LPL Financial’s $2.7B Commonwealth Acquisition Underpins Record Revenue but Pressures Cash Flows

LPL Financial’s scale and integrated platform fuel growth, while acquisition-related costs and regulatory risks shape near-term dynamics.

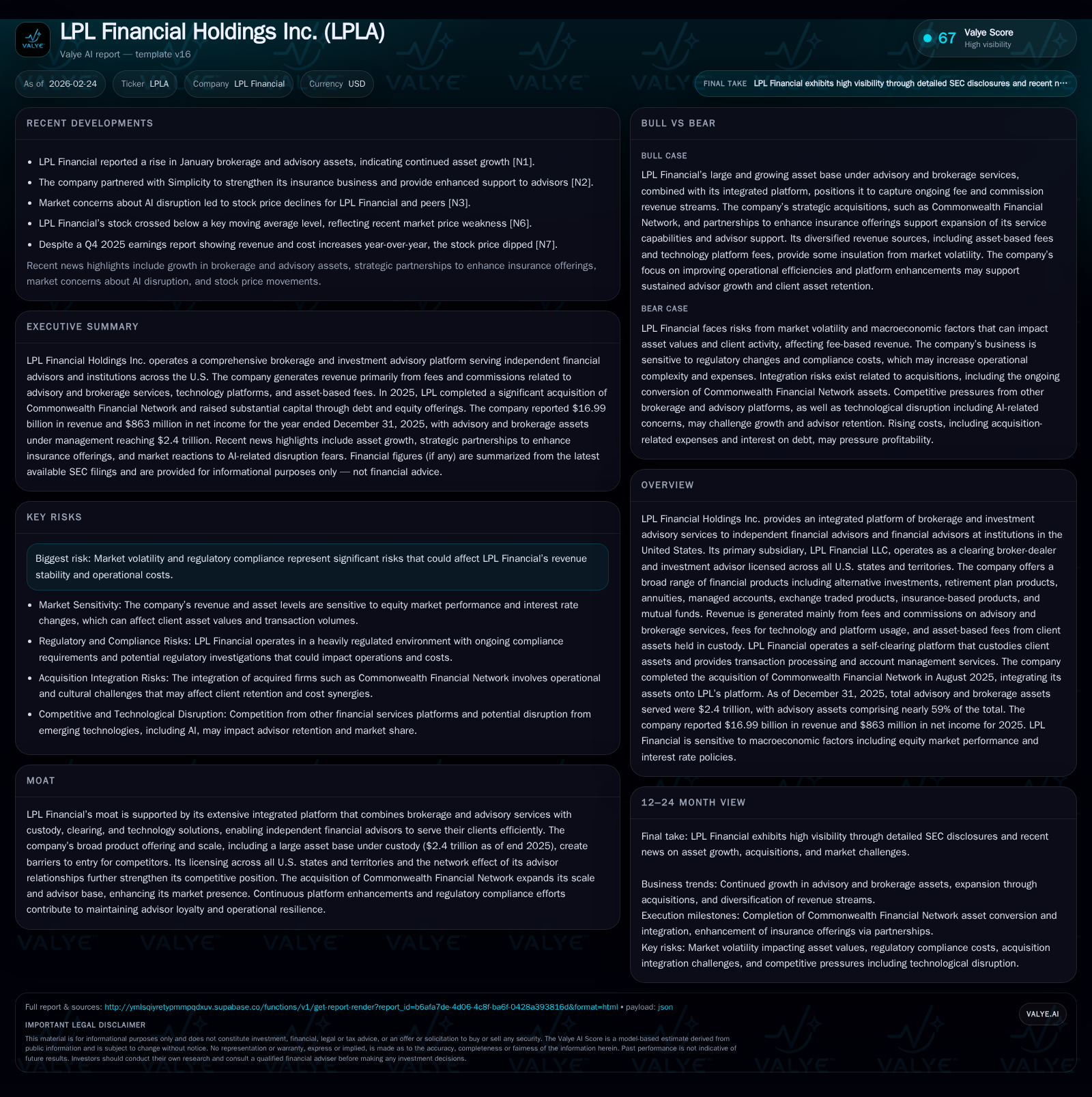

LPL Financial Holdings Inc. demonstrated robust revenue growth in 2025, driven by strong advisory services expansion and the transformative acquisition of Commonwealth Financial Network. Despite a 37% revenue jump to nearly $17 billion, the company faced an 18.5% net income decline and a significant operating cash flow contraction, reflecting elevated expenses related to integration, borrowing costs, and regulatory compliance. LPL's balance sheet strengthened substantially with equity rising to $5.3 billion due to equity issuance for Commonwealth funding, supporting ongoing investments and debt management. Going forward, execution on platform integration, regulatory environment navigation, and advisor asset growth will be critical to restoring cash flow stability and sustaining returns.

Company Overview

LPL Financial Holdings Inc., through its primary subsidiary LPL Financial LLC, is a leading U.S.-based provider of brokerage and investment advisory services targeting independent financial advisors and institutionally affiliated advisors. The self-clearing platform supports custody of client assets totaling approximately $2.4 trillion at the end of 2025, offering broad product breadth spanning alternative investments, retirement plans, annuities, managed accounts, ETFs, insurance products, mutual funds and more. Revenue streams are diversified across commissions on advisory/brokerage activities, asset-based fees on custody balances, technology platform fees charged to advisors, interest income from margin loans and cash balances, and transaction-related fees [S1].

The firm's moat largely stems from its integrated platform that combines clearing, custody, brokerage/advisory services with scale advantages amplified by licensing nationwide across all states plus territories. The network effect of its large independent advisor base — further expanded by the transformational acquisition of Commonwealth Financial Network for approximately $2.7 billion in August 2025 — positions LPL strongly within a fragmented industry undergoing concentration pressures [S1][N8].

Historical Performance (Past Growth Drivers)

LPL Financial has shown steady top-line growth over recent years with an acceleration in 2024-25 tied primarily to organic advisory revenue increases and inorganic expansion:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17.0 | 863 | -411 | 570 | +37.2% | -18.5% |

| 2024 | 12.4 | 1059 | 278 | 563 | +23.2% | -0.7% |

| 2023 | 10.1 | 1066 | 513 | 403 | +16.9% | +26.1% |

| 2022 | 8.6 | 846 | 1946 | 307 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 94 | 100 | -982 |

| 2024 | 90 | 170 | -285 |

| 2023 | 92 | 1100 | 109 |

| 2022 | 80 | 325 | 1639 |

Source: SEC companyfacts cache [F1].

*Latest fiscal year ended Dec-31-2025; all figures approximate per [F1]

The dramatic increase in revenue during FY25 reflects the first full impact of Commonwealth along with organic growth in advisory fees and technology/platform usage fees paid by an expanding advisor network [S1][N7]. However, net income declined sharply due mainly to elevated expenses in compensation (largely variable pay associated with asset performance), acquisition-related amortization of intangibles, higher interest costs on expanded debt levels following multiple senior note issuances starting mid-2024 into early-2025 totaling over $2 billion for acquisition funding [S6][S13], plus incremental integration spending.

Operating cash flow turned negative for the first time in this recent multi-year trend mostly due to working capital absorption attributable to acquisition timing effects (e.g., contingent consideration payments), elevated commission payouts tied directly to higher sales-based revenues paid out immediately versus reported on accrual basis for revenue recognition purposes, as well as growth-related investments into technology and service enhancements required for scaling advisor support capabilities [F1][N3][S13]. Capital expenditures stayed relatively flat year-over-year at roughly half a billion dollars annually as LPL prioritizes infrastructure modernization.

Future Growth Prospects

Revenue growth potential rests on several vectors:

- Advisor Base Expansion & Retention: Post-acquisition integration of Commonwealth’s approximately thousands of advisors onto LPL’s proprietary platform is underway with full transition expected by Q4 2026; successful migration without attrition critical for sustaining asset inflows [S1].

- Asset Under Custody (AUC) Growth: Continued growth in advisory & brokerage AUC driven both by market appreciation and new client asset accumulation through advisor networks; recent January brokerage/advisory asset rises signal momentum after volatile markets year-end [N7].

- Product Offering Innovation: Strategic partnership with Simplicity to enhance insurance product support evidences efforts to expand product penetration which typically garners higher fee capture rates per asset unit managed [N8].

- Platform Technology Adoption: Ongoing investments aimed at increasing automation efficiency while improving advisor tools can boost engagement metrics and lower operational risk exposure from manual workflows characteristic of wealth management custodians [S1].[Analysis: Technology infrastructure upgrades can also buffer against margin pressures common in the industry due to competition from robo-advisors and low-cost brokers].

Risks that could cap growth include market volatility impacting advisory AUM-linked fees; regulatory compliance resets prompting costly remediation measures (historically evident from SEC investigations); competitive pricing pressures especially amid fintech disruption fears seen broadly across broker-dealers including LPL’s peer Schwab [N6]; and operational complexities stemming from platform integrations.

Forecasts / Milestones / Expectations

Explicit guidance was not disclosed publicly post-Q4 results; however analyst focus should center around:

- Timing/details of Commonwealth full-platform transition completion slated around late-2026.

- Advisor retention rates during/after conversion process affecting recurring revenue stability.

- Incremental cost synergies realization vs integration expenses for merger-related goodwill amortization impacts.

- Regulatory resolutions or new rules impacting cash sweep programs or AML compliance governance frameworks.

- Quarterly updates on brokerage & advisory asset trends as proxy indicators for future recurring fee momentum.[Analysis: Market watch on expense containment success given recent sharp increase warranted due to operating loss impact on CFO]

Returns / Capital Allocation

Return on equity hovered around an estimated ~16% in FY25 (Net Income / Equity = $863m / $5.34b), down from mid-teens prior years due primarily to earnings dilution post-expansion combined with a substantially larger equity base following April equity issuance for deal funding.[F1] This dilution crosscuts net income given static dividends indicating return moderation

Dividend payout remained steady at roughly $0.30 quarterly per share amounting near $94 million total annually demonstrating commitment to shareholder yield despite earnings pressure.[F1][S15]

Buyback activity markedly slowed relative to previous years’ elevated repurchase levels (from over $1B in FY23 down to $100M FY25), reflecting temporary pause effects surrounding Commonwealth deal capital allocation priorities.[F1][S22] The company retains discretionary authority over timing pending capital needs constrained by credit covenants.[Analysis: Management likely prioritizing deleveraging flexibility or liquidity buffers versus aggressive buybacks short term]

Capital structure saw increasing debt leverage with aggregate corporate notes exceeding $7 billion after multiple fixed-rate senior unsecured bond issuances between mid-2024 through early-2025 at coupon rates ranging roughly from mid-4% up to near 6.75%, underpinning acquisition financing.[S6][S11] Revolving credit balances remained below maximum available lines but provide ample liquidity capacity mitigating refinancing risk risks ahead.

Industry Context & Operational Nuances

As an industry leader within the U.S independent wealth management channel—a sector historically resistant yet vulnerable to headwinds like AI-powered robo-advice platforms—LPL’s integrated clearing/custody/platform model remains an important competitive differentiator providing stickiness among advisors reliant on seamless operational workflows.

In-house clearing/custody reduces counterparty risk exposure often associated with third-party arrangements prevalent among smaller competitors while enabling economies of scale essential for funding continuous tech evolution accommodating real-time data flows and analytics responsiveness demanded by modern financial advisors.

Regulatory complexity presents persistent challenges given persistent SEC oversight coverage evidenced by past AML compliance investigations settled by monetary penalties (~$18m + earlier ~$50m fines); ongoing monitoring of regulation around electronic communications archiving policies underscores operational risk vigilance matters extensively highlighted within internal risk frameworks at LPL.[S5][S16][S18]

Conclusion

LPL Financial’s FY25 performance reflects a company scaling rapidly through transformative M&A activity balanced against strategic investments required for sustainable future growth amid complex regulatory constraints. Strong top-line increases underline successful expansion trajectory bolstered by integration of Commonwealth’s sizable advisor franchise, though near-term net earnings compression paired with negative cash flow trends highlight execution challenges common within large-scale integrations. Finally, prudent capital management focused on balancing leverage utilization against shareholder return disciplines will be pivotal as LPL seeks both operational resilience and competitive adaption within the evolving independent wealth management ecosystem.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations regarding any securities or companies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments