FormFactor Inc's Custom Semiconductor Testing Technologies and Capital Strategy in 2025

Examining FormFactor’s tailored probe card innovations, customer concentration risks, and capital deployment amidst semiconductor industry shifts.

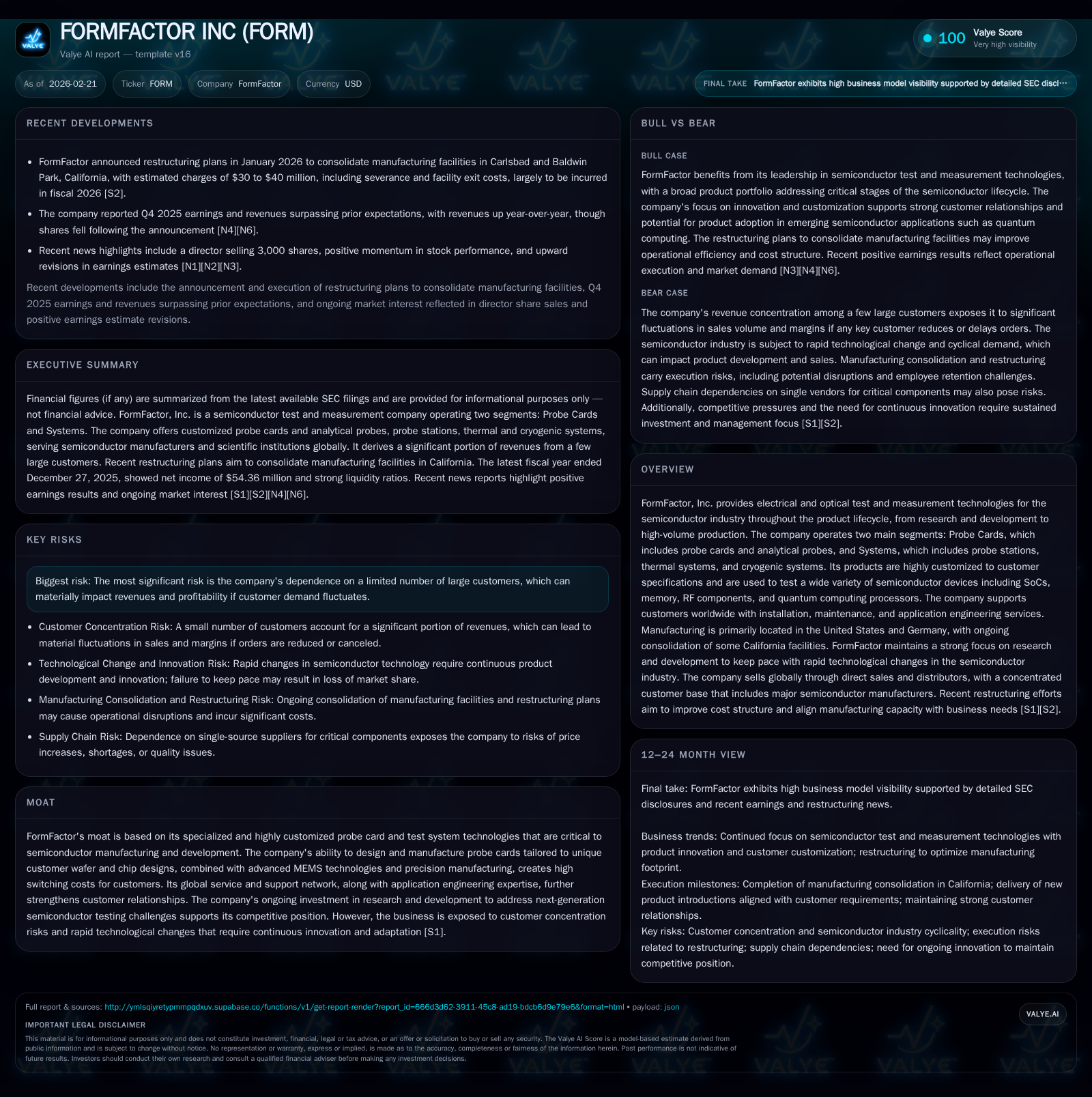

FormFactor Inc operates at the critical juncture of semiconductor testing with highly customized probe cards and systems that cater to an evolving semiconductor landscape. While the company’s operating income and net income declined in 2025, strong operating cash flow and significant capital investments highlight a strategic focus on capacity expansion and innovation. Customer concentration remains a key risk factor, with top clients accounting for a substantial portion of revenues. The absence of dividends but continued share repurchases at moderated levels underscores management’s emphasis on reinvestment to sustain technological leadership and support growth in emerging segments like quantum computing.

Custom Solutions Fueling Historical Growth and Revenue Dynamics

FormFactor's business model centers on crafting bespoke probe cards and intricate test systems critical to semiconductor device validation across R&D to fabrication stages. Their specialized Probe Cards segment comprises sophisticated micro-electromechanical systems (MEMS)-based contact elements tailored to customer wafer designs, accommodating diverse chip layouts including SoCs, memory modules, RF components, and emerging quantum processors [S10]. This customization enables FormFactor to capture the nuanced requirements of leading semiconductor makers.

Financial data from the latest fiscal year shows FormFactor posted operating income of $57.1 million in 2025, down 11.9% year-over-year from $64.8 million in 2024 despite ongoing revenue generation. Net income similarly contracted by 21.9%, reflecting margin pressures that may be linked to increased fixed costs or shifts in product mix [F1]. Notably, revenue data beyond 2017 is not available from provided tags; thus, analysis focuses primarily on profitability and cash flow metrics.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 54 | 115 | 57 | 104 | -21.9% |

| 2024 | 70 | 118 | 65 | 38 | -15.5% |

| 2023 | 82 | 65 | 83 | 56 | +62.4% |

| 2022 | 51 | 132 | 55 | 65 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 26 | 12 | 5.3 |

| 2024 | 53 | 79 | 7.3 |

| 2023 | 20 | 9 | 9.1 |

| 2022 | 82 | 67 | 6.3 |

Source: SEC companyfacts cache [F1].

Note: Revenues are not available from provided tags; financial analysis emphasizes profitability and cash flow.

Customer Concentration: Double-Edged Sword for Revenue Stability

A defining characteristic of FormFactor’s revenue profile is the concentration among a limited number of major customers—one accounted for approximately 22.9% of total revenues in fiscal year 2025; historically, the top two customers combined contributed over one-third of total revenues [S4][S5]. Leading clients include SK hynix Inc., Intel Corporation, Taiwan Semiconductor Manufacturing Company Ltd., and Samsung Electronics among others [S5]. This composition is influenced by ongoing semiconductor industry consolidation trends which inherently raise concentration risk.

Such dependence exposes FormFactor to sharp quarterly fluctuations in sales volumes and margins tied directly to individual customer order timing and capital expenditure cycles [S7]. Reductions or delays by these key accounts can result in excess inventory write-downs or impaired fixed-cost leverage given the bespoke nature of probe card manufacturing customized for distinct chip designs [S7][S14]. Furthermore, geopolitical events or regional economic shifts affecting these customers could indirectly impair demand for FormFactor’s products.

Technology Investments and Research & Development as a Growth Lever

FormFactor maintains a strong commitment to R&D as a cornerstone for competitive advantage amid fast-paced technological advancements within the semiconductor lifecycle testing domain [S1]. Core innovations focus on MEMS integration in probe cards allowing ultra-fine contact points with high precision force controls across complex wafer surfaces—a capability imperative for modern SoC test procedures requiring high pin counts with minimal signal degradation [S10].

Additionally, the company has developed vertically integrated thermal systems combining its probe stations with thermal management solutions enabling precise environmental conditions—from ambient through cryogenic temperatures—to optimize semiconductor test accuracy [S6][S10]. Notably, their cryogenic systems support quantum computing processor testing at near-absolute zero temperatures, positioning FormFactor at the frontier of emerging semiconductor segments requiring advanced instrumentation.

These R&D initiatives entail substantial investment but secure differentiated product offerings that competitors find difficult to replicate rapidly given high entry barriers including technical sophistication and customer qualification complexities [S1][S24].

Impact of Semiconductor Industry Trends on Future Demand Prospects

Recent earnings commentary highlights continuing demand drivers from foundry & logic device manufacturers alongside memory producers such as DRAM leaders—segments traditionally served through high-volume probe card sales [N2][N3][S4]. However, cyclicality of semiconductor capital expenditure programs combined with geopolitical tensions inject variability into near-term order patterns.

Consolidation among Fabless foundries and Integrated Device Manufacturers amplifies customer concentration risks but also opens potential scale opportunities if contract expansions materialize [S4][N3]. Concurrently, evolving test methodologies incorporating AI accelerator chips or more complex heterogeneous integrations could spur requirements for next-gen testing architectures where FormFactor aims to leverage its R&D pipeline.

The ongoing build-out of new manufacturing capacity such as the Texas facility expected online in late fiscal '26 reflects strategic alignment with increasing fab automation trends but contributes upfront capital intensity [S12][N4]. Longer-term prospects will require monitoring how emerging segmentations like quantum computing wafer test volumes evolve relative to broader foundry spending.

Detailed Review of Profitability and Cash Flow in Fiscal Year 2025

In fiscal year 2025, FormFactor’s operating income decreased by approximately 11.9% to $57 million while net income fell nearly 22%, indicating margin compression pressures potentially from higher operating costs or unfavorable sales mix shifts [F1]. Despite this profit contraction, operating cash flow remained strong at $115 million albeit slightly down (-1.8%) year-over-year signaling resilient core cash generation capacity.

Capital expenditures surged by nearly +170% reaching $104 million primarily driven by investments in new manufacturing infrastructure expansions and consolidation projects from California sites into newer facilities including one in Texas [F1][S12]. This surge led free cash flow—the residual after capex—to shrink materially with estimated FCF around $11.7 million.

Liquidity appears solid with a current ratio near 4.5x reflecting considerable liquidity buffers via cash equivalents exceeding $103 million at year-end [F1][S17]. Shareholders' equity expanded moderately amid retained earnings accumulation despite lower profitability levels.

Capital Allocation Priorities: Share Buybacks and Investment Intensity

FormFactor’s capital deployment strategy evidences prioritization of reinvestment over direct shareholder yield as no dividends have been declared per available data [F1][S26]. Share repurchase activity continued into fiscal year ’25 but decelerated notably from prior years—$26 million spent versus $53 million in ’24—reflecting prudent balancing against elevated CAPEX commitments.

This calibrated buyback approach underscores management’s focus on fostering operational scalability while maintaining flexibility for ongoing R&D funding critical for sustaining technological differentiation [S23][S26]. Capital redeployment efficiency remains a key metric given competing uses between internal innovation pipeline expenditures versus returning excess cash to shareholders via buybacks.

Key Milestones to Watch: Innovation Pipeline and Customer Diversification

Analyst commentary from recent earnings calls highlights anticipation around several next-generation probe technologies purportedly aimed at improving throughput for AI accelerators and novel multi-technology wafers requiring integrated optical-electrical testing platforms [N4][N5]. Monitoring progress towards commercialization milestones on these fronts will provide insights into sustainability of growth beyond traditional probes servicing established SoC or memory segments.

Equally important is diversification within the customer base as market consolidation enhances exposure risk concentrated among a few large accounts responsible for roughly one-third or more of revenues [S4][N5]. Watchpoints include disclosures regarding order book breadth expansions or new significant contract wins outside core legacy customers.

While no formal guidance currently offers explicit future forecasts within filings or news transcripts, sector-watchers should focus on quarterly cadence changes in revenue mix alongside R&D spend efficiency metrics as proxies for innovation adoption curves.

Risks Surrounding Customer Dependence and Product Customization Costs

The bespoke nature of FormFactor’s probe cards entails significant fixed cost structures coupled with customization expenses specific to each wafer design iteration which are generally non-recoverable upon order cancellations or deferrals—increasing gross margin volatility potential notably when faced with abrupt demand contractions [S7][S14]. The company explicitly flags exposure to impairment risks related to inventory write-downs reflecting these unique manufacturing challenges.

Given only limited customers contribute disproportionately large revenue shares (one single client near ~23% FY25), any weakening financial stability among such clients or disruptions caused by external factors like geopolitical trade restrictions could materially depress orders or delay payments impacting working capital needs [S7][S14].

Industry competition intensifies further risk dynamics as rival probe card vendors—including Japan Electronic Materials Corporation or Technoprobe—possess capabilities in MEMS technologies necessitating persistent innovation efforts by FormFactor lest market share erosion ensue [S24][S27]. The balance between maintaining technological edge versus cost containment represents an ongoing strategic challenge.

Disclaimer: This report is prepared for informational purposes based on publicly available data as of February 21, 2026, including SEC filings and news sources cited herein; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments