How Park Ha's Franchise Model and Peptide Tech Shape its Outpaced Financial Performance

Park Ha Biological Technology leverages proprietary peptide skincare innovations and an expanding franchise network, yet faces mounting financial losses amidst strategic restructuring.

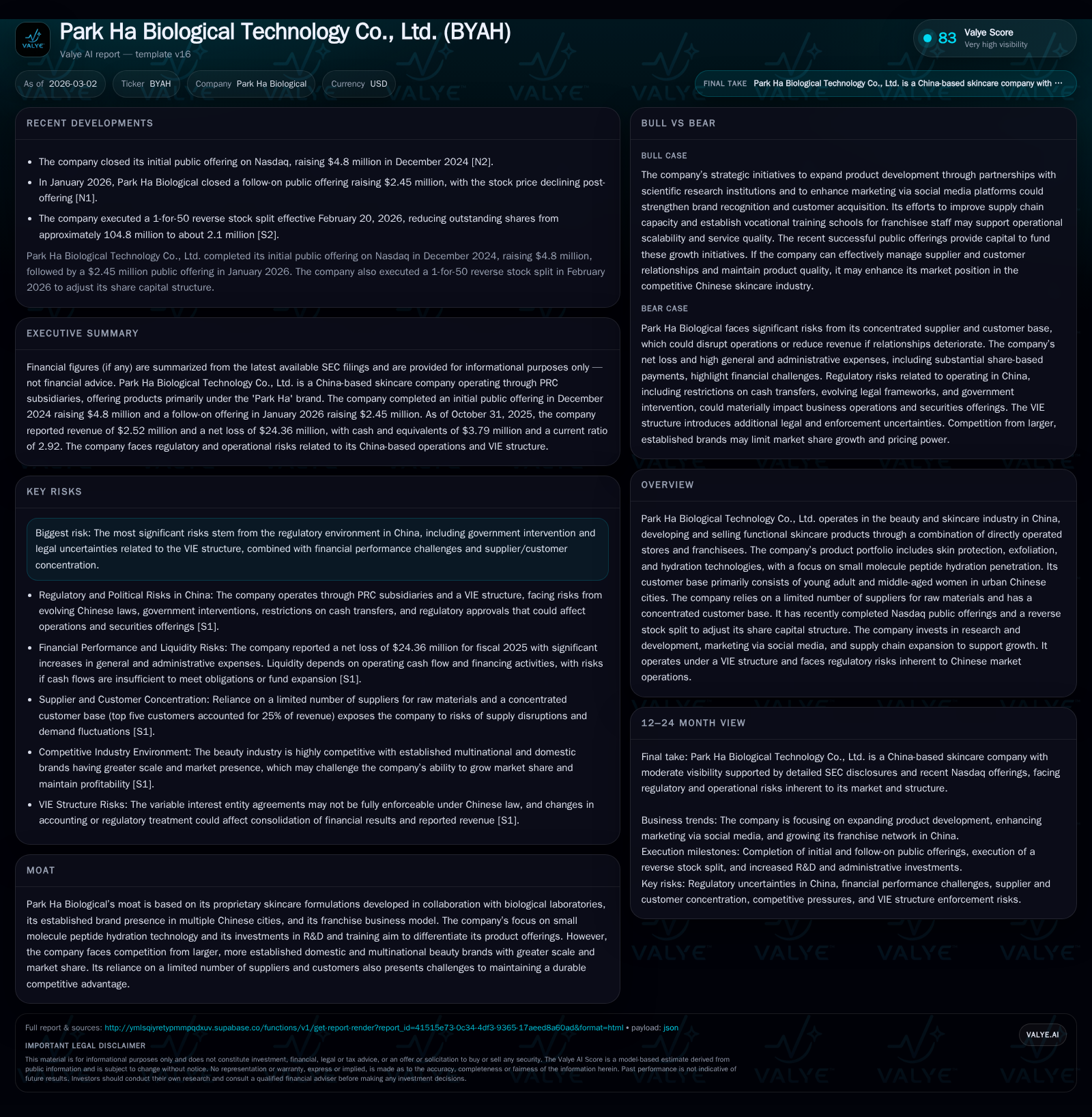

Park Ha Biological Technology has achieved near-6% revenue growth in fiscal 2025, primarily fueled by an expanding franchise footprint across Chinese urban centers and a differentiated product line centered on small molecule peptide hydration technology. Despite top-line progress, the company reported a plunging operating income turning to a $24 million loss and net losses over $24 million in FY25 reflecting sharp rises in share-based payments and professional fees linked to Nasdaq listings and corporate expansion. Park Ha has completed a reverse stock split alongside a $2.45 million secondary offering to strengthen its capital structure. Its reliance on concentrated suppliers and customers, combined with regulatory uncertainties inherent in its VIE structure in China, underscore its operational risks. Continued R&D investments affirm management’s commitment to technological differentiation but also exert near-term margin pressure.

Revenue Momentum Powered by Expanding Franchise Operations

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | -24 | 85852 | -24 | +6.0% | -5191.3% |

| 2024 | 2 | 0 | 960470 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -2973 | -609.9 |

| 2024 | 874901 | 31.8 |

Source: SEC companyfacts cache [F1].

Park Ha Biological Technology’s fiscal year 2025 revenue reached approximately $2.52 billion USD, marking a 6% year-over-year increase from $2.38 billion in FY24 as per [F1], [S1]. This growth was underpinned largely by the company's expanding franchise footprint within urban Chinese markets where its target demographic — mainly young adult and middle-aged women — is concentrated [S7], [S11]. Despite the total number of contracts for franchisees shrinking significantly from 45 in FY24 to just 22 by October 31, 2025, the company managed to maintain sales momentum through deeper market penetration per store and replenishment efforts guided by corporate standards. The shift reflects a strategic consolidation focusing on high-performance franchise outlets under the "Park Ha" brand name while simultaneously investing in directly operated stores.

The company's product portfolio emphasizes functional skincare solutions that incorporate small molecule peptide hydration penetration technology. Collaborations with biological laboratories have endowed Park Ha with proprietary formulations across nearly 70 SKUs spanning skin protection, exfoliation, sebum film repair, microecological balance, and anti-aging categories [S7], [S12], [N#]. This formulation edge aims to differentiate it from large domestic and multinational competitors dominating China's crowded beauty space [S28].

Financial Strains: Operating and Net Income Volatility

Despite revenue advances, operating results depict considerable tension within Park Ha’s cost structure and expense base. Operating income swung from a positive margin of $793K in FY24 into a deeply negative figure of roughly -$24.15 million USD in FY25 representing over a -3000% decline year-over-year [F1], [S1]. Net income followed suit falling from a modest gain of $479K in FY24 into a broad loss surpassing -$24.36 million for FY25 [F1]. This unprecedented operating loss reflects substantial escalation in general and administrative expenses — notably an extraordinary share-based payment expense totaling approximately $24 million connected with stock compensation issued around the Nasdaq listing process plus elevated professional fees supporting investor relations efforts [S17].

Margin pressures also relate to rising selling and marketing spend which nearly doubled from ~ $361K in FY24 to over $625K in FY25 — corroborating an aggressive push for brand visibility via social media campaigns [S1], alongside forecasted underlying cost increases from expanded retail presence. Moreover, cost of revenues declined materially from prior periods indicating some operational efficiencies or product mix optimization [F1], albeit overshadowed by the non-recurring headline expense items distorting profitability metrics.

Return on equity plummeted accordingly producing an approximate -610% based on latest net income relative to equity of $3.99 million at fiscal year-end [F1]. The steep decline signals immense financial strain amid scaling efforts without commensurate operational leverage.

R&D Innovation Focus: Small Molecule Peptide Technology

Park Ha Biological continues prioritizing research and development investments as a core pillar of its differentiation strategy within the intensely competitive Chinese skincare market. R&D expenditures swelled fivefold between FY24 ($36.7K) and FY25 ($238K), partially fueled by new initiatives such as cell therapy – an area signaling advanced bioactive innovation adjacent to peptide formulations – along with increased acquisition of raw materials specialized for novel products [F1], [S6], [S17].

The company attributes its moat primarily to these proprietary peptide hydration technologies developed jointly with biologically focused laboratories that enhance dermal penetration efficacy and hydration retention beyond standard cosmetic treatments [S28]. The commitment to ongoing scientific refinement underscores management's view that sustained technological leadership could mitigate competitive pressures posed by larger beauty conglomerates.

However, while such R&D dedication lays groundwork for medium-to-long-term brand value enhancement, these expenditures currently contribute additional overhead without immediate scale sales offsetting their cost impact.

Nasdaq Public Offerings and Reverse Stock Split Impact

During early 2026, Park Ha successfully completed a best-efforts follow-on public offering raising approximately $2.45 million USD gross proceeds at an issuance price near $0.11 per Unit featuring Class A ordinary shares plus warrants exercisable up to one year post-issuance [N1], [S4]. This capital raise explicitly targets funding expansion of directly operated store networks across China enhancing geographic reach beyond existing franchisees.

Simultaneously, the company implemented a critical capital structure adjustment through a formal 1-for-50 reverse stock split effective February 20, 2026 following requisite shareholder approval on December 26, 2025 [S2], [S3]. This corporate action reduced outstanding shares from roughly 104.8 million pre-split units down to about 2.1 million post-split shares aiming at compliance with Nasdaq minimum bid price rules while potentially improving marketability.

This dual maneuver seeks stable foundation for future equity financing options while addressing fragmented share capital complexities inherent after earlier IPOs combined with warrant exercises.

Capital Structure, Liquidity, and Cash Flow Dynamics

Liquidity metrics portray cautious stability amid operational deficits. As of October 31, 2025 the company held close to $3.79 million USD in cash equivalents with current assets totaling approximately $5.5 million versus current liabilities of about $1.88 million yielding a healthy current ratio near 2.92x suggesting short-term liquidity sufficiency [F1], [S13].

Operating cash flow dramatically contracted by more than 91% YoY down to roughly $85.9K compared with nearly one million USD generated in FY24 reflecting net loss pressures impinging working capital cycles or collections efficiency during store footprint transitions [F1], [S13]. Capital expenditures remained stable growing marginally around +4%, approximately $88K supporting maintenance or selective expansion capex rather than large-scale asset buildup typical for retail rollout phases [F1], [S6].

The resulting free cash flow measured as CFO minus capex registered slightly negative $(3)K illustrating tight cash conversion dynamics where reinvestment priorities constrain discretionary spending power amid losses.

Dividend payments have not been distributed historically nor are planned given persistent negative profitability and reinvestment focus detailed by management communications [S4], emphasizing capital allocation toward growth initiatives rather than returning cash.

No share repurchases are underway highlighting prioritization on preserving cash balances during scaling.

Risk Landscape: Regulatory Complexities and Dependence on Suppliers

Park Ha operates under a Variable Interest Entity (VIE) structure placing it in China’s particularly complex regulatory environment characterized by opaque enforcement nuances affecting dividend distribution ability and cross-border capital movement constraints as described extensively in filings [S15], [S16]. The PRC government’s tightening scrutiny over overseas-listed Chinese companies combined with emergent cybersecurity laws impose scrutiny risks impacting operational continuity or forcing compliance costs.

Supplier concentration risk is meaningful; two main suppliers represented circa 37% combined purchasing volume last fiscal year raising exposure if either fails contract terms or disrupts supply chain continuity amid increasing raw material volatility seen broadly across personal care sectors post-COVID supply dislocations [S18]. On customer side top five clients account for roughly one-quarter of revenue indicating concentration risk that could amplify volatility if demand patterns shift rapidly or payment collection challenges emerge given franchisee financial stress noted through increased credit loss allowances on receivables from franchisees rising markedly year-over-year [$232K allowance vs approximately $56K prior] demonstrating fragility among smaller channel partners within the ecosystem [F1], [S14].

Moreover geopolitical tensions between US-China regulatory frameworks may delay audits or escalation procedures complicating transparency for shareholders abroad alongside SEC delisting threats related to emerging U.S. audit reform mandates impacting all Chinese ADRs via HFCAA rules which remain unresolved sources of uncertainty that investors must monitor closely.

Outlook: Growth Prospects Balanced Against Key Constraints

Management signals intent toward broader geographic expansion emphasizing second-tier cities within China leveraging direct operations complemented by franchising leveraging digital marketing channels tailored towards urban professionals aligning offerings with evolving consumer preferences documented through internal surveys showing predominantly female clientele (~92%) residing near commercial hubs capable of discretionary premium skincare spend [N#, S7]. Pipeline developments revolve around launching male-targeted brands alongside continued investment into bio-peptide innovations reinforcing product differentiation hopes consistent with disciplinary focus established last year.[N1], [S1]

Nonetheless growth optimism is tempered against myriad headwinds: fierce competition from entrenched domestic players supported by multinational brands possessing superior scale economies; regulatory unpredictability affecting financial structuring; supplier concentration shocks; plus fixed cost leverage challenges as indicated by recent wide operating losses limiting near-term profit generation feasibility.

The path forward depends heavily on effective execution balancing aggressive expansion with rigorous cost controls including managing SG&A scaling effects prompted by stock-based compensation charges which illustrated sensitivity of profitability metrics when bond-like expenses emerge during capital market transitions.

What to Watch: Market Penetration, Regulatory Signals, and Capital Deployment

Key milestones include tracking quarterly changes in franchise contract counts assessing whether recent retrenchment shifts toward sustainable unit economics reflecting healthier average store productivity or further portfolio pruning will be necessary. Monitoring U.S.-China regulatory developments impacting VIE structures especially relating to annual audit approvals under HFCAA regulations remains critical given their potential influence on trading status and shareholder confidence. Additionally watching subsequent equity or debt capital transactions beyond recent follow-on offerings will shed light on financial runway sufficiency considering cash burn requirements from ongoing R&D investments plus incremental store openings. Dividend policy evolution could serve as proxy indicator for future free cash flow normalization but remains unlikely until sustained profitability emerges. Finally continued innovation newsflow regarding proprietary peptide technologies or product line expansions targeting underserved market segments such as male consumers offers qualitative insight into pipeline vitality.

This analysis is based solely on publicly available filings including audited financial data as of March 2026 without incorporating any non-public information or providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments