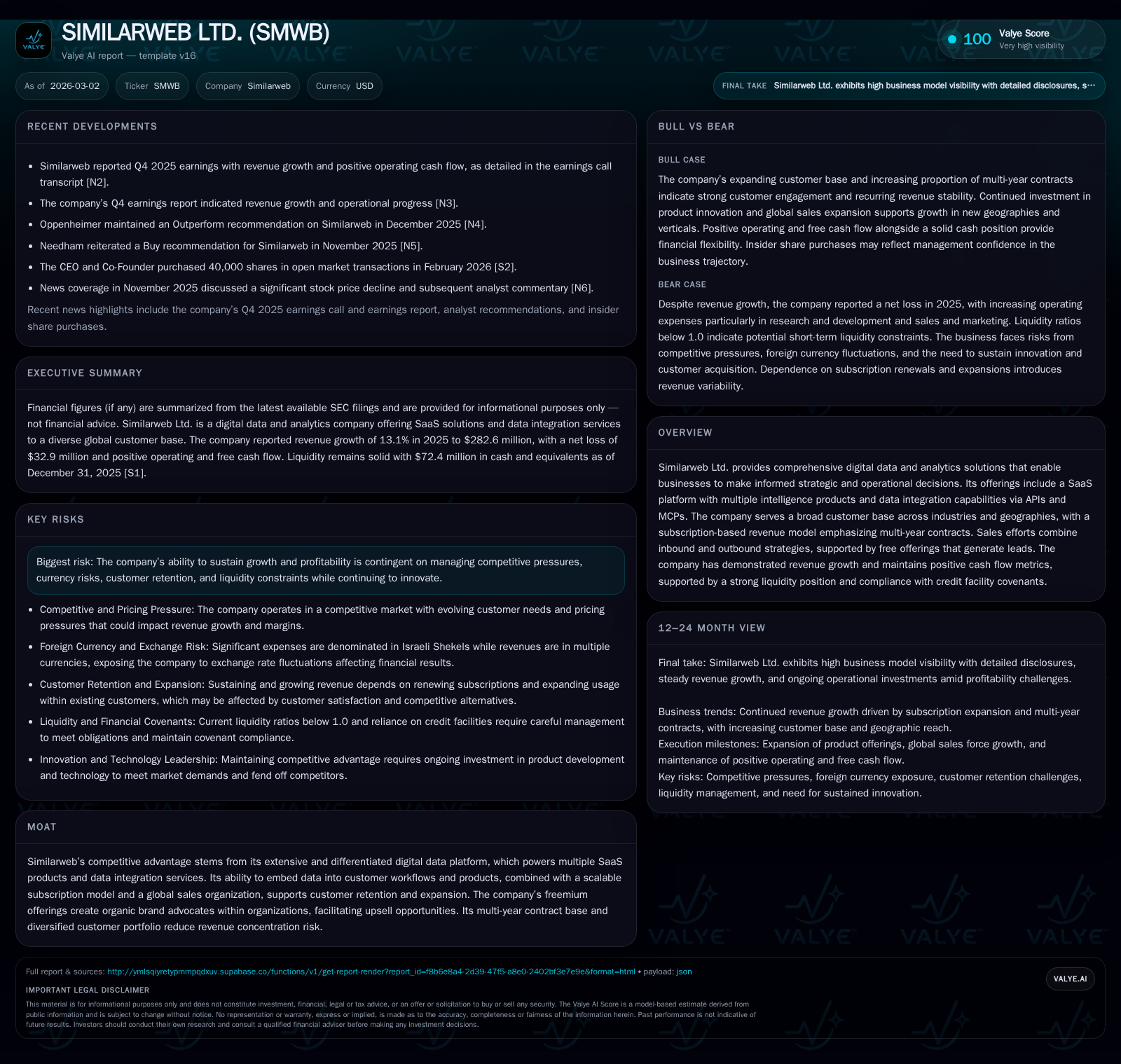

Similarweb Ltd. Expands Digital Intelligence SaaS with Growing Multi-Year Contracts Amid Profitability Challenges

Subscription revenue growth and broader customer base support positive cash flow despite escalating operating losses in 2025.

Similarweb Ltd. continues to develop its digital data analytics platform, experiencing steady revenue increases fueled by expanding enterprise adoption and multi-year contractual commitments. The company’s differentiated freemium model and API integration capabilities underpin customer retention and upsell opportunities. However, rising research, sales, and marketing expenses contributed to wider net losses in 2025, even as free cash flow remained positive. Liquidity is supported by a strong cash position and undrawn credit facility. Investors should monitor customer expansion, product innovation, and margin improvement as key milestones.

Company Overview

Similarweb Ltd., founded in 2009 and headquartered in Israel, delivers comprehensive digital data intelligence solutions through a SaaS platform suite that enables businesses globally to make strategic decisions using web and app usage data [S1][S6]. Its core asset is Similarweb Digital Data — a proprietary estimate of online actions across websites/apps — which feeds several product lines such as Web Intelligence, App Intelligence, Retail Intelligence, Sales Intelligence, and Stock Intelligence.

The firm blends direct user-facing analytics tools with Data as a Service (DaaS) offerings including APIs and customized datasets that integrate into customers’ BI workflows or machine learning frameworks [S1][S6]. This data business model is complemented by advisory services tailored to enterprise clients requiring bespoke analytics solutions.

Historical Growth and Performance

Between 2023 and 2025, Similarweb has demonstrated consistent top-line expansion. Revenues grew from $218 million in 2023 to $249.9 million in 2024 (+14.6%) then further increased by 13.1% to reach $282.6 million in 2025 [F1]. This growth was driven largely by subscription sales during the firm’s strategy to deepen penetration within existing accounts and broaden its global customer base:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -33 | 15 | -24 | 1 | -187.5% |

| 2024 | -11 | 30 | -10 | 1 | +61.0% |

| 2023 | -29 | -3 | -29 | 2 | +64.9% |

| 2022 | -84 | -46 | -88 | 28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 13 | -141.2 |

| 2024 | 29 | -41.6 |

| 2023 | -5 | -188.9 |

| 2022 | -74 | -381.1 |

Source: SEC companyfacts cache [F1].

Operating Income YoY % calculated as change from prior year; Free Cash Flow calculated as Operating Cash Flow minus Capex [F1]

The gross margin improved slightly to 79.5% in 2025 from 78.1% in prior year due to effective leveraging of cloud infrastructure and more efficient data acquisition processes [S10][F1]. However, operating expenses escalated significantly across all categories — research & development spending increased by over 30%, reflecting headcount growth primarily for engineering and data science teams including a Prague site expansion; sales & marketing expenses grew by more than 17%, underlying aggressive investment in both inbound/outbound channels plus account management to drive upsells; general & administrative costs also rose moderately [F1][S10][S25]. These investments pressured profitability despite growing revenues.

Business Model Drivers

Similarweb employs a subscription-based SaaS model supplemented by transaction-based data contracts and ancillary advisory services [S6][S7]. Pricing tiers are stratified based on solution complexity, geographic coverage, user seats, and feature sets with typical contract terms of one year or longer.

A distinct advantage lies in its multi-faceted data delivery:

- A robust software platform provides actionable insights directly to end-users ranging from marketers and analysts up to executives.

- Data integration via APIs allows embedding into enterprise ecosystems powering automated decisioning pipelines.

- Enabling customers to embed bulk Similarweb data into their own products creates an ecosystem dynamic enhancing stickiness [S1].

The company strengthens pipeline efficiency by employing freemium offerings accessible via its website and proprietary browser extension that attract millions monthly while generating hundreds of thousands of qualified leads funneling into paid tiers—a critical mechanism for organic brand advocacy within organizations [S7][S13].

Customer Base & Geographic Expansion

As of December 31, 2025, Similarweb had grown its paying customer base to over 6,100 entities, up nearly 11% from approximately 5,530 the prior year [S11]. Notably:

- U.S.-based customers rose more sharply, bolstering revenue from this region which accounted for approximately $154 million (~55% of total revenue).

- Europe/UK segment also expanded marginally with revenues reaching about $70 million.

No single customer accounts for more than 10% of total revenue, indicating diversified client exposure across industries such as technology, finance, retail, apparel, household products as well as institutional investors [S13]. Approximately two-thirds of ARR originates from multi-year agreements providing revenue durability with recognized upsell pathways through seasoned account managers fostering customer success [S6][S11].

Future Growth Prospects

Growth catalysts identified by management focus on further penetrating existing clients through broader feature uptake; expanding geographic presence especially in APAC markets like Japan and Singapore; deepening vertical-specific solutions; advancing AI-driven analytics capabilities; strengthening self-service modules for SMBs; and pursuing strategic acquisitions that complement core data assets or extend use cases [N1][N2][S9][S21].

However, these ambitions must be balanced against competitive dynamics characterized by players offering varying degrees of digital intelligence solutions which may pressure pricing or tenant switching costs [S17]. Currency risk remains notable due to substantial cost concentration in Israeli shekels juxtaposed against USD/GBP/EUR denominated revenues although hedging programs are in place mitigating volatility impacts [S17].

Capital Allocation & Returns

Similarweb remains unprofitable on a GAAP basis with net losses widening sharply to $33 million in FY2025 compared to an $11.5 million loss prior year due mostly to elevated operating expenses inclusive of share-based compensation charges offset partly by lower intangible amortization post-acquisitions [F1][S22]. Despite this, the company generated positive operating cash flow ($14.6 million) sustaining free cash flow around $13 million after limited capital expenditures ($1.49 million) focused on infrastructure investment rather than aggressive expansion capex [F1][S8][S24].

Cash balances rose modestly to $72.4 million at year-end without any drawn debt on its $75 million credit facility—signaling prudent liquidity management despite net current liabilities exceeding current assets somewhat (current ratio approximately 0.76) possibly reflecting deferred revenue recognition norms inherent in subscription businesses [F1][S4][S8].

No dividend distributions or share buybacks have been indicated recently; capital deployment prioritizes R&D scalability plus sales/marketing initiatives designed for longer-term value creation rather than near-term returns enhancement [N2][N3].

Risks Factors Overview

Principal risks hinge on maintaining innovation velocity against evolving industry standards; managing FX-related earnings variability given operational cost bases centralized in Israel; potential intensification of competition leading to pricing pressure or client attrition; scaling global sales teams efficiently; containing cash burn tied to heavy R&D/S&M spend ahead of operating profit realization; cybersecurity/data privacy challenges inherent to large-scale digital data provisioning; regulatory shifts impacting cross-border data aggregation; alongside macroeconomic effects influencing corporate IT budgets affecting spend on analytics platforms.[S17]

Conclusion (No Investment Opinion)

Similarweb Ltd.’s trajectory shows robust top-line momentum underpinned by enlarging SaaS subscriptions fueled through strategic multi-year deals offering better visibility alongside a growing customer footprint particularly in high-value geographies like the U.S.. Despite stretched profitability metrics due to significant reinvestment into technology development and go-to-market expansion efforts during 2025 — evident also in wide net losses — the firm maintains disciplined liquidity supported by positive free cash flow generation.

How efficiently Similarweb translates scale benefits into sustainable margins through operating leverage will be key watching points for stakeholders evaluating its competitive endurance amidst evolving digital intelligence market demands over coming years.

This report is based solely on publicly available information as of March 2026 including SEC filings (20-F), earnings call transcripts, press releases and industry analysis without any predictive forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments