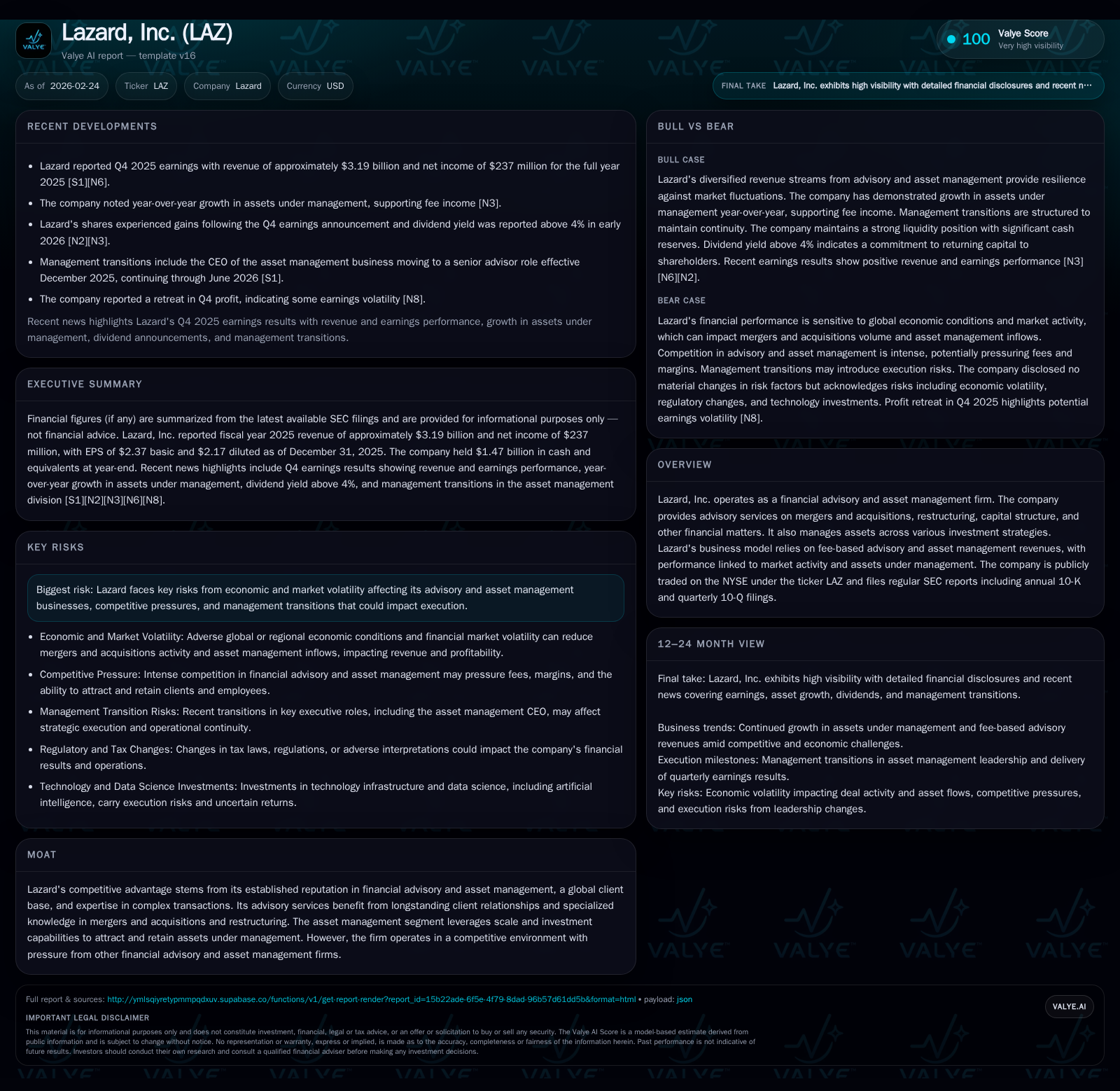

Lazard, Inc. Manages Transition Challenges While Stabilizing Fee-Based Revenue Growth

Lazard’s recent financials reflect modest revenue growth tempered by declining profitability amid leadership changes and market volatility.

Lazard, Inc. posted 1.5% revenue growth in 2025 driven primarily by steady asset management fees and advisory activity, but operating income and net income declined by about 15% year-over-year. Leadership transitions in key executive roles—most notably the CFO—signal ongoing efforts to stabilize operations. The firm’s asset management segment benefits from increased assets under management (AUM), yet market and economic uncertainties continue to pose headwinds. Capital returns remain consistent with dividend payments supported by cash flows, though share buybacks have slowed after a sizeable repurchase in 2022.

Company Overview and Historical Performance

Lazard, Inc. operates as a dual-focused financial advisory and asset management firm with global reach and a strong reputation for handling complex mergers and acquisitions (M&A), restructuring transactions, capital structure advice, alongside managing diverse investment strategies. The business model emphasizes fee generation from advisory mandates and asset management fees linked directly to AUM performance fluctuations.

In reviewing Lazard's financial history over the past four fiscal years ending December 31, there is a discernible pattern of volatile earnings near a revenue trough in 2023 followed by recovery:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3.2 | 237 | 519 | 328 | +1.5% | -15.4% |

| 2024 | 3.1 | 280 | 743 | 386 | +21.1% | +470.8% |

| 2023 | 2.6 | -75 | 165 | -80 | -9.2% | -121.1% |

| 2022 | 2.9 | 358 | 834 | 517 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 187 | 91 | 487 |

| 2024 | 179 | 60 | 697 |

| 2023 | 173 | 102 | 136 |

| 2022 | 182 | 692 | 784 |

Source: SEC companyfacts cache [F1].

Note: Some YoY figures for years with losses/negative operating income are omitted due to volatility.

Revenue peaked notably in prior years with strong expansion in advisory fees amid M&A booms but dipped during challenging market conditions in FY23 before rebounding modestly in FY24-25[F1]. Operating income swung dramatically from a loss in FY23 back to profitable territory though fell again in FY25 on margin pressures[F1]. Net income followed a similar pattern.

Operating cash flow exhibited sharp fluctuations impacted by working capital swings alongside earnings variability while capital expenditure remained conservative between $28–$50 million annually, consistent with service-based firms emphasizing human capital over fixed assets[F1].

Capital allocation shows a firm commitment to dividends alongside active buybacks which however moderated significantly after an elevated program especially seen in FY22 where repurchases spiked to nearly $700 million before tapering down sharply[F1]. This aligns with cautious capital deployment prevailing among elite advisers balancing regulatory scrutiny and shareholder return expectations.

Leadership Transitions Affecting Strategy Execution

Recent disclosures highlight key leadership transitions reflective of broader strategic recalibration within Lazard heading into the new fiscal year:

Tracy Farr assumed the CFO role effective February 2026, succeeding Mary Ann Betsch who shifted into a Senior Advisor position through June this year[S25][S26]. Farr brings substantial tenure from within the company’s Capital Structure Advisory team enhancing continuity amid operational challenges.

The asset management business underwent leadership refinement with Christopher Hogbin named Managing Director and CEO effective no later than January end-2026[S21][S27], following Evan Russo’s transition out of an executive role to senior advisorship phased through December last year[S21].

These changes indicate Lazard’s intent to strengthen financial stewardship while refreshing top-line growth leadership particularly within asset management where scale efficiencies and innovative strategies like AI integration are pivotal for competitive advantage[S12].

Growth Prospects and Sectional Outlook

Future growth is expected primarily from:

- Increased AUM benefiting from market appreciation and net inflows buoyed by specialized investment strategies[N2][N3].

- Continued demand for financial advisory services given persistent corporate restructuring needs amid geopolitical uncertainties and sectoral shifts[S4].

- Technology investments targeting artificial intelligence applications which may boost operational efficiency and client engagement as signaled in recent corporate messaging on Lazard’s "2030 vision" strategy[S15][S12].

Constraints arise due to:

- M&A market cyclicality directly impacting deal flow volumes thus fee generation.

- Competitive pressures from larger bulge bracket banks expanding advisory capabilities alongside boutique firms honing niche specialization.

- Macroeconomic risks including inflationary pressures that could slow client activity or reduce risk appetite[S4].

Lazard's established client relationships provide some moat against commoditization; however, execution risk remains non-trivial particularly while integrating new leaders across critical functions.

Financial Returns and Capital Allocation Dynamics

The approximate return on equity for FY25 stands robust around +27%, computed as net income over average shareholders' equity derived from year-end balances[F1]. This measures healthy profitability alignment albeit down from peak levels when revenue expansion was accelerating.

Free cash flow remains solid at about $487 million (operating cash flow less capex), underpinning sustainable dividend payouts totaling roughly $187 million—a trend maintained throughout recent years despite earning fluctuations[F1]. Buybacks restarted moderately after large reductions post-pandemic, suggesting prudent capital deployment aligned with market opportunities but calibrated for current earnings realities.[F1]

What To Watch Going Forward – Analysis Perspective

Although explicit long-term guidance is not available currently through official filings or press releases, critical indicators will include:

- Quarterly trends in AUM changes reflecting market positioning, investment performance, and net inflows/outflows impacting fee revenues.

- Advisory fee momentum tied closely to transaction volumes evidenced by announced deals or league table metrics.

- Operating margin recovery post-leadership transition demonstrating cost control efficiency amidst wage inflationary environments.

- Updates on technological investments yielding productivity enhancements particularly AI-assisted analytics favoring Lazard's differentiated offerings.

- Dividend sustainability versus evolving cash generation amidst broader economic conditions.

Overall, Lazard operates at the intersection of cyclical deal activity and structural asset gathering trends where sustained execution excellence will dictate stronger profit trajectories despite external headwinds.

Disclaimer: This analysis is informational only based on current publicly available SEC filings, news sources cited herein, and recognized industry dynamics as of early 2026 without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments