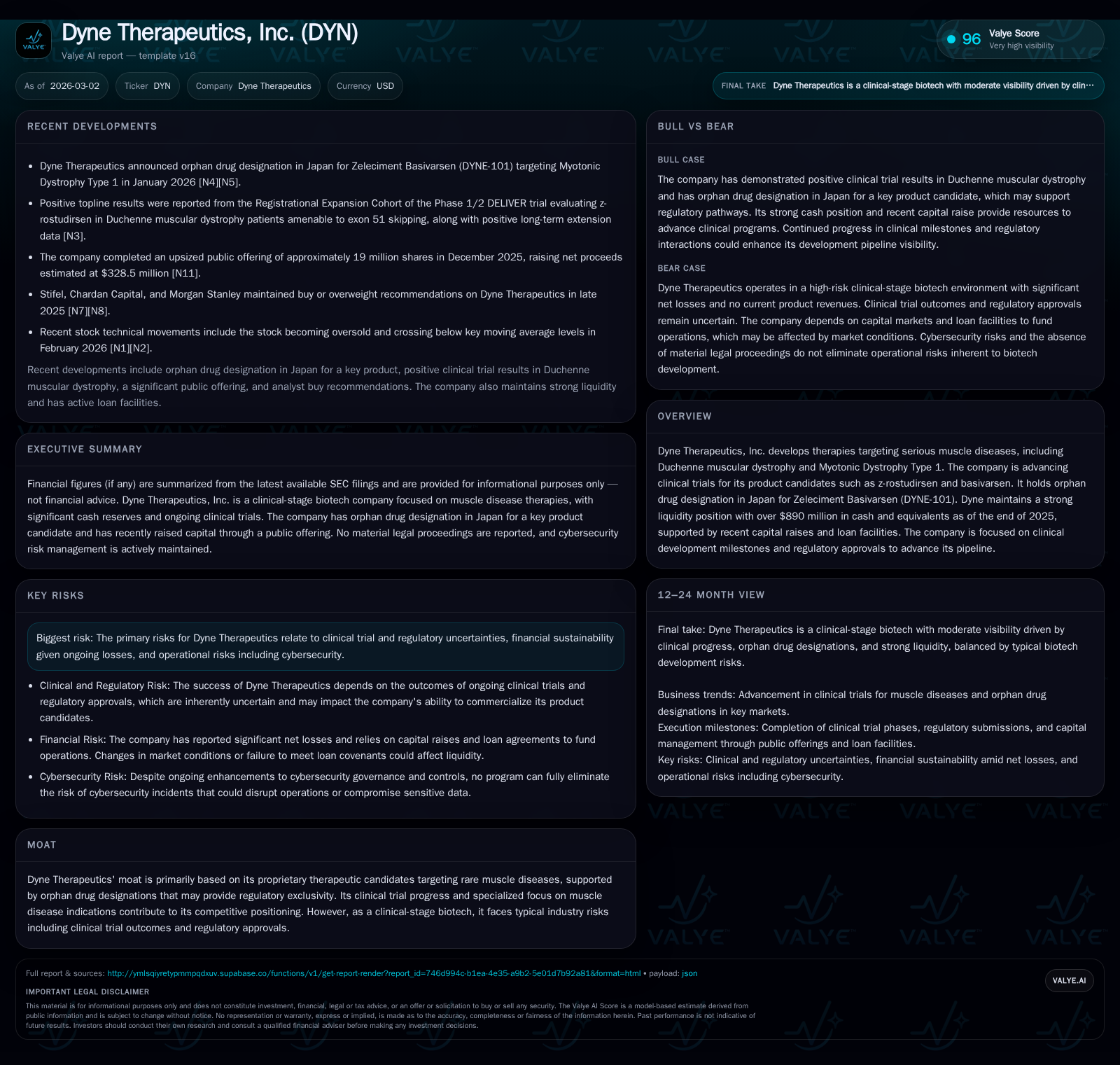

Dyne Therapeutics Charts Clinical Progress Against Muscular Dystrophy’s Financial Drag

Dyne Therapeutics advances its muscle disease pipeline through costly clinical programs, sustained by strong liquidity and orphan drug exclusivity.

Dyne Therapeutics, Inc. pursues specialized therapies for rare muscle diseases with key candidates like z-rostudirsen and basivarsen progressing through pivotal trials. Despite increasingly steep operating losses driven by intensive research and development, Dyne leverages orphan drug designation in Japan to establish regulatory exclusivity that could enhance commercialization prospects. The company maintains a robust cash position exceeding $890 million, supported by recent equity offerings and a structured loan facility, extending its runway into early 2028. Investors should monitor upcoming Phase 3 trial initiations and potential FDA Priority Review decisions as critical inflection points amid clinical and financial risks inherent to clinical-stage biotechs.

Clinical Development Journey and Historical Operating Trends

Since FY2022, Dyne Therapeutics has markedly escalated its investment into advancing clinical trials for rare muscle disease therapies such as z-rostudirsen (DYNE-251) intended for Duchenne muscular dystrophy (DMD) patients amenable to exon skipping, alongside basivarsen targeting Myotonic Dystrophy Type 1. This strategic focus is mirrored by rapidly increasing operating losses over four consecutive fiscal years: from -$171 million in FY2022 to nearly -$468 million by FY2025 — an increase of roughly 174% over the period [F1]. Net income declines have been comparable with FY2025 losses reaching -$446 million.

Operating cash flow trends evidence similarly pronounced negative shifts caused primarily by elevated R&D expenses typical of clinical-stage biotech companies heavily invested in late-phase development without current product revenues. Capital expenditure has remained comparatively low (around $1.9 million in FY2025), underscoring that Dyne's financial outflow is dominated by operational spending rather than tangible asset investments [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -446 | -403 | -468 | 2 | -40.6% |

| 2024 | -317 | -292 | -344 | 2 | -34.5% |

| 2023 | -236 | -188 | -242 | 1 | -40.4% |

| 2022 | -168 | -154 | -171 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -405 | -45.9 |

| 2024 | -295 | -50.4 |

| 2023 | -189 | -258.4 |

| 2022 | -157 | -66.6 |

Source: SEC companyfacts cache [F1].

Loss escalation parallels systematic scaling of clinical programs and deepening trial phases but underscores the financial drag characteristic of market entry gambits in orphan disease areas.

Leveraging Orphan Drug Designations: Competitive Edge and Regulatory Timing

A critical strategic advantage comes from Dyne's orphan drug designation granted for Zeleciment Basivarsen (DYNE-101) in Japan announced January 20, 2026 [N4][N5][S1]. Orphan status confers regulatory exclusivity measures that restrain competition through market protections such as reduced generic entrance possibilities and expedited regulatory interactions.

This exclusivity can enhance commercial viability by enabling premium pricing frameworks often necessary to recoup R&D investments for rare disorders characterized by small patient populations.

Zeleciment Basivarsen's target indication—Myotonic Dystrophy Type 1—is among muscle diseases with significant unmet medical need, thereby reinforcing Dyne's differentiation within biotech portfolios concentrated on neuromuscular therapies.

Near-Term Growth Catalysts and Pipeline Milestones

Looking forward, Dyne is poised to initiate a global Phase 3 clinical trial of z-rostudirsen in the second quarter of 2026 according to disclosures [S28]. This trial represents a pivotal inflection point to support broad regulatory filings globally.

Management anticipates potential U.S. Food and Drug Administration (FDA) Priority Review for z-rostudirsen’s Biologics License Application (BLA) allowing for accelerated review timelines targeted toward an early 2027 launch if approval is granted on schedule [N1][S28].

Investors should closely monitor interim data readouts from ongoing trials including open-label extensions that contribute evidentiary weight for efficacy and safety profiles.

Importantly, delays or unfavorable outcomes at these milestones could materially affect Dyne's valuation pathway given its dependence on successful late-stage transitions from investigational candidates to approved therapies.

Capital Structure, Cash Runway, and Debt Facilities

At fiscal year-end December 31, 2025, Dyne maintained a strong liquidity position with cash, equivalents, and marketable securities totaling approximately $893 million [F1], bolstered notably by proceeds from a December 2025 public offering which raised around $328 million net after underwriting expenses [S10][S18].

Further supporting liquidity is an amended Loan and Security Agreement with Hercules Capital dated December 8, 2025 [S6][S8][S9], under which Dyne drew a second term loan tranche of $50 million.

Key loan terms include:

- Floating interest rate tied to Wall Street Journal prime rate subject to a floor at 7.50%, plus margin of 2.45% annually;

- Interest-only payments scheduled until July 2030 with potential extensions contingent on milestone achievements;

- First-priority security interests covering substantially all company assets including intellectual property.

This multi-tranche financing structure offers Dyne optionality with up to approximately $125 million more available upon achievement of specified clinical and commercial milestones further extending operational runway into early calendar year 2028 [S9][S10][S26].

Such financial flexibility is pivotal given the high burn rates inherent in advancing orphan drug pipelines prior to commercial revenue generation.

Assessing Returns Amid Continued Losses — ROE and Cash Flow Dynamics

Despite substantial equity injections elevating shareholders' equity to roughly $972 million by the end of FY2025, Dyne reports approximate negative return on equity near -45.9%, symptomatic of net losses exceeding $446 million during the same period [F1].

Free cash flow remains negative at about -$405 million when subtracting capital expenditures from operating cash flows underscoring ongoing reliance on external capital infusions to fund operations given absence of product revenue streams [F1].

While operating within typical biotech developmental norms where near-term profitability is undelivered pending regulatory success and commercialization, such negative returns emphasize the imperative for disciplined capital allocation efficiencies.

Potential positive catalysts tied to pipeline advancement could alleviate pressure if resulting approvals enable patient access generating revenue flows.

Risk Factors: Trial Uncertainty, Regulatory Hurdles, and Operational Safeguards

Primary risk vectors confronting Dyne revolve around uncertain clinical outcomes as trial progressions can yield unexpected safety or efficacy results potentially halting program advancement or altering regulatory perspectives [S5][S7][S25][S28].

Given the substantial operating deficit load compounded with debt servicing commitments under credit facilities, maintaining financial sustainability over high burn phases remains challenging especially if approval timelines extend beyond projections or additional funding requirements materialize unexpectedly [S6][S12].

Operational risks also encompass cybersecurity vulnerabilities prompting implementation of evolving control frameworks aimed at governance enhancement including third-party risk management amid sophisticated threat landscapes—though no program can fully eliminate exposure risks as acknowledged openly by management [S1][S7].

Reputational risks linked with trial disappointments or regulatory setbacks carry ancillary commercial repercussions potentially impacting stakeholder confidence.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding any securities mentioned.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments