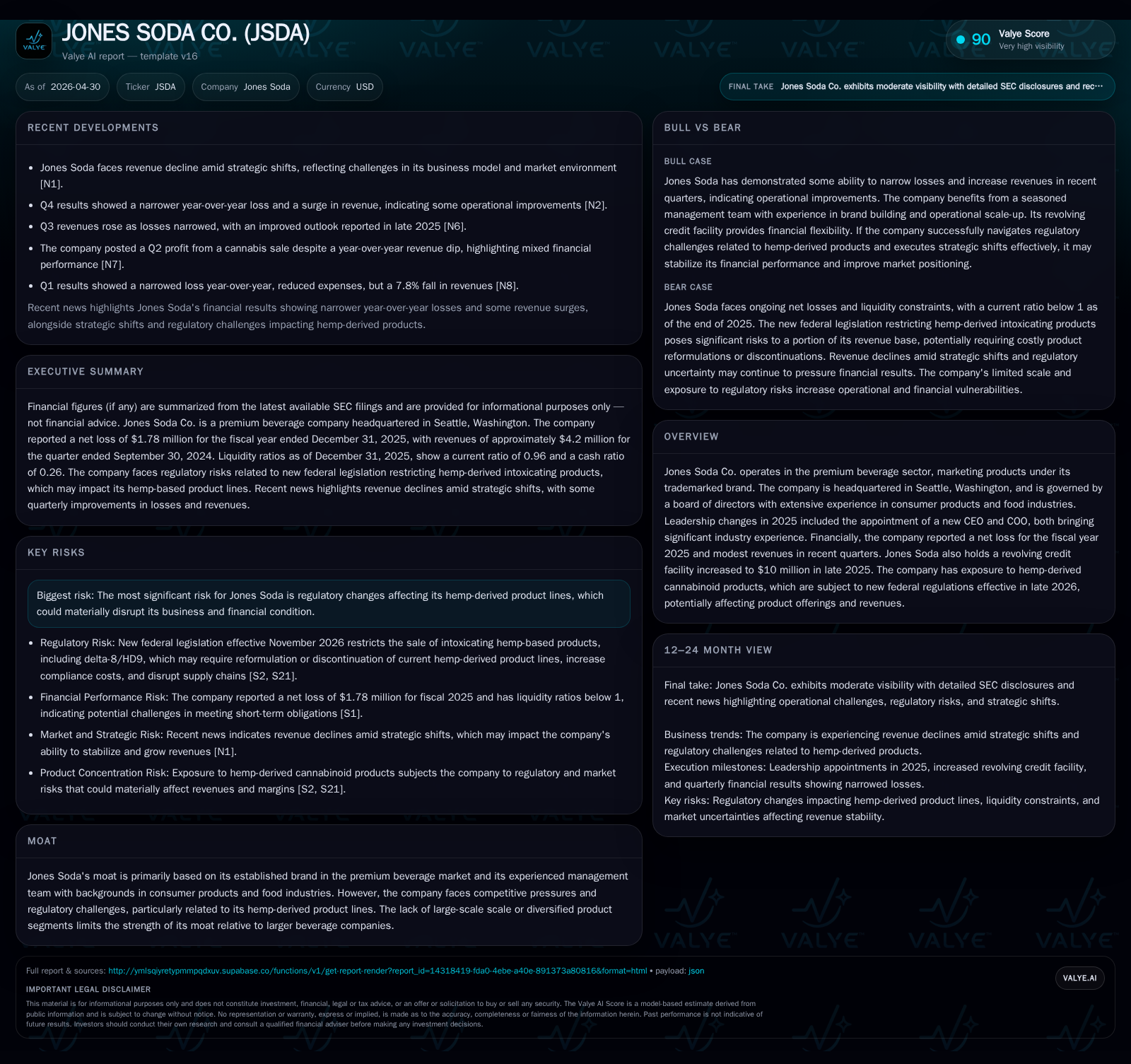

Jones Soda's Brand and Regulatory Challenges Shape 2026 Outlook

Recent federal hemp regulations and strategic management changes are redefining Jones Soda's operational and growth landscape.

Jones Soda recently disclosed heightened regulatory risks from new federal laws targeting intoxicating hemp-derived products, which threaten a core component of its product portfolio. The company faces revenue pressures amid these legislative shifts and is adapting with leadership and operational changes to sustain growth in the premium beverage niche. While brand equity and innovation foster growth opportunities, looming compliance costs and channel restrictions impose significant constraints. Monitoring regulatory implementation and reformulation progress will be critical for assessing Jones Soda’s near-term trajectory.

Latest Operating Developments and Strategic Implications

Jones Soda’s recent disclosures bring sharp focus to escalating regulatory risks tied to its hemp-derived beverage lines. The November 14, 2025 10-Q [S2] highlighted newly enacted U.S. federal legislation transforming the hemp product landscape by imposing a strict total-THC limit of 0.4 milligrams per product and banning intoxicating hemp-based cannabinoids such as delta-8/HD9 without FDA regulation. Implementation is slated for November 2026.

This paradigm shift compels Jones Soda to significantly reformulate or discontinue existing hemp-derived products to achieve compliance. Consequentially, management anticipates accelerated inventory obsolescence triggered by banished formulations, disruptions in supply chain inputs especially upstream intermediates, elevated testing and labeling expenditures, and diminished sales channels due to prohibitions on online marketplaces and convenience store retailing [S2].

In tandem with these headwinds, a corporate governance update filing on April 2, 2026 [S3] detailed amendments to executive stock option vesting for the CFO alongside prior strategic appointments such as the December 2025 induction of Darcey Macken as COO [S27]. Macken brings deep operational expertise scaled from high-growth CPG brands—and her arrival underscores a drive toward tighter organizational execution amidst volatile external conditions.

Recent Nasdaq reporting corroborates ongoing revenue softness linked to these transitions [N1]. Quarter-to-quarter fluctuations embody the challenge of balancing consumer demand volatility against necessary compliance-driven adjustments.

Business Model Overview and Product Portfolio Strengths

Jones Soda generates revenue predominantly through sales of its trademarked "Jones Soda Co." branded beverages—positioned as premium soda products marked by distinctive flavor profiles and innovative packaging. The business model revolves around consumer appeal rooted in differentiated taste experiences coupled with cult-like brand loyalty cultivated over years.

Complementing this core are cannabinoid-infused sodas featuring hemp-derived ingredients like delta-8/HD9 —attractive within emerging wellness trends but now burdened by tightening regulatory scrutiny [S1][S2]. These products historically enhanced both top-line growth potential and gross margin expansion due to higher price points commanded within niche markets.

Revenue streams are volume-dependent but sensitive to pricing power influenced by channel placement predominantly in specialty retailers rather than broad mass-market distribution. Unit economics align with typical small-batch premium beverages—cost-intensive raw materials balanced by avowed ability to command brand premiums.

Recent financial commentary notes a notable revenue surge in some quarters attributed partially to expanded cannabinoid offerings [N2], yet the strategic value is offset heavily by prospects of forced product withdrawals or reformulations.

Competitive Positioning amid Premium Beverage Market Dynamics

Within the broader beverage sector—which features dominant multinational players benefiting from scale advantages—Jones Soda occupies a niche defined by specialized branding and product innovation. The company’s competitive moat is marginally protected via strong brand identification with subcultures favoring craft sodas and flavor experimentation [S1].

However, limitations persist: Jones lacks broad production scale or diversified portfolio breadth found among larger rivals like PepsiCo or Coca-Cola which constrains negotiating leverage with distributors and retailers. Channel fragility emerges particularly acute given evolving regulations curbing sales of intoxicating cannabinoid products through common convenience outlets—a vital pivot point for consumer acquisition in this segment.

Supply chain stability also poses challenges as formulation shifts induced by regulatory demands necessitate agile ingredient sourcing while controlling incremental compliance cost inflation [N1]. Against this backdrop, incremental innovation becomes a necessity rather than an option to preserve shelf presence.

Growth Drivers: Brand Equity and Product Innovation

Despite constraints, Jones Soda retains several identifiable growth levers. Foremost is enduring brand equity underpinning consumer retention within premium soda devotees—a relatively sticky demographic given appetite for novelty combined with nostalgia appeal [S1].

Product innovation continues as both a branding exercise and a direct revenue catalyst; cannabinoid-infused lines have demonstrated episodic momentum fueling quarter-over-quarter top-line improvements pre-regulatory clampdown [N2]. This indicates underlying market receptiveness that could translate into long-term gains if reformulated successfully.

Selective channel expansion initiatives aim at elevating distribution into alternative retail settings less impacted by online/convenience restrictions—potentially specialty natural food stores or experiential venues aligned with lifestyle positioning.

Operational improvements driven by new leadership appointments target scaling efficiencies while maintaining inventive agility—crucial given narrow margin structures currently experienced.

Risks and Constraints: Regulatory Landscape and Revenue Volatility

The November 2025 risk disclosures [S2][S9][S26] explicitly articulate the considerable uncertainty imposed by new federal hemp laws effective late 2026 which could disproportionately disrupt Jones Soda's financial performance. Key risk elements include:

- Mandatory reformulation or cessation of intoxicating cannabinoid sodas causing accelerated inventory write-downs.

- Increased compliance burden across testing protocols, labeling accuracy requirements, and distribution monitoring specifically limiting online marketplaces, gas stations, and convenience store sales.

- Interpretive ambiguities around "similar effect" cannabinoids engender variable enforcement outcomes dependent on forthcoming FDA/HHS guidance due within months post-enactment.

- Litigation exposure stemming from recall mandates or state-federal regulatory misalignments.

- Margin erosion potential due to prohibition of synthesized cannabinoids reducing product differentiation scope.

Management acknowledges these risk vectors but also attempts mitigation via disciplinary control frameworks enacted alongside newest compensation policies linking executive incentives more closely with performance milestones [S3][S21].

Upcoming Milestones and Key Watchpoints

Investors and stakeholders should monitor these critical developments for directional clarity:

- November 2026: Federal hemp product rules take full effect; assess company compliance status including visible product reformulations or discontinuations [S2].

- FDA/HHS publications (expected within one year from legislation): definitive lists clarifying naturally occurring versus prohibited cannabinoids setting enforcement parameters [S2].

- Quarterly earnings releases commencing Q1/Q2 2026: evaluate impact on margins, updated sales mix excluding impermissible products, progress in cost rationalization [N2][S12].

- Inventory write-down disclosures signaling effectiveness of supply chain responsiveness.

- Management execution on operational improvements under new COO influence; tracking vesting milestones for key executives aligned with turnaround objectives [S3].

Consolidated Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.6mm | |

| 2025-12-31 | ||

| Current assets | $13.3mm | |

| 2025-12-31 | ||

| Current liabilities | $13.8mm | |

| 2025-12-31 | ||

| Current ratio | 0.96x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

The latest fiscal year ending December 31, 2025 figures illustrate ongoing financial pressures consistent with narrative tension between growth ambitions versus regulatory-imposed constraints:

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 3,599,000 |

| Current Assets | 13,262,000 |

| Current Liabilities | 13,764,000 |

| Operating Income | -4,766,000 |

| Net Income | -1,779,000 |

| Current Ratio | 0.96 |

Jones Soda operates at an operating loss highlighting margin compression partially attributable to increased costs linked directly or indirectly to regulatory challenges. It does not constitute investment advice or recommendations. Any forward-looking or predictive assessments are inherently uncertain given rapidly evolving regulatory environments affecting Jones Soda’s business model.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments