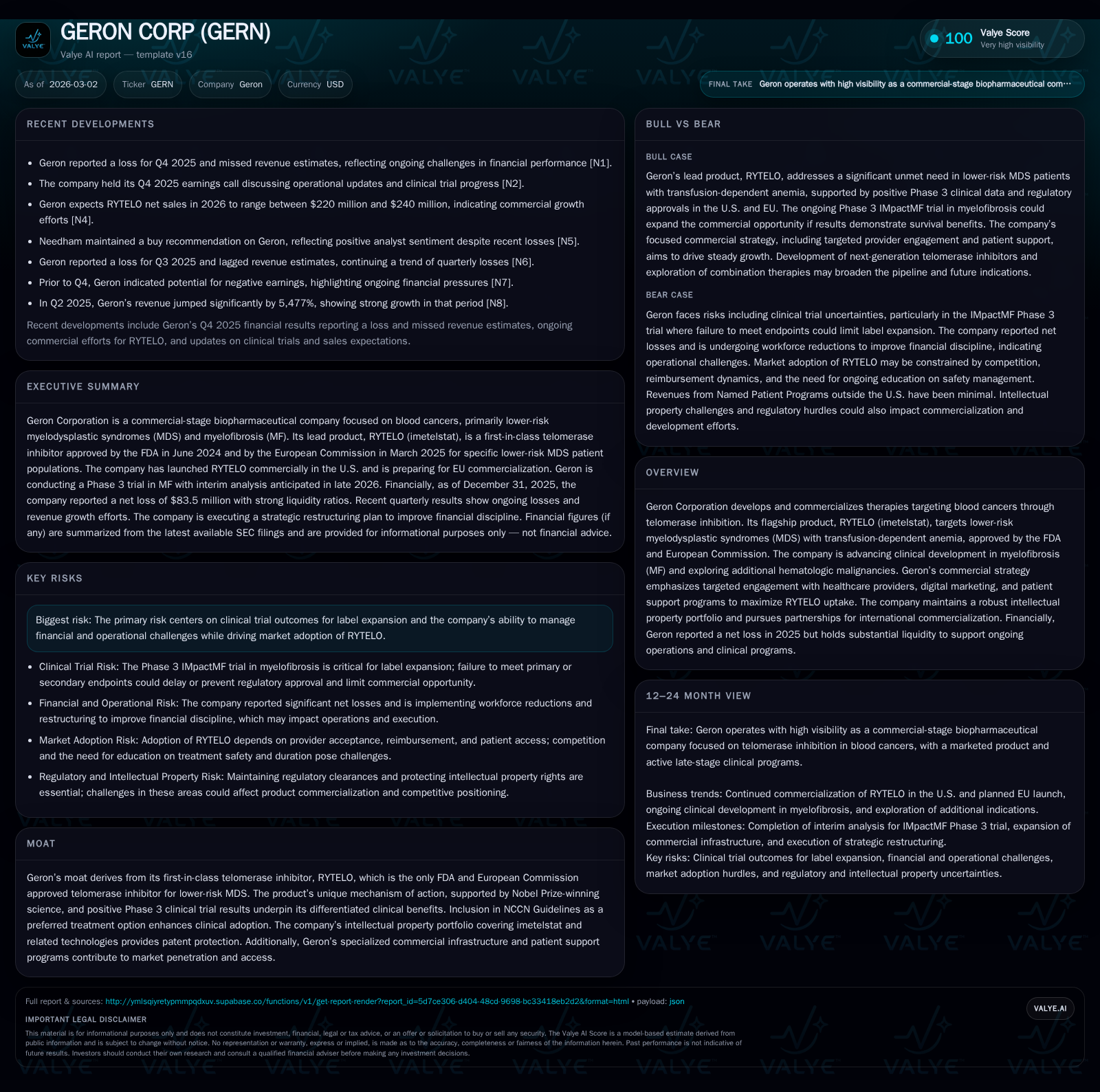

Geron Corp’s RYTELO Commercialization and Clinical Trials Define Growth Amid Financial Losses

Geron focuses on expanding its telomerase inhibitor franchise despite ongoing net losses and operational challenges.

Geron Corporation, a commercial-stage biotech company, is advancing growth through the commercialization of its first-in-class telomerase inhibitor, RYTELO (imetelstat), approved for lower-risk myelodysplastic syndromes (MDS). The company launched RYTELO in the U.S. in mid-2024 and secured European Commission approval in early 2025, with plans to extend market access internationally. Alongside commercialization efforts, Geron progresses its phase 3 IMpactMF trial in relapsed/refractory myelofibrosis (MF), with interim overall survival data expected in late 2026. Despite promising clinical data and strong intellectual property protections, Geron reported significant net losses and negative operating cash flows as of fiscal 2025 but maintains ample liquidity to support ongoing development and commercialization initiatives.

Company Overview and Strategic Positioning

Geron Corporation has transitioned from clinical-stage research to a commercial-stage biotech entity focused on hematologic malignancies through its pioneering telomerase inhibitor platform. The company’s flagship therapy, RYTELO® (imetelstat), embodies Nobel Prize-winning science targeting the enzyme telomerase to inhibit malignant cell proliferation while potentially modifying disease progression [S11][S14].

After FDA approval on June 6, 2024 for adult patients with low- to intermediate-1 risk myelodysplastic syndromes (lower-risk MDS) suffering from transfusion-dependent anemia not responsive or ineligible to erythropoiesis-stimulating agents (ESAs), Geron orchestrated a U.S. commercial launch [S11]. The European Commission granted marketing authorization in March 2025 for essentially the same population excluding those with isolated deletion 5q cytogenetic abnormality—a niche where alternative treatments exist—covering all EU states plus Iceland, Norway and Liechtenstein [S11][S12].

Lower-risk MDS is a progressive blood disorder predominantly affecting elderly patients where anemia is the most significant clinical problem leading to transfusion dependency. Serial transfusions pose risks such as iron overload associated with worsened survival outcomes [S17]. RYTELO addresses this unmet medical need by demonstrating statistically significant benefits—including over eight weeks red blood cell transfusion independence—in the pivotal Phase 3 IMerge clinical trial [S16][S17].

Historical Financial Performance

Financially, Geron has operated at a loss consistent with many biotech firms transitioning to early commercialization while advancing multiple clinical assets. The company reported minimal revenues historically due to pre-commercialization stages but recorded operating losses as it scaled operations [F1]. Notably:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -83 | -111 | -69 | +52.2% | |

| 2024 | -175 | -219 | -174 | 680000 | +5.2% |

| 2023 | -184 | -168 | -194 | 830000 | -29.8% |

| 2022 | -142 | -127 | -139 | 431000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -37.0 | |

| 2024 | -219 | -62.3 |

| 2023 | -169 | -74.3 |

| 2022 | -128 | -177.4 |

Source: SEC companyfacts cache [F1].

(Figures for revenue are minimal or not material post-2017 reflecting early sales start; operating income shows improving losses indicating some efficiency gains though still negative) [F1].

Operating cash flow remains negative due to substantial investment in commercialization infrastructure and clinical advancement. Capital expenditures are modest relative to overall spend typical for a pharmaceutical developer without heavy manufacturing assets. Equity increased sharply through capital raises supporting development programs prior to slight decline at FY25 end due to accumulated losses [F1].

Commercial Execution and Market Penetration

Geron's commercial strategy for RYTELO is finely tuned toward maximizing penetration within eligible U.S. patient populations:

- Targeted engagement with high-volume healthcare providers focusing on earlier treatment lines enhances prescriber awareness.

- Emphasis on digital marketing channels and third-party educational platforms ensures consistent messaging.

- Cross-functional teams exceeding sixty members including key account managers and regional directors provide comprehensive coverage.

- The REACH4RYTELO™ patient support program facilitates access addressing payer challenges.

The National Comprehensive Cancer Network (NCCN) Guidelines list imetelstat as a Category 1 preferred treatment option at second-line ESA-ineligible segments regardless of ring sideroblast status—a significant endorsement enhancing physician adoption confidence [S14]. In October 2025 updates replaced azacitidine with imetelstat as preferred therapy among first-line RS-negative ESA-ineligible patients further expanding market opportunity [S14].

Following European approval in early 2025 Geron partners with Tanner Pharma to facilitate Named Patient Programs outside the U.S., though revenues from these remain minimal so far. Planned commercialization across select EU markets leverages experienced collaborators managing reimbursement and Health Technology Assessment submissions essential for pricing negotiations [S10][S12].

Pipeline Development and Clinical Milestones

Beyond lower-risk MDS indications addressed by RYTELO's approved label Geron pursues label expansions via ongoing studies:

- IMpactMF Phase 3 Trial: Pivotal study evaluating imetelstat in relapsed/refractory myelofibrosis patients post-JAK inhibitor therapy failure—an area with high unmet medical need. Approximately completed enrollment by September 2025; interim overall survival analysis expected second half of calendar year 2026 with final readout anticipated late-2028 [S10][S28].

- IMproveMF Trial: Phase 1 study investigating combination of imetelstat with ruxolitinib as frontline therapy across intermediate-to-high-risk MF groups aiming for synergistic effects [S19].

- Investigator-led Studies: Phase1/2 trials exploring combinations with hypomethylating agents ± venetoclax for relapsed/refractory acute myeloid leukemia represent potential additional indications leveraging telomerase inhibition mechanism [S8][S14].

- Discovery programs targeting next-generation oral telomerase inhibitors aim at improved formulations potentially broadening future applicability beyond intravenous imetelstat [S8].

Phase2 IMbark data demonstrate compelling efficacy signals including median overall survival approximately doubling historical outcomes post-ruxolitinib failure along with molecular marker reductions and symptom improvement suggesting possible disease modification unlike existing therapies [S18][S21]. Safety profiles remain manageable featuring reversible thrombocytopenia/neutropenia consistent with prior studies [S18].

Financial Positioning and Capital Allocation

Despite recent net losses reflecting investment-heavy development combined with nascent commercial ramp-up, Geron maintains financial resilience:

- Cash & equivalents totaled approximately $77.6 million at fiscal year-end December 31, 2025 providing operational runway.

- Current assets exceed $520 million versus current liabilities near $112 million yielding a strong current ratio around ~4.7 indicating solid short-term liquidity [F1].

- A senior secured loan agreement amended January 2026 extends optional drawdowns totaling up to $250 million across three tranches subject to revenue milestones providing flexible capital sourcing options for expansion needs [S15][S20].

- No dividends or share repurchases have been declared; capital allocation prioritizes reinvestment into clinical research and commercialization scale-up consistent with stage norms [F1][S22][S23].

Financial discipline remains critical given ongoing operating outflows ($68.5 million operating loss FY25; negative operating cash flow exceeding $111 million) though improving trends indicate some containment versus prior years’ heavier losses linked to late-stage product development phases [F1].

Risks Summary

Key risks include:

- Clinical Development Outcomes: Success of label extensions especially IMpactMF Phase3 overall survival endpoint is pivotal; failure or delay could materially affect valuation.

- Commercial Adoption: Market uptake depends on physician willingness tempered by entrenched standards such as ESAs or supportive care.

- Regulatory Environment & Patent Protection: Maintaining exclusivity via robust intellectual property portfolio amid competitive pressures targeting hematologic oncology.

- Financial Sustainability: Managing funding requirements until profitable scale demands stringent capital stewardship amidst commercialization uncertainties.

- Operational Execution: Effective coordination across sales teams alongside complex clinical programs is essential.

- Cybersecurity Governance: Board oversight of IT security risk management underpins safeguarding proprietary data crucial for biotech innovation pipelines [S9].

Outlook: Monitoring Catalysts and Growth Drivers

Near-term focus centers on IMpactMF interim overall survival results expected second half of calendar year 2026 which could significantly influence labeling expansion enabling access into intermediate-to-high-risk MF segment—a substantial market given limited post-JAK inhibitor options.

International expansion beyond Named Patient Programs into deeper European markets offers growth potential but entails reimbursement challenges requiring strategic partnerships as indicated by plans not to self-commercialize outside U.S.[S12]. Enhanced payer access strategies domestically anchored by differentiated efficacy claims supported by NCCN guideline revisions may gradually increase new patient starts mitigating initial launch challenges.[S14]

Progression of pipeline candidates including combination therapies or oral formulations can diversify future revenue streams reducing dependence on single product sales.

In summary, GERN stands at an inflection point where scientific innovation underpins unique product differentiation centered on disease modification contrasting traditional symptom management approaches prevalent within hematologic malignancies landscape. Their ability to translate positive clinical outcomes into sustainable revenues while controlling costs will dictate their trajectory from developmental biopharma entity toward established oncology therapeutics player.

This report synthesizes available public filings and news reports without providing investment recommendations or price targets. Readers should consider this analysis informational rather than advisory.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments