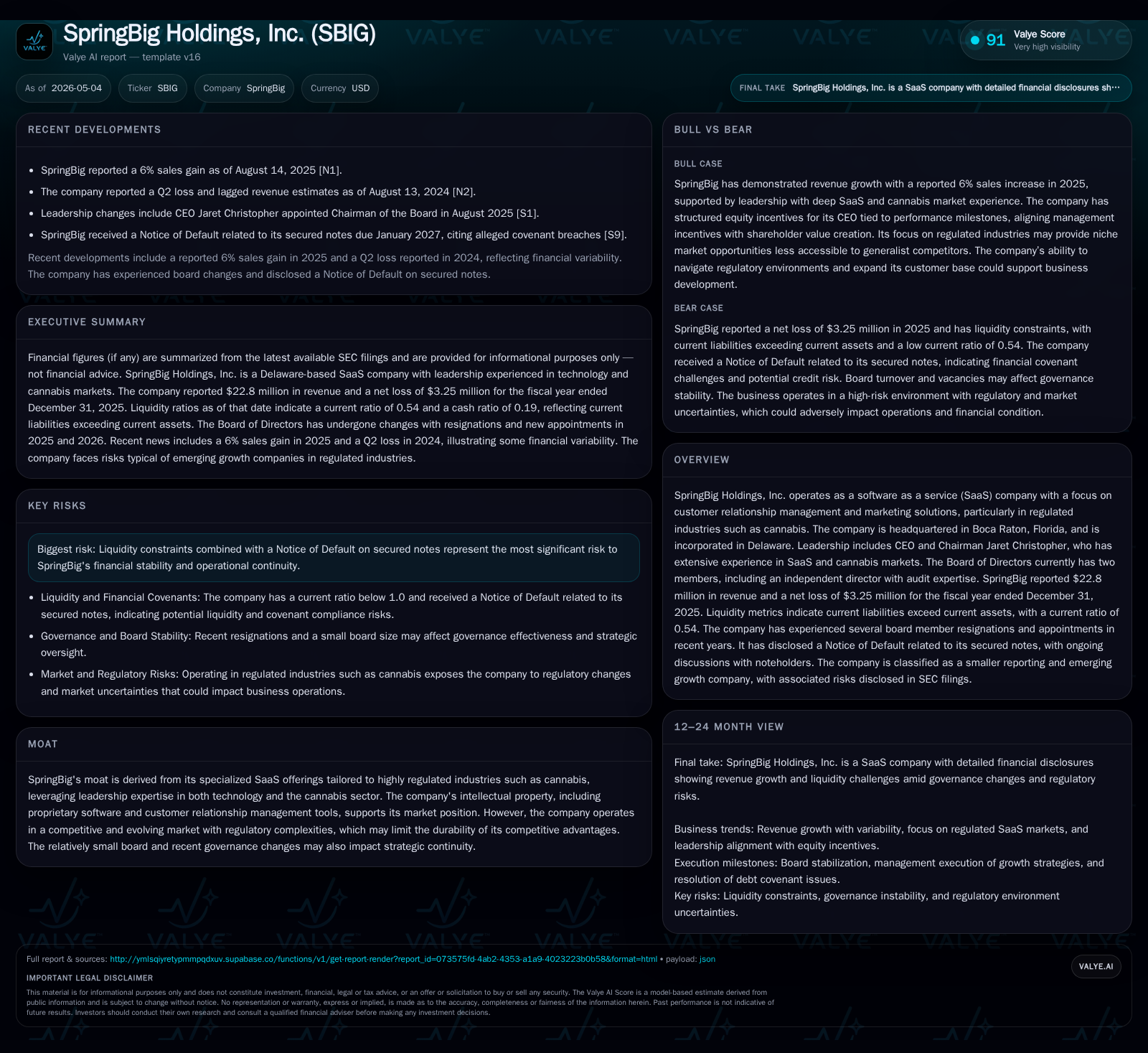

SpringBig Holdings Faces Financing Tests While Sharpening Cannabis CRM Solutions

SpringBig confronts a Notice of Default on its secured notes amidst efforts to expand its niche SaaS platform for regulated cannabis retailers.

In April 2026, SpringBig Holdings received a Notice of Default on its secured term and convertible notes despite current payments and ongoing negotiations with lead noteholders. The company’s specialized SaaS platform targeting highly regulated industries—primarily cannabis retail—positions it well for market growth, but continuing liquidity constraints and regulatory complexities weigh on its operational flexibility. Growth hinges on expanding customer penetration in emerging legal markets and leveraging proprietary CRM solutions, while key risks include refinancing challenges and governance continuity.

Recent Operational Developments and Capital Structure Update

SpringBig Holdings’ most consequential recent development is the receipt of a Notice of Default dated April 21, 2026, concerning its 2024 Secured Term Notes and Convertible Notes due January 2027 [S3]. Despite being current on all payments through early 2026 and actively negotiating with its two principal noteholders—Shalcor Management, Inc. and Lightbank II, L.P.—the company was cited for three alleged events of default. Additional allegations pertain to failures in meeting certain material obligations under the note agreements.

This formal notice signals acute financial stress that could accelerate obligations or precipitate enforcement actions unless resolved before maturity. Contextually, SpringBig ended calendar year 2025 with liquidity strains: current assets totaled approximately $4.18 million against current liabilities of about $7.71 million, yielding a current ratio of just 0.54 [F1]. Cash and equivalents stood at roughly $1.5 million [F1], underscoring limited cushion against short-term obligations.

Taken together, these developments mark a critical inflection point potentially compressing operational flexibility amid the company’s reorientation efforts post-CEO transition in early 2025 [S1]. The default notification adds urgency to capital structure repair initiatives currently underway.

Business Model Overview: Specialized SaaS for Regulated Industries

SpringBig operates as a software-as-a-service (SaaS) provider delivering customer relationship management (CRM) and marketing solutions tailored specifically for highly regulated industries, with cannabis retail as its core focus [S1]. Its platform provides dispensaries and ancillary businesses the ability to engage customers via loyalty programs, targeted promotions, and compliance-aligned communications.

Revenue primarily derives from recurring subscription fees linked to license usage of its proprietary software suite complemented by ancillary service charges for onboarding or enhanced data analytics capabilities [S1]. The company’s intellectual property assets encapsulate the specialized workflows required to navigate strict state-by-state cannabis regulations around marketing messaging and transaction tracking.

Leadership expertise uniquely straddles the SaaS technology domain and cannabis market dynamics—two complex arenas requiring nuanced understanding for product relevance and adoption [S1]. This integration supports a moat based on sophisticated domain-specific features that generalist SaaS competitors cannot easily replicate.

Customer stickiness benefits from high switching costs engendered by regulatory calibration needs and integration depth within client operations. However, the company's relatively modest scale limits its bargaining power with larger enterprise clients.

Competitive Set and Regulatory Environment in Cannabis CRM

The cannabis software ecosystem is characterized by few dominant incumbents addressing both compliance hurdles and marketing intelligence needs. A handful of platforms compete for market share by offering modular loyalty solutions or more comprehensive CRM stacks with inventory control tie-ins [S1]. SpringBig distinguishes itself through deep regulatory specialization combined with flexible cloud delivery facilitating rapid geographic expansion into newly legalized states.

Regulatory fragmentation remains a defining structural feature: each market imposes unique rules governing permissible promotional content, data security standards, and reporting.[S1] These layers elevate barriers to entry but entail continuous product updates, certification efforts, and legal oversight expenditures.

Pricing power is partially preserved by scarcity of tailored solutions but capped by client budgets limited within small to medium dispensary chains. Switching costs also hinge on contractual lock-ins and technical integration complexity with point-of-sale systems—a key distribution channel.[S1]

Capacity-wise, cloud architecture offers scalable delivery; however, human capital specializing in legal/regulatory updates constrains rapid rollouts in new jurisdictions. Demand thus aligns closely with regulatory liberalization speed balanced by compliance burdens.

Growth Drivers: Market Expansion and Customer Penetration Trends

SpringBig’s growth blueprint leans heavily on penetrating emerging legal cannabis markets where contrived supply dynamics fuel demand for compliant CRM tools [S1]. As states continue adopting adult-use legislation or expanding medical dispensary programs, SpringBig’s ready-to-deploy platform offers first-mover advantages.

Further growth avenues include upselling integrated marketing features such as automated personalization engines leveraging customer purchase data analytics. These enhance lifetime value per user and improve margin profiles once platform adoption scales sufficiently.[S1] Cross-selling into ancillary verticals governed by stringent regulations (e.g., pharmaceuticals or alcohol distributors) presents potential pipeline opportunities but remains at exploratory stages.

Measured KPIs likely focus on new customer acquisitions across states legalized during recent election cycles plus retention rates indicating competitive defensibility post onboarding.[S1] Strategic partnerships with point-of-sale providers or payment facilitators could accelerate network effects critical in this niche.

If successfully executed, this formula could enhance revenue visibility supported by multi-year subscription contracts typical in regulated SaaS sectors.

Risks and Watchpoints: Liquidity Constraints and Regulatory Complexity

The immediate risk profile centers on liquidity limitations exacerbated by the Notice of Default concerning contractual covenants under SpringBig’s largest debt tranches [S3]. A current ratio below unity (0.54) at fiscal year-end further stresses working capital adequacy [F1].

Governance aspects add complexity; SpringBig maintains a small board (two members) with recent turnover raising concerns about strategic continuity and robust oversight [S1]. Reliance on founder-CEO leadership heightens execution risk if personnel changes occur unexpectedly.

Regulatory uncertainties in the cannabis market remain volatile due to shifting federal policies despite state-level legalization trends. With notes maturing January 2027, negotiations with lead noteholders regarding restructuring or refinancing solutions require close scrutiny for signs of progress or deterioration [S3].

Simultaneously monitoring customer acquisition metrics especially entry into newly authorized cannabis regions will gauge sales momentum sustaining revenue growth.[S1] Contract renewals reflecting retention levels offer insights into competitive moats effectiveness.

Finally, any shifts in executive roles or board membership warrant attention given historical turbulence around governance transitions reported in recent annual disclosures [S1]. Preservation of leadership stability underpins trust among stakeholders during this financially sensitive phase.

Appendix: Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1500000 | |

| 2025-12-31 | ||

| Current assets | $4mm | |

| 2025-12-31 | ||

| Current liabilities | $8mm | |

| 2025-12-31 | ||

| Current ratio | 0.54x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

(Source: Company facts as of December 31, 2025 [F1])

This snapshot underscores the scale mismatch between operating losses posing profitability challenges alongside thin liquidity buffers threatening near-term solvency absent successful financing measures.

Disclaimer: This analysis is provided solely for informational purposes and does not constitute investment advice or recommendations regarding securities issued by SpringBig Holdings, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments