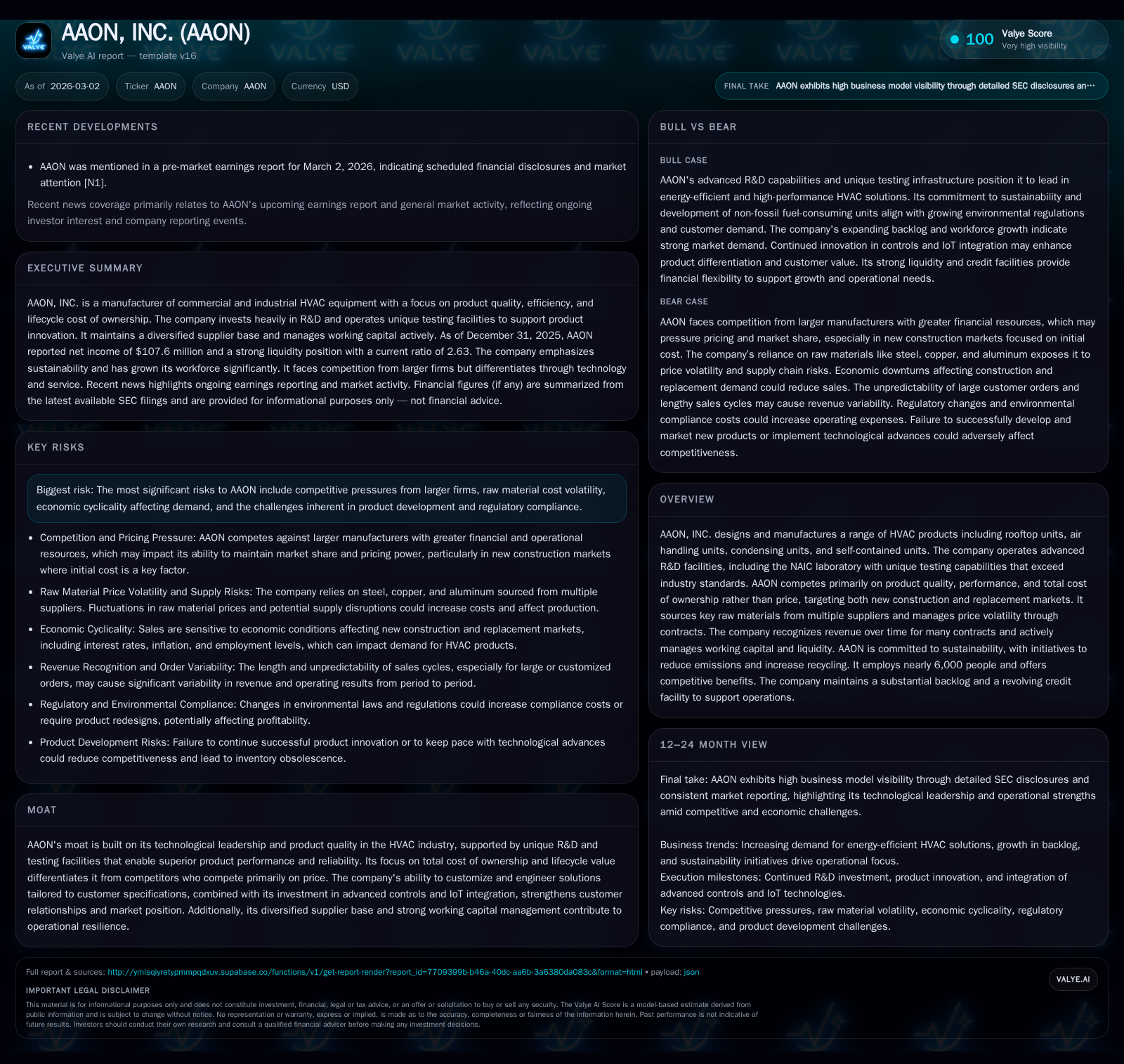

AAON's Technological Edge Supports Resilient Growth Despite Margin Pressure and Cash Flow Challenges

AAON leverages unique R&D capabilities and a strong backlog to navigate competitive pressures and regulatory shifts in HVAC markets.

AAON, Inc. has demonstrated solid growth supported by its advanced engineering and testing infrastructure, helping to differentiate its HVAC products through quality, performance, and lifecycle value. While operating income and net income declined sharply in the latest fiscal year due to margin compression and operational volatility, the company maintains a substantial backlog, expanded credit facilities, and continued investment in innovation and sustainability. Key risks include raw material cost fluctuations, competitive dynamics against larger players, and evolving environmental regulations demanding costly adaptations. AAON's capital allocation reflects prudent dividend payments and share repurchases despite cash flow reductions.

Historical Financial Performance

AAON’s financial trajectory through 2025 reveals a mixture of robust topline momentum backed by product demand and operational challenges. The company recorded operating income of $146.2 million in fiscal year 2025, down from $209.1 million in 2024, representing a decline of roughly 30% year-over-year [F1]. This contraction translated into net income decreasing from approximately $168.6 million in 2024 to about $107.6 million in 2025 (-36.2%) [F1]. The sharper net income drop versus operating income suggests some impact from non-operating expenses or higher interest/other costs.

The precipitous decline in operating cash flow from $192.5 million (2024) to just $0.5 million (2025) is striking; this was accompanied by significant working capital changes tied to the company's large backlog increase and contract billing timing differences [F1,S4,S13]. Resultantly, free cash flow was negative by nearly $54 million after accounting for capital expenditures.

Financial Snapshot Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 108 | 1 | 146 | -36.2% |

| 2024 | 169 | 193 | 209 | -5.1% |

| 2023 | 178 | 159 | 227 | +77.0% |

| 2022 | 100 | 61 | 127 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 33 | 30 | 12.0 |

| 2024 | 26 | 100 | 20.4 |

| 2023 | 26 | 25 | 24.2 |

| 2022 | 23 | 13 | 17.9 |

Source: SEC companyfacts cache [F1].

Operating margins compressed notably despite stable or growing sales volumes due to raw material cost pressures and possibly increased warranty or service-related expenses [S15,S19]. These headwinds coincided with ongoing investments in R&D and expansion of capabilities that AAON pursues as part of its technological moat.

Technological Leadership and R&D Investment

Central to AAON’s strategy is its focus on engineering-driven differentiation rather than competing solely on price against larger peers such as Lennox, Trane Technologies, Carrier Global, Daikin, Johnson Controls among others [S15,S23]. The company touts its North American Innovation Center (NAIC), which features some of the world’s most comprehensive HVAC testing chambers—capable of loading conditions beyond industry norms including sound testing at actual load and extreme environmental conditions like rain, snow, wind up to specific thresholds that competitors generally cannot replicate [S14].

This facility enables AAON to deliver precise customer-validated performance claims allowing premium positioning especially among building owners focused on total cost of ownership rather than upfront purchase prices [S15]. Additional BASX segment R&D efforts complement this work by engineering semi-customized thermal management solutions tailored for niche customer specifications using high-performance components assembled selectively [S11,S14].

R&D spending rose from roughly $43.7 million in 2023 to over $58 million in fiscal year 2025 reflecting sustained commitment to new product development including energy-efficient technologies compatible with evolving refrigerant regulations as well as IoT integration using AI tools for control algorithms advancement [S11,S16].

Backlog Strength and Market Positioning

Contract backlog growth is a critical leading indicator for AAON given many sales are recognized over time aligned with project milestone satisfaction rather than at delivery alone. At December 31, 2025 backlog stood at approximately $1.83 billion—more than doubling from about $867 million a year earlier—which bodes well for near-term revenue visibility albeit with caveats around customer reduction or deferral rights contained within contracts [S4].

The company's market footprint spans commercial HVAC systems targeting both new construction—which remains more price sensitive—and replacement or owner-controlled purchase segments where AAON has gained market share by emphasizing product longevity and lifecycle economics rather than lowest initial equipment cost [S15,S23]. Operational improvements have narrowed prior price gaps making their semi-custom offerings more attractive even amid contractor-driven new builds.

Operational Risks and Raw Material Exposure

Holding multiple raw material suppliers has been instrumental in upholding manufacturing continuity; however steel, copper, aluminum commodity price volatility continues affecting input costs unpredictably [S9,S19]. AAON mitigates this through cancellable/non-cancellable purchasing contracts ranging six to eighteen months but accepts some risk if market prices move rapidly contrary to contracted terms which could lead either to excess inventory costs or foregone savings.

Additional risk stems from reliance on third-party representatives for sales distribution; competitive poaching of channel partners remains a concern particularly versus more resource-rich competitors who may secure exclusive arrangements jeopardizing AAON’s geographic coverage diversity [S10]. Natural disasters near main plant locations including tornadoes pose disruptions albeit partially offset marked by insurance coverage subject to premium hikes.

Cybersecurity threats are increasingly material given digital integration both internally via ERP system upgrades underway as well as external IoT deployments associated with smart HVAC controls [S22,S16]. The firm acknowledges that AI governance protocols must evolve fast enough relative to technological advances or face compliance/legal risks.

Regulatory Compliance and Sustainability Efforts

AAON confronts intensifying environmental regulations requiring costly transitions: notably the US EPA-mandated shift completed January 1, 2025 toward refrigerants with lower global warming potential (R-454B), plus looming state-specific rules such as New York’s regulation mandating <10 GWP refrigerants by early next decade imposing further R&D burdens . Such patchwork regulations may inflate production complexity and costs.

In response AAON pursues sustainability rigorously—achieving Platinum level status twice consecutively on an industry Sustainability Alliance Scorecard benchmarking energy use and material management—and continuing investment in renewable energy sourcing (~36% currently), waste diversion programs involving metal recycling exceeding 17 thousand tons annually across plants, paint byproduct recycling partnerships, LED lighting retrofits across sites plus behavioral energy efficiency enhancements [S17,S20,S26].

AAON also steadily increases proportion of non-fossil fuel consuming units indicating alignment with broader electrification trends despite uncertain regulatory timing around natural gas/petroleum fuel phase-outs affecting historic core gas-fired product lines.

Capital Structure and Returns

Balance sheet management appears conservative: current ratio stands solidly above par at roughly 2.63x reflecting healthy liquidity though cash & equivalents rest modest ($13k) due partly to elevated working capital absorption tied to backlog scaling [F1]. Long-term leverage is supported by a recently expanded revolving credit line increased from $500 million to $600 million providing ample borrowing headroom nearing $200 million availability post borrowings [$398m drawn] which underscores confidence in financing adequacy for operations [S13,S28].

Dividend policy remains consistent with yields modest but progressive—dividends paid rose by nearly a quarter year-over-year topping $32.6 million in FY25—and buyback activity resumed at ~$30 million after larger-scale repurchases in prior years ($100m+ in FY24), signaling shareholder return focus balanced against liquidity needs during earnings pressure periods [F1,S27].

Return on equity approximate calculation places ROE near mid-teens (~12%)—reflective of solid profitability despite EBITDA pressure—while free cash flow constraints highlight need for ongoing margin recovery and working capital improvements.

Workforce Dynamics and Talent Management

Growing headcount from ~3,666 employees two years ago to almost 5,900 indicates scale-up following BASX acquisition integration plus organic expansion driven by demand growth requiring skilled labor capacity primarily localized across Tulsa (corporate HQ), Redmond Oregon (BASX control tech), Longview Texas (coil production) facilities among others [S20].

Competitive compensation packages with extensive benefits including aggressive employer match plans for health savings accounts/401(k), profit-sharing bonuses, tuition assistance programs along with paid parental leave etc., illustrate commitment toward talent attraction/retention amidst tight labor markets.

Outlook Considerations and What To Watch For (Analysis)

While explicit financial guidance was not issued contemporaneously with the recent earnings release [N13], future growth drivers revolve around:

- Successful conversion of backlog into revenues without significant order cancellations.

- Continued innovation progress especially addressing evolving refrigerant requirements while holding unit production costs stable.

- Mitigation effectiveness concerning raw material price swings; prudent inventory management reducing excess carrying costs.

- Expansion or defense of share within both replacement markets benefiting from lifecycle value narratives versus new builds where pricing sensitivity endures.

- Ability to manage operational risks related to cyber systems upgrade completion timeliness.

- Ongoing execution on sustainability goals potentially unlocking incentives or customer preference benefits.

- Navigating regulatory heterogeneity especially across states imposing divergent timelines/certifications impacting product design modularity/costs.

Monitoring quarterly updates on backlog status changes/billing milestones alignment will be key indicators signaling health of near-term revenue recognition prospects. Additionally scrutiny toward gross margin trends combined with cash generation metrics will illuminate whether expansionary pressures on input costs can be sufficiently offset by operational efficiencies or pricing adjustments.

Disclaimer

This analysis is prepared for informational purposes without providing investment advice or recommendations. It synthesizes disclosures filed by AAON Inc., third-party news articles referenced herein, and industry context as of the latest reporting dates available without speculative forecasting beyond documented data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments