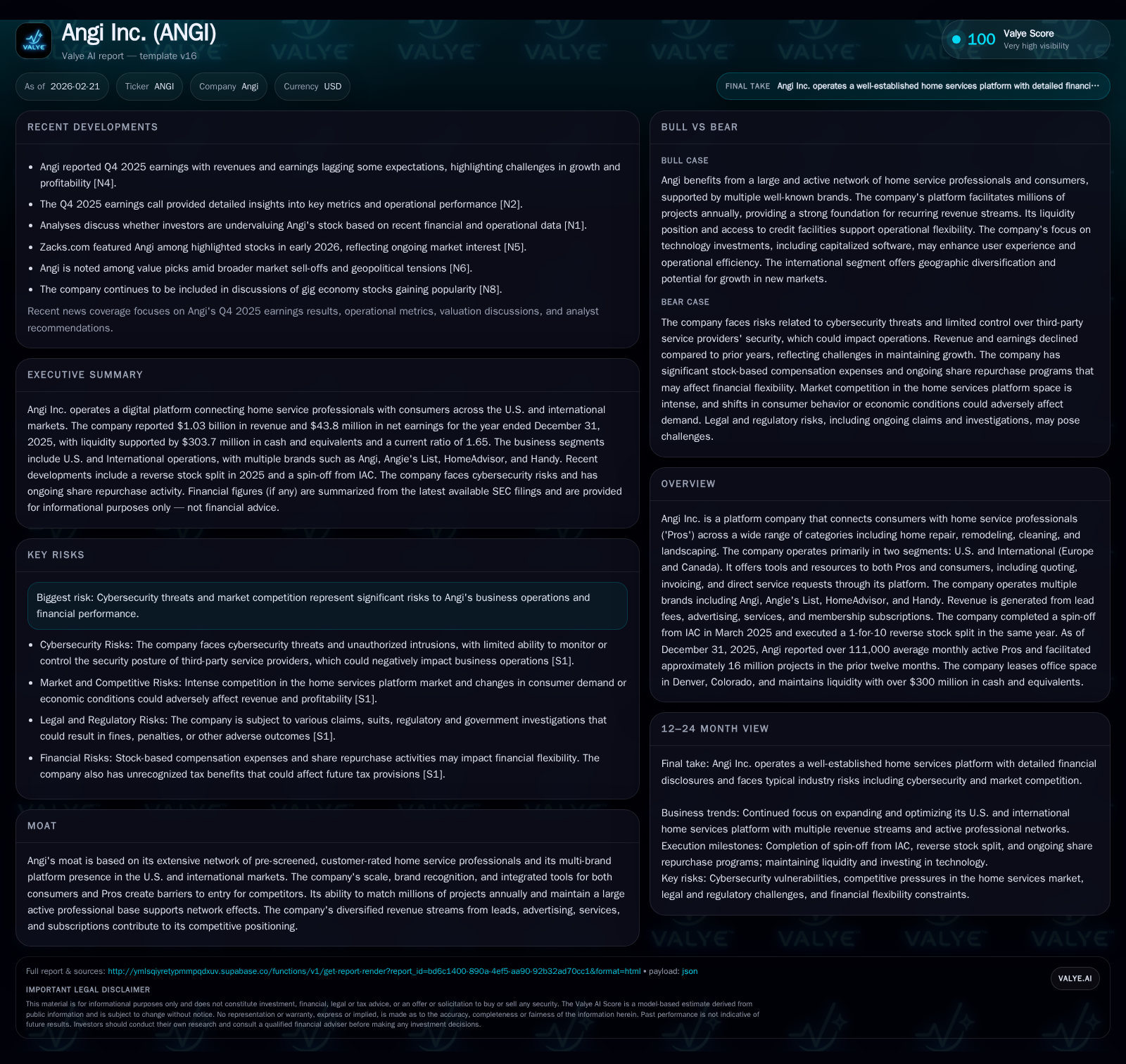

Angi Inc. Aligns Growth and Capital Allocation Amid Spin-Off Transition and Market Pressures

Post-spin-off operational restructuring and capital deployment shape Angi's growth trajectory in the evolving home services marketplace.

Angi Inc., a multi-brand platform connecting consumers with home service professionals, experienced a notable rebound in operating income and net profit in FY2025 following its March 2025 spin-off from IAC. The company's revenue declined year-over-year as it restructured and adjusted its business model, particularly within its U.S. segment, while maintaining solid international contributions. Despite generating positive operating cash flow, capital expenditures and sizable share repurchases exerted pressure on free cash flow. Angi’s competitive moat hinges on its extensive network of pre-screened pros and integrated consumer tools, but cybersecurity risks and competitive dynamics remain challenges to watch. Its capital strategy prioritizes aggressive buybacks over dividends amid ample liquidity and manageable debt.

Company Overview and Spin-Off Context

Angi Inc., formerly part of IAC Inc., officially separated through a spin-off in March 2025, making it an independent publicly traded company (ticker: ANGI) [S1][S5]. In conjunction with the spin-off, Angi implemented a 1-for-10 reverse stock split to concentrate its equity base [S7]. The company operates a multi-brand digital marketplace that connects consumers with home service professionals (“Pros”) across over 500 categories including repair, remodeling, landscaping, and cleaning services primarily in the U.S., Canada, and Europe [S6][N1]. Its recognized brands include Angi, Angie’s List, HomeAdvisor, and Handy.

Historical Performance & Drivers

Angi's reconstructed segment reporting emphasizes two segments: U.S. (Dominant market) and International (Canada plus key European markets) [S6][S9]. The company's performance recovered notably from losses in earlier years — the company reported an operating loss exceeding $26 million in FY2023 but reversed to positive $21.9 million in FY2024 [F1]. FY2025 marked continued operational improvement with operating income surging nearly 199% YoY to $65.4 million driven by substantial cost rationalizations including workforce reductions (~350 employees), reduced depreciation from lowered capital spend, and increased operating efficiency [S22][S23].

However, this came despite declining revenue which fell about 13% YoY from $1.19 billion in FY2024 down to approximately $1.03 billion for FY2025 [F1][S24]. The contraction largely stemmed from decreased lead generation revenues (-3% U.S. leads portion YoY), reduced advertising fees (-31% YoY in U.S.), falling service revenues (-22% U.S.), and falling membership subscriptions (-32% U.S.) [S24]. International revenues showed resilience holding near $126 million for FY2025 providing some geographic diversification [F1][S24].

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 44 | 65 | 60 | +19.0% |

| 2024 | 37 | 22 | 50 | +191.4% |

| 2023 | -40 | -26 | 48 | |

| 2022 | -126 | 116 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, CFO, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 149 | |

| 2024 | 29 | 3.5 |

| 2023 | 11 | -3.9 |

| 2022 | 8 |

Source: SEC companyfacts cache [F1].

- CFO available only for latest year based on MD&A disclosures [S16][F1]

Note: Operating Cash Flow (CFO) for prior years is not fully available from companyfacts; latest CFO of $105M plus capex indicators suggest negative free cash flow for FY25 [F1].

Future Growth Prospects

Despite the near-term revenue decline caused by market adjustments and the Company's decision to realign business models (such as migrating Canadian operations onto the European platform), Angi maintains growth levers from:

- A large active professional base exceeding 111,000 average monthly active Pros as of Q4’25 supporting sustained network effects [N1][N2].

- Massive scale matching approximately 16 million home service projects annually enabling a rich data-driven marketplace ecosystem [N1][S6].

- Expanding subscription offerings targeted at homeservice professionals coupled with advertising opportunities.

- Geographic expansion via international marketplaces in Austria, France, Germany, Italy, Netherlands, UK benefiting from cross-border technology leverage [S6][N3].

Nonetheless, growth headwinds include stiff competition from both national platforms and local niche players that could limit market share gains or pricing power [S27]. Ongoing cybersecurity threats pose risk to customer trust and regulatory compliance given sensitive payment data involved in transactions [S1][S27].

Forecasts & Upcoming Milestones

Angi has not provided explicit forward financial guidance yet but highlights several points requiring investor attention:

- Monitoring shifts in consumer preferences away from lead-based models toward subscription or bundled services.

- Effectiveness of recent restructuring initiatives on margin expansion.

- Execution progress on syncing international brands onto unified technology backbones.

- Capital expenditure plans anticipating a moderate reduction of roughly 5-10% below the $59.6 million spent in FY2025 focused mainly on capitalized software development efforts [S26][S28].

- Managing potential impacts of macroeconomic factors such as housing market fluctuations on home improvement demand.

Returns & Capital Allocation

Return metrics illustrate modest profitability: estimated ROE based on FY2025 net income ($43.8 million) over equity ($1.06 billion at FY2024 end) approximates a low single-digit return near 4.1%, signaling room for improved capital efficiency [F1].

Capital allocation sharply prioritized shareholder returns via buybacks totaling nearly $149 million in FY2025 — representing a significant increase over prior years — which exhausted all share repurchase authorizations granted during that period as of December-end [S10][F1]. No dividend distributions are planned currently reflecting management’s choice to deploy excess cash into reducing outstanding shares rather than pay dividends while maintaining liquidity reserves exceeding $300 million combined cash/cash equivalents at year-end [F1][S20].

Capex investments focused mainly on internal-use software capitalization amounted to nearly $60 million reflecting strategic product initiatives aimed at enhancing user experience and operational scalability though management signals slightly lower levels anticipated going forward owing partly to project completion phases [S26][S28].

Balance sheet liquidity remains sound with no borrowings drawn against the recently established $175 million senior secured revolving credit facility as of end-2025 and manageable long-term debt carrying just under $500 million principal outstanding at favorable fixed interest rates (3.875%) maturing mid-2028 [S4][F1]. Operating cash flow notably improved posting over $105 million compared to previous periods supporting working capital needs despite elevated capex spend [F1][S16].

Competitive Moat & Industry Dynamics

Angi’s strength lies chiefly in its expansive platform ecosystem connecting hundreds of thousands of vetted service Pros with consumers across numerous home improvement categories supported by well-known brand names (Angi, Angie’s List, HomeAdvisor, Handy). This scale engenders network effects that competitors find difficult to replicate quickly without considerable upfront investment in marketing, technology integration, and professional screening processes . Integrated quoting tools, invoicing systems and direct booking capabilities create customer stickiness benefiting both consumer convenience and professional engagement.

The home services category continues trending toward digital marketplace consolidation driven by consumer preferences for trustworthy vetted vendors coupled with ease of online transaction execution versus traditional offline sourcing methods.

Nevertheless heightened cybersecurity risks related to third-party infrastructure dependencies remain pivotal concerns with potential reputational impacts should breaches occur [S1]. Competitors ranging from other technology-enabled platforms to traditional referral networks continue vying aggressively for market share putting pressure on pricing dynamics across segments.

Risks & Legal Environment

The company faces persistent cybersecurity threats as detailed by recurring unauthorized system intrusions impacting business continuity risk mitigation efforts around critical infrastructure shared with suppliers/vendors remains imperfect despite ongoing governance protocols [S1]. Additional legal exposures include routine claims across intellectual property disputes, privacy regulations especially GDPR compliance given international footprint alongside labor/employment litigations common within gig-enabled workforces; however current matters are not deemed individually material financially but could aggregate adversely if unresolved swiftly [S27]. Macroeconomic uncertainty including inflationary pressures affecting household discretionary spending may translate into fluctuating project volumes.

Conclusion & Monitoring Checklist (Analysis)

Going forward observers should monitor:

- Trajectory of domestic versus international segment revenues especially recovery or stabilization trends post restructuring moves.

- Effectiveness of ongoing margin improvement plans including cost control beyond one-time headcount reductions.

- Platform engagement metrics such as monthly active Pros counting and project volume matched.

- Share repurchase pacing relative to market price volatility or potential resumption of dividend policy.

- Developments concerning cybersecurity framework enhancements or any incidents reported.

- Management commentary on macroeconomic impact scenarios affecting consumer demand patterns.

While recent profit improvements are encouraging after years of losses, revenue contraction implies growth constraints ahead that Angi must strategically address using its scale advantages and new product/service innovation within increasingly competitive environment typical for mature tech-enabled marketplaces supporting fragmented home services industry segments.

This report is based on publicly available filings and news reports as of February 21, 2026. It is provided solely for informational purposes without recommendation or solicitation related to any securities or investment strategies related thereto.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments