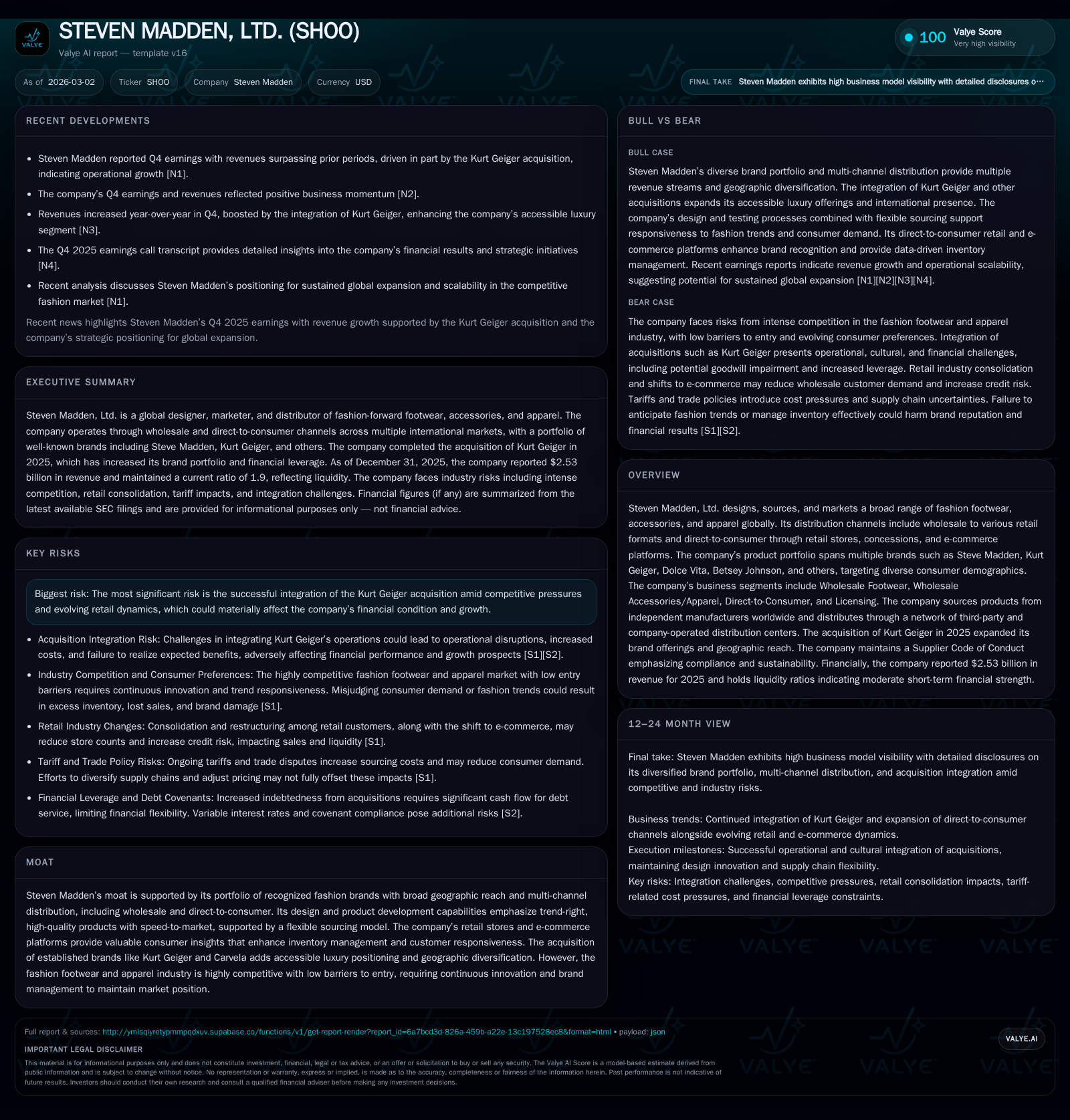

Steven Madden’s 2025 Growth Largely Fueled by Kurt Geiger Acquisition Challenges in Profit Margins

The company’s extensive brand portfolio and multi-channel reach underpin top-line gains while operating income contraction highlights integration and cost pressures.

Steven Madden, Ltd. achieved notable revenue growth in 2025 driven primarily by the acquisition of Kurt Geiger, which also expanded its international footprint and brand breadth. However, operating income declined sharply despite higher sales, reflecting increased costs associated with the acquisition and heightened competitive and supply chain challenges. Cash flow generation remains positive but has weakened compared to prior years amid elevated capital expenditures for growth initiatives. The company’s flexible sourcing model, strong design capabilities, and diverse distribution channels support future growth, though successful integration and evolving retail dynamics will be critical to sustaining momentum.

Company Overview and Business Model

Steven Madden, Ltd. operates globally as a designer, marketer, and distributor of fashion footwear, accessories, and apparel with multiple well-known brands including its flagship Steve Madden line alongside Kurt Geiger (acquired mid-2025), Dolce Vita, Betsey Johnson, Carvela, ATM, Blondo, and Anne Klein (licensed). The company's products are sold through wholesale channels—targeting department stores, specialty retailers, mass merchants—and direct-to-consumer outlets spanning company-operated stores, concessions in international department stores, and e-commerce platforms across North America, Europe, Asia-Pacific regions, and beyond [S1][S12][S16].

Its flexible outsourcing model leverages independent manufacturers worldwide across China (majority at 56% of purchases in 2025), Cambodia (~25%), Vietnam, Mexico, Brazil, India and others without long-term supplier contracts or facility ownership. This approach supports rapid response to fashion trends but exposes it to global supply chain fragility [S5][S22].

Historical Performance and Financial Overview

Steven Madden reported steady revenue growth over recent years interrupted by margin compression in 2025. Revenue climbed from approximately $2.28 billion in 2024 to $2.53 billion in 2025—a robust 11% increase primarily attributable to the strategic acquisition of Kurt Geiger in May 2025 expanding product offerings particularly into accessible luxury segments as well as increasing geographic diversification predominantly in the U.K. [F1][S2].

However, operating income plummeted by more than 64%, from $225 million in 2024 down to $81 million in 2025 [F1]. This dramatic decline contrasts sharply with top-line strength and reflects significant integration costs associated with the Kurt Geiger acquisition alongside pressure from tariffs affecting input costs and freight inflation [S19][S8]. Net income figures (latest available only through FY20) have historically exhibited volatility but showed some upward momentum pre-acquisition [F1].

Operating cash flow decreased nearly 18% to $162 million with free cash flow—after a notable rise in capital expenditures related to store build-outs and technology investments—contracting accordingly yet remaining positive [$119 million FCF] [F1]. Dividend payments held steady around $61 million annually; however share repurchases were scaled back sharply following prior years’ aggressive buybacks signaling a recalibrated capital allocation mix favoring debt management post-acquisition [F1][S8].

Historical performance (annual)

| FY | Rev ($bn) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 2.5 | 162 | 81 | 43 | +11.0% |

| 2024 | 2.3 | 198 | 225 | 26 | +15.2% |

| 2023 | 2.0 | 229 | 213 | 19 | -6.6% |

| 2022 | 2.1 | 268 | 282 | 16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 61 | 14 | 120 |

| 2024 | 61 | 98 | 172 |

| 2023 | 63 | 142 | 210 |

| 2022 | 66 | 149 | 252 |

Source: SEC companyfacts cache [F1].

Revenue growth percentages reflect year-over-year changes where available; operating income fluctuations illustrate increasing cost pressures.

Strategic Developments & Future Growth Prospects

The pivotal event shaping Steven Madden's recent results is the May-2025 acquisition of Kurt Geiger which broadened portfolio depth into accessible luxury categories such as high-end footwear and handbags while granting greater UK/EU exposure [N3][S2][S13]. The acquisition is expected to enhance global brand presence and provide scalable synergies through shared sourcing and distribution platforms.

Growth drivers include:

- Continued expansion of direct-to-consumer channels emphasizing digital commerce capabilities leveraging seven branded e-commerce sites.

- Accelerated product innovation fueled by strong design teams focusing on trend-right styles appealing across diverse demographics.

- Geographic expansion supported by existing joint ventures and concessions across emerging markets including South Africa and Asia-Pacific.

- Integration and cross-pollination of brands such as Carvela offers cross-selling opportunities.

Challenges that could cap growth:

- Successful integration of Kurt Geiger remains uncertain with incurred costs weighing on profitability.

- Intense competition from both niche fashion companies and large diversified apparel/shoe firms constrains pricing power.

- Supply chain disruptions heightened by geopolitical risks (including tariffs on Chinese imports), freight cost inflation, and dependency on third-party manufacturers without long-term contracts.

- Retail sector consolidation may reduce wholesale customer breadth; increasing shift to e-commerce requires continuous adaptation.[S1][S6][S19]

Monitoring performance against milestones such as profitability improvement post-Kurt Geiger integration, inventory turnover rates amidst fashion cycles, digital sales penetration growth will be critical indicators going forward; specific public guidance remains limited [N12][N4].

Capital Allocation & Returns Analysis

Steven Madden’s balance sheet reflects a meaningful increase in leverage tied primarily to the $300 million term loan secured for the Kurt Geiger deal plus a revolving credit facility initially used sparingly [S8]. Debt service obligations constrain free cash deployment potentially impacting dividends or share repurchases.

Return on equity is subdued at approximately 2.6% for FY25 due to lower net income relative to equity base boosted by goodwill from acquisitions [F1]. Despite this modest ROE metric:

- The company maintains a consistent dividend policy distributing roughly $60 million annually indicating a focus on shareholder returns.

- Share repurchase activity has markedly declined likely prioritizing debt reduction and operational investment after prior higher buyback levels.

- Capital expenditures have risen significantly (+65% YoY) underlining reinvestment into physical retail stores plus technology infrastructure enabling omnichannel synergy [F1][S16].

Industry Context & Competitive Positioning

Steven Madden's moat stems from its multi-brand strategy combining trend-forward offerings with core classic styles catering primarily to women aged broadly across young adults to middle age segments worldwide [S12]. The ability to swiftly bring fashion-right designs from conception through manufacturing to market via an agile supply chain adds competitive advantage.

However:

- Fashion footwear/accessories is notoriously volatile with rapid consumer preference shifts requiring constant innovation.

- Barriers to entry remain low inviting new competitors continually pressuring market share.

- Industry consolidation among retailers places additional risk on wholesale revenue streams.

- Tariff regimes introduce cost uncertainties especially for China-sourced goods vital to >50% of production [S19][S22].

Integration of acquired businesses like Kurt Geiger will test execution capabilities amid these intensifying headwinds.

Risks Highlighted By Management

Management discloses several key risks that could materially impact financial health including:

- Failure or delay integrating Kurt Geiger's operations raising costs or diluting brand equity.[S2]

- Credit risk stemming from retailer bankruptcies or consolidations reducing orders.[S10]

- Supply chain interruptions caused by geopolitical tensions or labor unrest at ports impacting delivery timelines.[S23]

- Tariffs elevating costs potentially forcing product price increases reducing competitiveness.[S19]

- Litigation or intellectual property challenges although currently judged unlikely to have material effects.[S7]

- AI implementation risks related to data integrity or regulatory compliance could disrupt operational decision-making.[S20]

Conclusion & Outlook Considerations (Analysis)

Steven Madden enters post-acquisition phase facing the nuanced challenge of translating expanded scale into sustainable profit improvement. The top-line momentum fueled by Kurt Geiger affirms strategic directional merit yet clearly integration expense pressure along with macroeconomic factors curtailed operating profitability markedly last fiscal year.

Watch points for assessment going forward include effective synergy capture from brand blending, management’s ability to tighten gross margins amid supply uncertainty and inventory agility improvements particularly in e-commerce fulfillment efficiency. Additionally, managing elevated leverage prudently alongside allocating capital between organic investments versus shareholder returns will shape financial flexibility.

While dividend continuity supports return stability shareholders accustomed to stronger prior buybacks may observe recalibrated distributions until earnings robustness is restored.

The environment remains competitive emphasizing that Steven Madden's enduring relevance depends on preserving brand resonance combined with nimble execution against evolving consumer tastes worldwide.

This report is based solely on publicly available information as of March 2, 2026 including SEC filings [F1], news releases [N#], and regulatory disclosures without provision of investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments