Park Hotels & Resorts Confronts Earnings Volatility and Heavy Capital Expenditures Amid Portfolio Renovations

The lodging REIT grapples with recent operating losses despite active asset management and balance sheet flexibility.

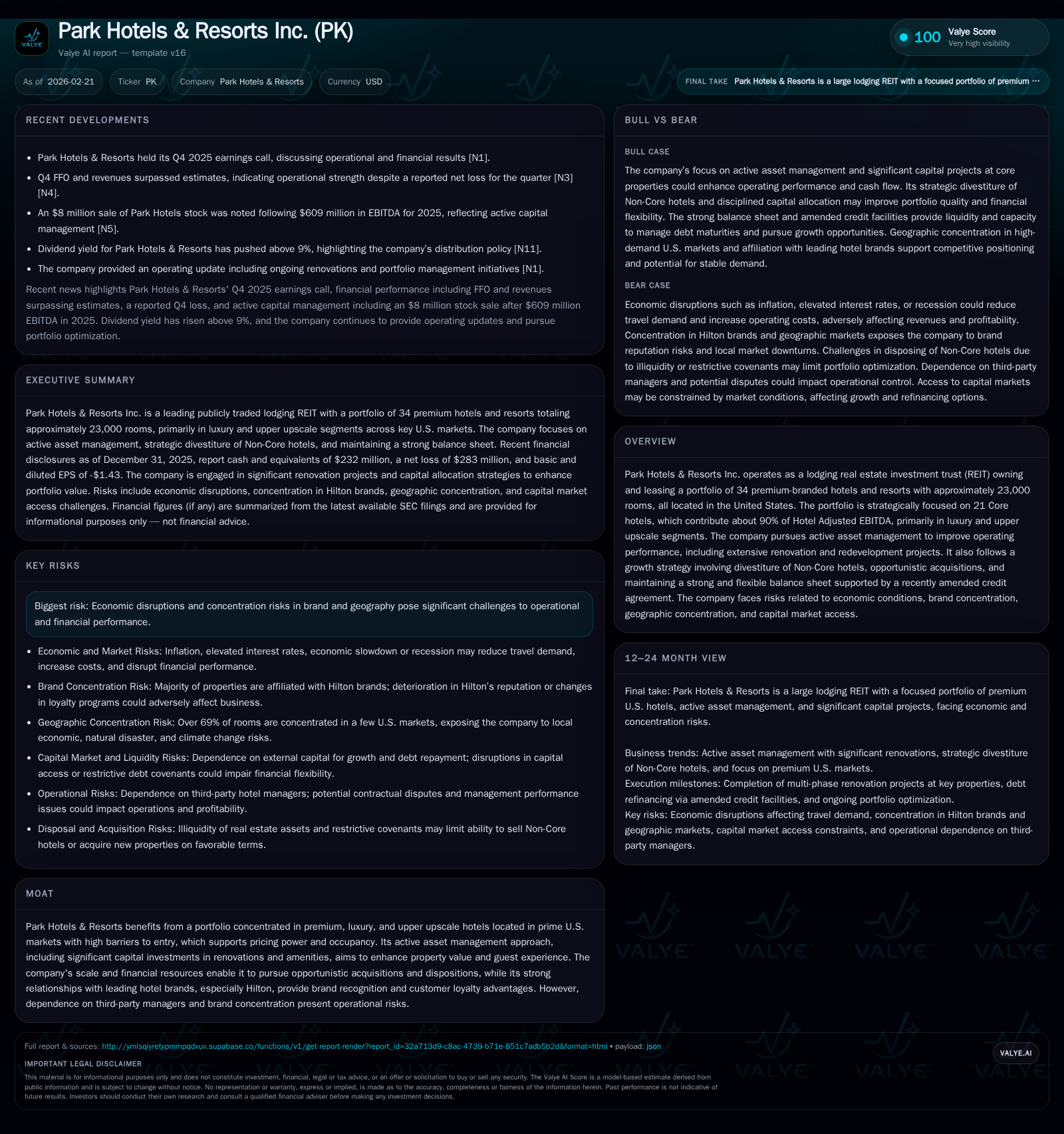

Park Hotels & Resorts Inc. operates a concentrated portfolio of 34 premium-branded U.S. hotels focused on the luxury and upper upscale segments, driving roughly 90% of EBITDA from its core 21 properties. Despite solid revenue trends, the company reported a significant operating loss in 2025 driven by elevated capital expenditures and lower operating income compared to prior years. Renovation projects across flagship properties and a strategic disposition of non-core assets define its growth approach, alongside maintaining liquidity through an amended credit facility. The firm faces risks from geographic concentration, brand dependencies, and macroeconomic headwinds impacting travel demand and costs.

Company Overview

Park Hotels & Resorts Inc. (Ticker: PK) is one of the largest publicly traded lodging REITs focusing exclusively on premium-branded hotels and resorts located solely within the United States. As of early 2026, the company owns or leases 34 properties with close to 23,000 rooms concentrated primarily in luxury and upper upscale segments, where it derives approximately 90% of its Hotel Adjusted EBITDA from its core portfolio of 21 hotels including one unconsolidated joint venture [S1],[S25]. The portfolio benefits from strategic location concentration in high-barrier-to-entry markets such as Florida, Hawaii, Chicago, New York City, New Orleans, and Boston representing over two-thirds of room count—an advantage supporting premium pricing yet exposing PK to heightened geographic risk [S19],[S25].

The company pursues an active asset management strategy designed to enhance operating performance via third-party managers complemented by extensive capital investment programs focused on comprehensive renovations and repositionings intended to maintain competitiveness and improve guest experience. Simultaneously, Park Hotels has a deliberate external growth strategy involving opportunistic acquisitions balanced against divesting non-core assets to optimize portfolio quality and financial flexibility [S1],[S14],[S25].

Historical Performance

Financially, Park Hotels demonstrated consistent revenue growth earlier this decade; however, recent years have been marked by significant volatility primarily influenced by extensive capital spending cycles and fluctuating operating results. The following table summarizes key annual financial metrics for FY 2022 through FY 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -283 | 398 | -33 | 296 | -233.5% |

| 2024 | 212 | 429 | 391 | 227 | +118.6% |

| 2023 | 97 | 503 | 343 | 285 | -40.1% |

| 2022 | 162 | 409 | 296 | 168 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 280 | 45 | 102 |

| 2024 | 512 | 116 | 202 |

| 2023 | 152 | 180 | 218 |

| 2022 | 7 | 227 | 241 |

Source: SEC companyfacts cache [F1].

Note: Revenue annual data not consistently available; operating income figures derive from SEC-tagged data [F1].

Operating income deteriorated sharply in FY2025 into negative territory due primarily to increased depreciation and expenses associated with ongoing renovation projects as well as possible impairments or mark-to-market adjustments detailed in earnings disclosures [N1],[N5],[F1]. Net income mirrored this trend with a steep loss following positive net profits in prior years supported by steady operational cash flows.

Operating cash flow remained robust around $400 million annually but shows some decline attributable partly to working capital changes amid construction activities. Notably, capital expenditures surged over recent periods—reaching $296 million in FY2025—reflecting major renovation investments especially at Hawaiian resorts such as Hilton Waikoloa Village and Hilton Hawaiian Village Waikiki Beach Resort, along with the Royal Palm South Beach Miami property renovations projected for completion by mid-2026 [S12],[S14]. Despite elevated spending, Park Hotels maintains positive free cash flow (~$102 million estimate for FY2025), underscoring operational resilience.

Dividends paid have been substantial reflecting REIT distribution requirements but declined from over half a billion dollars in FY2024 to $280 million in FY2025 as management balances shareholder returns against reinvestment needs. Share repurchases also contracted notably last year signaling a more cautious capital allocation stance amid industry headwinds [F1].

Growth Prospects

Park Hotels’ future growth hinges largely on its ability to successfully execute ongoing asset renovations that enhance brand positioning and command higher average daily rates and occupancy within core assets, notably its presence in convention-heavy and resort markets with large meeting spaces that generate stable group revenue streams [S14],[N1]. Active asset management initiatives extend beyond guestroom upgrades to lobby transformations, food-and-beverage enhancements, recreational amenities expansions including golf course refurbishments, retail platform developments on vacant land parcels, and optimizing underutilized areas—a multipronged approach intended to boost property valuations.

The company also pursues selective dispositions of non-core hotels that historically underperform or fall outside target segments. Since spinning off from Hilton parent company in 2017, Park Hotels has divested about fifty-one lower-growth properties totaling around $3 billion proceeds which it redeploys into deleveraging and enhancing core portfolio returns [S14]. Further non-core sales remain part of their strategic roadmap thus creating potential capital recycling opportunities.

On the acquisition front, while no major new hotel purchases have been disclosed since the Chesapeake Lodging Trust acquisition in late-2019, Park intends to opportunistically capture accretive investments aligned with its brand affiliation pillars primarily under Hilton Family Brands including Waldorf Astoria luxury offerings as well as Marriott Tribute Portfolio properties when beneficial market conditions arise [S1],[S14],[N4].

Financially the recently amended credit agreement bolsters Park Hotels’ liquidity with an expanded $1 billion revolving credit facility coupled with an incremental $800 million delayed draw term loan due largely in early next decade allowing for refinancing existing mortgage maturities amounting approximately $1.4 billion during calendar year 2026 [S4],[S8],[S9]. This conservative financial posture allows flexibility needed amid lodging cyclicality while supporting continued capex outlays.

At present though macroeconomic factors including inflationary pressures driving labor costs higher coupled with potential recessions pose risks to room demand trends impacting occupancies negatively [S17]. Dependency on Hilton’s branding exposes the company to operational risks should there be brand dilution or customer loyalty erosion considerations [S22]. Geographic concentration further intensifies vulnerability especially given adverse weather events or climatic shifts threatening coastal resorts worth noting under industry-specific ESG scrutiny.

Forecasts & Milestones

Explicit forward-looking earnings guidance has not been formally released; however Q4 earnings commentary suggested stabilization efforts centered on completing renovation cycles by mid-2026 intending eventual margin expansion enabled by enhanced guest experiences fostering improved revenues per available room (RevPAR) metrics alongside cost optimization partnering with third-party operators [N1,N5,N6].

Key milestones include:

- Final phase completion at Hawaii hotels into early/mid-2026 for investment exceeding $150 million across two resorts,

- Reopening of Royal Palm South Beach Miami following a comprehensive overhaul slated for June-July calendar midyear,

- Continued disposition activity for remaining non-core assets announced opportunistically,

- Planned drawing under delayed draw term loan facility planned within the first half of calendar year to refinance existing debt maturities,

- Monitoring macroeconomic indicators closely impacting travel behavior for prompt adaptive responses.

Watching trends in RevPAR recovery post-renovations will be critical along with operating margin progression after absorption of current higher cost burdens tied to investment activities forms key analytical focal points moving forward.

Returns & Capital Allocation

Return on equity turned negative around minus nine percent as losses outweighed equity base driven largely by impairment charges linked to recent asset repositionings combined with interest expenses related to debt servicing costs [F1]. This profitability dip contrasts prior years' positive ROEs indicating cyclical disruptions albeit offset partially by solid underlying cash flow generation.

Capital allocation approach balances dividend obligations pursuant to REIT regulations against reinvestments into core portfolio refreshment endeavors reflecting shift toward long-term value creation over short-term payout maximization [S12],[F1]. Dividend distributions were scaled back markedly in fiscal year 2025 but remain material paying out nearly eighty percent+ of operating cash flows supporting investor returns.

Share repurchase programs persisted though throttled back significantly relative to prior periods signaling prudent liquidity management amid uncertain economic outlooks. Parking near $45 million spent on buybacks shrank substantially versus over $100 million executed the prior year reflecting desire to preserve cash headroom.

While specific metrics like FFO or AFFO guidance are not explicitly detailed in corporate disclosures this sets-up monitoring for future quarterly updates particularly surrounding renovation completions impact alongside leverage ratios tied into credit covenants ensuring compliance.

Industry Dynamics & Risks

Park Hotels operates within a highly competitive lodging sector dominated by other REITs as well as private equity groups owning similar upper upscale hotels often competing aggressively both for guest business and acquisition targets contributing pricing pressures potentially constraining margins [S20].

The industry is subject to cyclical volatility magnified recently by global events such as the COVID-19 pandemic disrupting demand patterns; future pandemics or geopolitical shocks could return volatility unexpectedly adversely affecting occupancy fee structures broadly.[S1]

Rising labor costs intensified by shortages affect operational efficiencies; guest preferences evolve necessitating constant innovation requiring ongoing capital investments which may strain resources if poorly timed.[S17]

Further concentration risks arise from reliance mainly on Hilton system brands providing loyalty program benefits yet exposing Park Hotels heavily should brand reputational damages emerge.[S22]

Geographical concentrations heighten vulnerabilities notably exposure along coastal areas subject to climate risks including hurricanes or sea-level rise necessitating additional mitigation costs impacting profit margins longer term.[S19]

Regulatory demands around environmental compliance escalate expenditures while cybersecurity threats loom requiring investment safeguarding data integrity posing incremental cost burdens.[S28]

Conclusion & Watch Points

Park Hotels & Resorts stands at a pivotal juncture balancing heavy reinvestment cycles into premium properties aimed at securing long-term competitive advantage while navigating near-term profitability swings evidenced by operating losses last fiscal year paired with meaningful capex uptick. Successful execution of renovations coupled with disciplined capital deployment via strategic dispositions will be vital.

Monitoring quarterly EBITDA trends post-renovation completions alongside debt utilization levels within covenant bands will provide key signals regarding operational recovery momentum and financial health sustainability.

Investor focus should remain attuned to evolving macroeconomic conditions affecting travel demand elasticity plus brand partner execution efficacy given extensive dependency plus regulatory/ESG developments influencing cost structures.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations regarding securities of Park Hotels & Resorts Inc., nor any suggestions regarding buying or selling such securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments