PS International Group's Freight Forwarding Faces Structural Headwinds and Margin Squeeze

Significant revenue decline and margin compression reveal challenges in PSIG’s air freight business amidst tariffs and liquidity constraints.

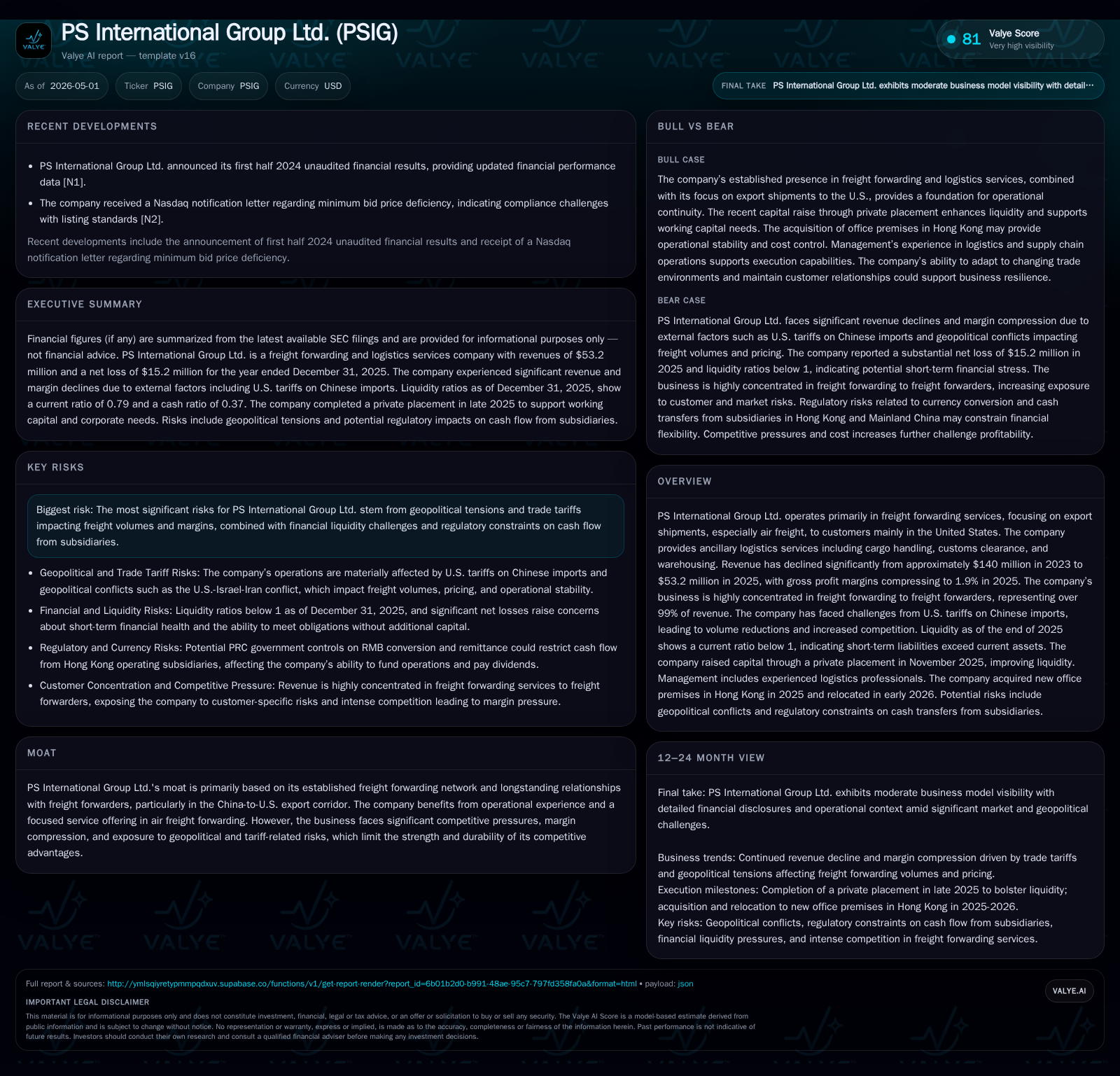

PS International Group Ltd. reported a sharp 39% revenue drop to $53.2 million in 2025, with gross margins compressing to under 2%, reflecting ongoing volume declines largely tied to U.S. tariffs on Chinese imports. The company’s freight forwarding business, focused primarily on air cargo export services to the U.S., shows exposure to geopolitical trade tensions and intense competition. Despite longstanding relationships with freight forwarders, PSIG’s narrow customer concentration and financial liquidity pressures raise questions on its path to profitable growth.

Recent Operating Update

PS International Group Ltd.'s latest quarterly update filed on November 26, 2025 ([S2]) presented unaudited interim condensed consolidated financial statements through June 30, 2025. This update highlighted continued operational stress resulting from declining freight volumes impacted by expanded U.S. tariffs on Chinese imports announced in early 2025 ([S5]). These tariffs critically disrupted the company’s primary trade corridor—China to the United States—leading to a near halving of annual revenues from $87 million in 2024 to just over $53 million for full-year 2025 ([F1], [S1]). The company also completed a private placement capital raise towards the end of 2025 ([S18]) aimed at shoring up liquidity amid widening losses.

The annual filing dated April 30, 2026 ([S1]) confirms that revenue declined by approximately 39% year-over-year while gross profit fell by over 70%, compressing margins drastically to under two percent. Net losses ballooned to $15.2 million—more than tripling the prior year loss—primarily driven by reduced volumes and growing fixed cost burdens despite some scaling back of operating expenses ([F1]).

Business Model

PS International Group Ltd.’s core business is freight forwarding focused on air export shipments predominantly servicing the China-to-U.S. trade route ([S1], ). Revenue is heavily reliant (over 99%) on contracts with freight forwarders rather than direct commercial shippers, making the company a B2B supplier within the logistics chain rather than an end-user facing entity ([S1]). The company complements air freight forwarding with ancillary logistics services including customs brokerage, cargo handling, and storage solutions.

Revenue mechanics are fundamentally volume-driven—PSIG earns fees based on cargo volumes shipped via airfreight complemented by related service charges. Pricing largely depends on negotiated contract rates with freight forwarder customers across major lanes. Thus, variations in shipment volumes driven by macroeconomic trade flows, particularly those influenced by U.S.-China trade barriers, directly impact top-line revenue.

Margins have historically been pressured due to pass-through costs associated with carrier fees, customs duties, and fuel surcharges embedded within cost of goods sold. PSIG’s ability to extract positive gross margins hinges on operational efficiency and pricing discipline within a commoditized freight forwarding landscape where switching costs are low.

Industry Structure and Competitive Position

Within international freight forwarding, PSIG operates as a smaller player with a niche focus on China-origin air exports destined for the United States market segment—a corridor increasingly complicated by shifting tariff regimes reflecting broader geopolitical tensions ([S5]).

The industry is characterized by large multinational integrators such as DHL, FedEx Trade Networks, and Kuehne + Nagel who offer integrated multimodal logistics platforms that combine extensive carrier relationships with advanced technology solutions for supply chain visibility and management—a competitive advantage PSIG lacks in scale.

PSIG's moat derives mainly from its established network of partner freight forwarders within its geographic focus and accumulated operational experience serving this corridor (). However, its reliance on a narrow customer base (with significant related-party transactions) increases concentration risk.

Competitive pressures have intensified due to tariff-induced volume reductions alongside intensified price competition among brokers fighting for diminished cargo flows—a trend reflected in severe margin compression experienced by PSIG moving into 2025 [F1].

Growth Drivers

Growth prospects for PSIG appear structurally constrained amid ongoing U.S.-China trade tensions increasing costs for importers/exporters and reducing overall shipment volumes ([S5], ). Any recovery depends materially on normalization or easing of tariff regimes, which remain uncertain given recent expansions such as the invocation of Section 122 of the Trade Act that added temporary ad valorem tariffs in early 2026 ([S5]).

Operationally, PSIG could seek incremental growth through broadening ancillary logistics offerings (e.g., warehousing solutions) or expanding into additional geographic corridors beyond the China-U.S. axis. However, current financial constraints cap investment capacity needed for such strategic pivots ([F1]).

The private placement executed in November 2025 provides some capital buffer but reflects necessity for cash flow relief amid weakening operations ([S2], [S18]). Technology adoption or alliances may boost service quality or customer retention; however, no immediate evidence of such initiatives exists within filings.

Risks and Constraints

PS International Group Ltd.’s most acute risk lies in exposure to fluctuating geopolitical factors notably U.S. tariffs targeting Chinese imports which materially disrupt freight volumes and erode pricing power ([S1], [S5]). This external macro driver translates into volatile revenue streams and profitability instability.

The company faces liquidity challenges evidenced by a current ratio below unity (0.79), indicating short-term liabilities exceed available current assets at year-end 2025 ([F1]), raising concerns about working capital adequacy especially given negative operating cash flow trends (-$1.3 million) exacerbated by elevated capex spend ($4.2 million) without corresponding earnings improvement ([F1]).

Additional risks stem from internal control deficiencies flagged as material weaknesses around financial reporting integrity which could undermine investor confidence or invite regulatory scrutiny if unaddressed ([S11], [S22]).

Customer concentration risk remains significant since over 99% of revenue comes from related-party or single sector freight forwarding contracts; loss or renegotiation could sharply impact revenues (5[S1]). The competitive environment offers limited differentiation beyond network relationships creating potential pricing pressures.

Finally, regulatory constraints specific to subsidiaries’ cash flow remittance capabilities might restrict group-level liquidity flexibility limiting strategic operational adjustments (, inferred analysis).

What to Watch Next

- Regulatory developments around U.S.-China tariffs including potential trade negotiations or tariff rollbacks that could revive transpacific air cargo volumes.

- Quarterly/interim operating metrics post-June 2025 especially volume trends as reported in future SEC filings starting mid-2026.

- Progress on remediation efforts addressing identified internal control weaknesses impacting timely financial reporting quality.

- Strategic initiatives around broadening service offerings beyond pure forwarding or geographical diversification highlighted in investor communications.

- Liquidity trajectory especially after deployment of proceeds from November 2025 private placement alongside capital expenditures focused on infrastructure acquisitions like new office premises reported during early 2025 ([S25]).

- Customer contract renewals or expansions signaling demand stabilization or growth potential.

Financial Profile (Supporting Evidence)

Historical performance (annual)

Capital returns and efficiency (annual)

FY End 12/31/25 |

The income statement confirms severe deterioration: revenues declined nearly two-fifths year-over-year while net losses widened significantly due mostly to margin compression and non-cash charges associated with warrant liabilities issued in private placements ([F1], [S1], [S18]). The company’s balance sheet at year-end 2025 shows a current ratio of 0.79, indicating current liabilities exceed current assets ([F1]). Net debt is negative at approximately -$5.3 million, reflecting a net cash position when subtracting total debt from cash and equivalents ([F1]). Cash flow metrics indicate persistent negative operating cash flow coupled with elevated capex largely reflecting property acquisition moves supporting office relocations announced for early/mid-2026 periods ([S25]). These expense patterns further strain free cash flow generation requiring close monitoring.

Overall equity turned negative by year-end signaling accumulated losses eroding shareholders’ capital base which may affect access to external capital markets absent operational turnaround or restructuring measures.

This report is prepared solely for informational purposes based on publicly available filings without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments