Julong Holding Ltd: Navigating Early Growth Amid Regulatory and Transparency Challenges

An in-depth review of Julong Holding's IPO progress, integrated solutions business, financial development, and tax risk environment.

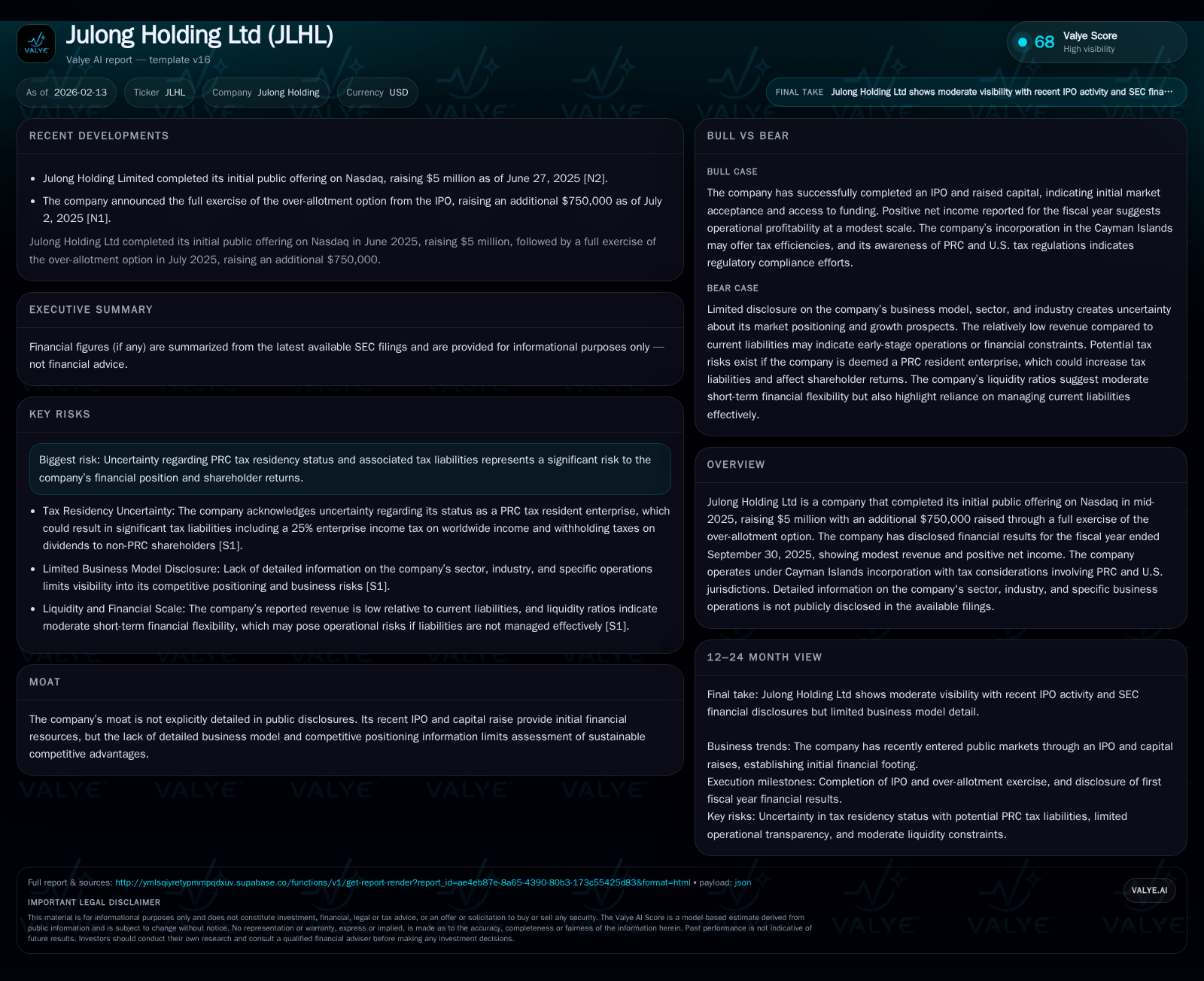

Julong Holding Ltd emerged as a newly public player in late 2025 via a Nasdaq IPO, secured $5.75 million in capital, and reported steady revenue growth paired with positive net income for FY2025. Its core business centers on delivering sophisticated smart infrastructure systems to urban Chinese utilities and multifamily properties, despite limited public disclosure of detailed sector classification. Notably, Julong faces complex taxation ambiguities stemming from its Cayman Islands domicile and uncertain PRC tax residency status, which pose considerable risk to its financial outlook. The company’s initial performance suggests operational resilience but also highlights challenges tied to competitive tender processes and cost pressures in an evolving regulated landscape.

From IPO Launchpad to Market Reality: Julong Holding’s Nascent Journey

In mid-2025, Julong Holding Ltd marked its official entry into the public markets through a Nasdaq initial public offering that raised approximately $5 million in primary capital alongside a full exercise of the over-allotment option adding $750,000 more. This early-stage capital injection serves as a foundational platform for the company's growth ambitions but simultaneously reflects modest scale relative to many U.S.-listed peers [S1], [F1]. Incorporated in the Cayman Islands with principal executive offices registered in Beijing, China, Julong occupies a complex jurisdictional stance with potential implications on regulatory oversight and investor sentiment.

As a recently public entity, Julong disclosed its first comprehensive annual results for the fiscal year ended September 30, 2025. The financials reveal an encouraging trajectory marked by steady revenue expansion—from RMB119 million (roughly USD $16.8M) in FY2023 to RMB252 million (~USD $35.4M) in FY2025—alongside positive net income scaling from RMB11.2 million (approx USD $1.6M) to RMB26.2 million (about USD $3.7M) over the period [S1], [F1]. This supportive data paints a picture of operational momentum yet also houses caution given still relatively limited absolute size.

Conspicuously absent from public disclosures is an explicit sector or industry classification detailing Julong’s specific market positioning or competitive landscape beyond broad references to intelligent solutions servicing public utilities and property management sectors within China. This opacity challenges external analysts attempting to fully contextualize Julong's niche or moat [S1], underscoring the transitional nature of its information profile consistent with many small-cap foreign private issuers newly listed on U.S. exchanges.

Decoding the Core Business: Intelligent Integrated Solutions in Chinese Urban Infrastructure

Julong positions itself as a professional provider of intelligent integrated solutions designed primarily for China's urban utilities infrastructure along with commercial and multifamily residential properties. Their system portfolio includes:

- Intelligent security surveillance

- Fire protection apparatus

- Parking management systems

- Toll collection technologies

- Public broadcasting frameworks

- Identification authentication mechanisms

- Data room infrastructures

- Emergency command centers

- Comprehensive city management platforms

These offerings reflect an integrated approach targeting digital transformation within municipal services and real estate operational efficiency [S1]. By consolidating multiple subsystems into cohesive solutions, Julong ambitiously aims to simplify management processes for clients while driving long-term cost savings and operational reliability.

Business lines divide into three main streams:

- Engineering solutions focused on installation and customization of intelligent projects

- Ongoing operation and maintenance services ensuring functionality and support continuity

- Sales of equipment and materials necessary for these smart systems

Integral to Julong’s value proposition is 'one-stop' service delivery matched with stringent quality assurance policies that emphasize high standards alongside long-term customer relationships bolstered through collaboration with technical installation teams sharing core corporate values [S1]. Such integration indicates not merely product sales but embedded service contracts fostering recurring revenue opportunities.

Financial Trajectory: Growth in Revenue, Profit, and Backlog Analysis

Julong's reported revenues for fiscal years ending September 30 grew from RMB119 million (USD ~$16.8M) in FY2023 to RMB252 million ($35.4M) by FY2025—a compound annual growth rate exceeding 40%, marking robust top-line expansion during this nascent stage [S1], [F1]. Concurrently net income surged from RMB11.2 million ($1.6M) to RMB26.2 million ($3.7M), revealing margin improvement potential alongside enhanced scale advantages.

A critical component underpinning future revenue visibility lies within Julong’s contract backlog:

- Engineering solutions backlog: RMB32.5 million (~$4.6M)

- Operation & maintenance backlog: RMB16.4 million (~$2.3M) Totaling roughly RMB48.9 million or about USD $6.9 million as of FY-end 2025 [S1].

This balance between project design-delivery work and ongoing maintenance contracts underscores an increasingly diversified revenue base spanning one-time engineering fees plus stable service contract streams.

Geographically rooted wholly within China’s urban environments, these contracts benefit from national digitization drives but remain susceptible to macroeconomic trends influencing infrastructure investment rates [S1].

Competition and Cost Dynamics: Navigating Market Pressures in a Tender-Based Industry

Julong operates within a competitive bidding environment where projects are awarded after tender submissions reflecting both estimated project costs plus targeted mark-ups aimed at sustaining margins [S1]. The company explicitly identifies escalating competition as a material operating risk; rivals may aggressively lower prices or enhance solution attractiveness thus compelling Julong to adjust margins downward during intense bidding rounds.

Cost control emerges as another pivotal challenge since costs comprise predominantly direct labor expenses along with materials procurement—both subject to inflationary pressures amid China's dynamic economic context [S1]. Any misestimation exposing the company to cost overruns or project delays could materially erode profit margins or strain liquidity.

Management's disclosures regarding pricing strategies reveal they adapt bids based on competitive intensity but aim to balance margin preservation while securing new contracts essential for backlog renewal and staff retention [S1]. This balancing act remains delicate given tender-driven contracting inherently pressures profitability especially for smaller players seeking scale economies.

Strategic Partnerships and Supply Chain Foundations

To maintain product quality across their integrated intelligent systems Julong depends heavily on stable supplier relationships providing equipment components central to their solution assemblies [S1]. Suppliers wield significant influence as they control supply access plus technological contributions that augment customer appeal.

While suppliers have no binding obligation for long-term exclusivity or defined pricing terms beyond contractual agreements, maintaining mutually beneficial ties underpins Julong's ability to competitively differentiate through breadth of offerings combined with proprietary system integration expertise [S1].

Disruptions or deteriorations in supplier cooperation could jeopardize product reliability or inflate costs thereby raising execution risks particularly given evolving technology standards within smart city domains.

Cybersecurity Governance: Board-Level Oversight of Emerging Digital Risks

Recognizing the inherent risks linked with IT-driven solutions servicing critical infrastructure sectors, Julong has proactively instituted comprehensive cybersecurity governance policies framed around confidentiality/integrity/availability principles enforced through company-wide protocols [S1].

Oversight responsibilities reside principally with the board's audit committee which regularly reviews cybersecurity strategy implementation effectiveness alongside related risk metrics [S1]. Operationally assigned team leaders report directly into senior management ensuring cross-departmental coordination consistent with industry best practices even at this smaller scale.

Employee guidelines enforce stringent limits on proprietary data access reinforcing internal controls against inadvertent breaches or intentional misuse [S1]. Despite no identified cyber incidents adversely impacting operations thus far—a notable disclosure contrasting many small emerging firms—the firm anticipates ongoing exposure due to increased prominence within digital ecosystems that attract potential threat actors.

This layered cybersecurity framework exemplifies prudence by embedding risk awareness culturally while elevating monitoring regimes embedding resilience foundationally into organizational practices.

Complex Tax Landscape: PRC Residency and Jurisdictional Implications

Perhaps most materially opaque yet impactful is Julong’s uncertain tax residency stemming from provisions under China’s Enterprise Income Tax (EIT) Law administered through circulars like SAT Circular 82 dictating criteria for deeming offshore entities resident taxable enterprises if 'de facto management bodies' operate predominantly within mainland China [S1].

The company holds Cayman Islands incorporation—a jurisdiction without corporate income taxes—but sustained operational control exercised largely from China complicates definitive residency conclusions potentially triggering retroactive PRC enterprise income tax obligations at standard rates near 25% on global income streams.[S1]

Interpretation uncertainty generates catastrophic risk possibilities including heightened tax liabilities plus penalties undermining earnings sustainability while clouding shareholder returns visibility especially juxtaposed against U.S.-based listings where regulatory scrutiny around foreign private issuer tax compliance intensifies continually.

This unresolved structural dichotomy surfaces repeatedly as a core risk theme emphasizing regulatory unpredictability inherent for foreign-listed Chinese enterprises despite nominal operational progress.[S1]

Outlook and Risks: The Balancing Act Between Expansion Potential and Regulatory Vulnerabilities

Looking ahead, Julong faces an intricate interplay of growth drivers constrained by external pressures:

- Economic activity levels in China strongly influence public infrastructure investments directly impacting project pipelines.

- Intensifying competition amidst tender-based procurement modes challenges consistent margin achievement.

- Input cost volatility necessitates sophisticated project cost estimation capabilities coupled with operational agility.

- Cybersecurity needs will deepen given digital platform interconnectivity raising vigilance imperative.

- Most critically latent prevailing uncertainties surrounding effective PRC tax residency pose enduring downside tail risks threatening cash flow stability.[S1]

Strategically navigating these vectors requires not only expanding customer penetration via superior project execution quality but also mitigating structural imponderables associated with regulatory jurisdictional complexities diluting pure operational progress visibility.[S1]

Valuation Snapshot and Strategic Considerations for Investors

From a capital structure perspective, post-IPO resources include over $8.7 million cash & equivalents alongside total current assets nearing $46 million balanced against current liabilities about $38 million yielding a liquidity ratio around 1.21—indicating reasonable short-term solvency buffers commensurate with early-stage capital needs but not excessive surplus reserves [F1].

The modest capital raise reflects constrained upfront funding initially limiting expansive R&D or acquisition maneuvers but likely aligns well with controlled growth mandates presently achievable within their chosen market segments.[S1]

Given limited publicly available competitive positioning details paired with unresolved taxation ambiguities weighing on certainty over free cash flow persistence beyond nascent profitability phases, valuation approaches require caution emphasizing results monitoring alongside potential shifting regulatory landscapes defining longer-term moats undetermined explicitly thus far.[F1], [S1]

Disclaimer: This analysis is provided solely for informational purposes based on data available as of February 2026 without any investment recommendations or forecasts regarding future stock performance or corporate actions involving Julong Holding Ltd (ticker JLHL). Investors should consider multiple sources alongside professional advice when evaluating opportunities linked to this or related securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments