chiefly an $87 million gain on the sale of the Aerospace Products Group completed mid-2025 [N1][S2]. Supplementary positive impacts included insurance proceeds related to a fire incident within the Bedding Products segment and real estate sales totaling approximately $39 million combined during H2 of 2025 [N1][S2]. Such one-offs contributed materially to Q3/Q4 earnings boosts, elevating EBIT markedly versus the prior year periods.

Notwithstanding these lifts from divestitures and incidental gains, underlying core operations showed improvements highlighted by incremental volume stability and margin recoveries across key segments. Operating cash flow ascension alongside lowered capex underlined better working capital management amid restructuring initiatives.

Segment Insights: Bedding Products’ Role and Vertical Integration

The Bedding Products segment remains pivotal for Leggett & Platt, contributing about 38% of trade sales through the first nine months of 2025 [S2]. This segment benefits from substantial vertical integration that strengthens cost control over critical inputs amid volatile global supply conditions. Notably, Leggett & Platt owns a major steel rod mill located in Sterling, Illinois, with an annual capacity around half a million tons [S1]. Approximately half of this output feeds internally into wire drawing mills (in Missouri and Indiana), which process rod into drawn wire essential for mattress innersprings and other components.

This internal production capability mitigates reliance on external suppliers susceptible to market disruptions or tariff-related cost escalations. Steel materials have been subject to several U.S. antidumping and countervailing duties targeting countries such as China, Indonesia, and others — affecting import availability and pricing dynamics [S1][S24]. Furthermore, the company vertically integrates specialty foam chemical production used domestically within Bedding Products. This integrated supply chain offers resilience against foam chemical shortages that have plagued the broader industry recently due to raw material constraints.

The combined impact of these factors creates a competitive moat by insulating product cost inputs from broader market swings. The ability to supply own steel products externally also diversifies revenue channels beyond mattress manufacturing customers.

Strategic Actions Impacting Operations in 2024-2025

During this period, Leggett & Platt undertook decisive restructuring moves focused mainly on capacity rationalization within its Bedding Products and Furniture, Flooring & Textile Products segments [S2]. Specifically, it consolidated approximately 17 manufacturing or distribution facilities within bedding operations plus an additional four facilities servicing furniture-related lines primarily across U.S.-based sites [S1][S2]. These actions responded to historically reported suboptimal capacity utilization rates across many plants.

The sale of Aerospace Products Group in July 2025 not only generated significant proceeds ($276 million) but also infused EBIT with an immediate one-time gain of $87 million contributing notably to quarterly earnings improvements [N1][S2]. The divestiture allowed reallocation of resources towards core businesses while advancing debt reduction objectives.

Restructuring-related charges totaled about $15 million for the first nine months of 2025 but were offset more than threefold by associated operational margin improvements stemming from leaner footprint and overhead rationalizations [N1][S2]. These measures created scalability benefits that should underpin future margin stability even if demand growth remains subdued.

Trade Policies and Supply Chain Challenges Influencing Cost Structure

Trade-related regulatory actions profoundly shape Leggett & Platt’s cost structure especially concerning mattresses — a category heavily scrutinized under U.S. trade enforcement policies [S1][S24]. Antidumping duties implemented since early 2020 cover imports from China (with duties extended through May 2030), along with several Southeast Asian countries where impositions range broadly up to hundreds percent margins.

In addition to tariffs enacted on finished mattress imports from countries such as Bosnia-Herzegovina, Bulgaria, India, Italy, Mexico, Poland, Taiwan among others with final injury determinations reached throughout mid-2024, ongoing legal proceedings persist including appeals filed against DOC rulings and an ITC importer appeal regarding retroactive duties assessments [S1].

More recently (November 18, 2025), petitioners including Leggett & Platt have requested DOC initiate ‘anti-circumvention’ inquiries targeting mattress component imports purportedly being assembled into mattresses domestically but circumventing dumping orders—focused on Poland, Mexico, Malaysia shipments [S1]. Such actions aim at sustaining trade protections but pose uncertainty regarding future competitive dynamics.

Suppliers also face broader supply chain risks encompassing foam chemical shortages linked to raw material delays or geopolitical tensions especially impacting Asian manufacturing hubs relevant for furniture components as well as automotive seating systems supplied via Specialized Products segment [N1][S24]. Disruptions affecting aluminum component supplies for automotive OEMs further complicate demand fulfillment reliability.

Capital Allocation: Debt Reduction, Shareholder Returns, and Cash Flow Trends

Capital allocation choices reflect Leggett & Platt’s financial stabilization priorities following years of distress. The company delivered an approximate ROE near 23% for FY2025 based on net income relative to equity levels reported at year-end [$235 million / ~$1.02 billion] [F1]. It generated free cash flow (operating cash flow minus capex) around $281 million highlighting solid cash conversion alongside conservative investment spending reductions relative to prior years [F1].

The amended credit facility completed July 2025 extended maturity out to July 2030 while reducing aggregate lending commitments from $1.2 billion down to $1 billion providing ongoing liquidity backup for commercial paper issuance though no outstanding borrowings were recorded under the revolver at December ’25 close—borrowing capacity was estimated near $709 million after factoring covenant limits [S6][S8][S11]. This amendment signals proactive debt management amidst improving operating results.

Shareholder returns became more restrained post-loss years. Dividends dropped significantly from roughly $136 million paid in FY24 down to just $27 million paid during FY25 reflecting deliberate payout moderation consistent with accelerating deleveraging goals [F1][S14]. Meanwhile share repurchases slowed considerably to only about $2.4 million from higher preceding buybacks evidencing cautious capital deployment amid volatile market conditions.

Overall capital strategy reflects priority given to balance sheet repair while preserving optionality for selective acquisitions or organic growth investments if opportunity sets emerge.

Forward-Looking Considerations: Growth Prospects and Pending Risks

Management commentary from recent earnings transcripts shows guarded optimism around stabilizing customer demand post-pandemic disruptions especially within bedding and furniture end markets but refrains from explicit revenue guidance due primarily to unresolved external uncertainties including trade litigation outcomes affecting import pricing structures [N1][N3][S24].

Pending appeals related to anti-dumping duty revocations particularly involving Indonesia maintain downside risk given possibility of lower protectionist tariffs potentially eroding domestic pricing power [S1]. Meanwhile anti-circumvention investigations raise questions about enforcement strength impacting component sourcing.

Geopolitical risks extending supply chain volatility—especially in Asia—pose operational headwinds including freight bottlenecks or supplier insolvencies which could constrain volume growth or hamper cost containment efforts prompting margin pressure despite internal efficiency initiatives [S24][N1].

Organic growth drivers rely heavily on bedding innovations leveraging proprietary specialty foam chemical capabilities plus potential market share gains via expanded private label mattress offerings complemented by select product line optimizations across furniture components addressing evolving workplace trends [N1][S2]. Strategic acquisitions remain contemplated but currently quiet given deleveraging emphasis.

Operational Capacity and Manufacturing Footprint Dynamics

Leggett & Platt operates roughly between 110-115 production facilities spanning approximately 18 countries worldwide emphasizing North America, Europe, and Asia predominantly servicing their respective regional markets [S1]. Total owned plants account for about half that count (53 owned vs ~51 leased globally) indicating flexibility embedded through lease arrangements particularly meaningful for furniture/flooring units where footprint consolidation has been active recently [S1].

Critical production assets include the extensive steel rod mill (~1 million square feet) at Sterling IL supporting critical vertical integration within Bedding Products—a linchpin asset whose disruption could impose significant sourcing shocks requiring expensive spot market purchases adversely impacting margins [S1].

Most facilities reportedly operated below full capacity utilization rates entering FY25 enabling consolidation plans without near-term drastic capital expenditure requirements while improving operational scalability as excess footprints are trimmed through restructuring schemes implemented since early 2024 targeting improved productivity metrics across segments [S1][S2]. Geographic diversity helps mitigate supply interruptions localized either politically or logistically enabling customer service continuity even when specific facility challenges arise.

Leggett & Platt’s financial recovery embodies a complex interplay between strategic restructuring; savvy supply chain risk management anchored by vertical integration; tactical portfolio adjustments; disciplined capital allocation offsetting returns; all underpinned by ongoing trade policy dynamics creating both protective moats yet intrinsic uncertainty. While the resurgence evident in FY25 signals robust operational momentum restoration relative to recent losses, vigilance remains critical given macroeconomic headwinds nonetheless poised against evolving consumer demand patterns across diversified end markets.

This report is based solely on publicly available information provided by Leggett & Platt Inc. filings, transcripts, news sources cited herein, and companyfacts numeric data as referenced without extrapolation or forward-looking predictions beyond stated evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments