Volato Group Advances with Strategic Merger and Aviation Platform Expansion

Volato’s imminent shareholder vote on the M2i Global merger and expanded aircraft offerings mark critical turning points for its aviation and technology portfolio.

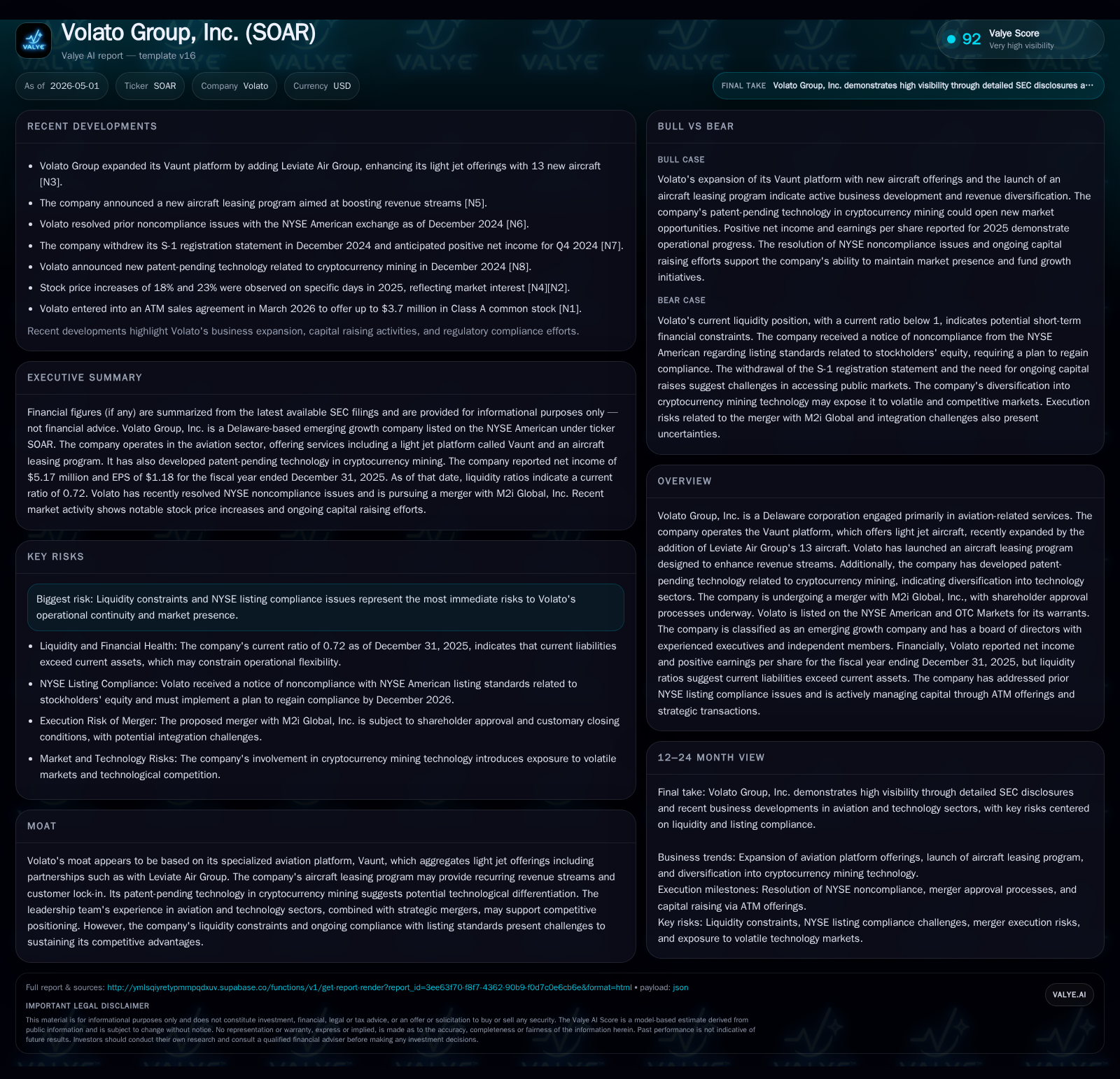

Volato Group is poised at a strategic juncture with a shareholder meeting scheduled for May 7, 2026, to approve its merger with M2i Global, potentially reshaping its operational and financial outlook. The company’s core business centers on the Vaunt platform, an aircraft aggregation service for light jets, recently enhanced by acquiring Leviate Air Group's fleet. Introducing an aircraft leasing program signals a shift toward recurring revenue streams. Additionally, Volato is diversifying with patent-pending cryptocurrency mining technology. Despite promising synergies and diversification, liquidity constraints and compliance challenges with NYSE American listing standards remain key risks.

Merger Update and Near-Term Operating Impact

Volato Group is entering a pivotal phase with a special shareholder meeting announced for May 7, 2026, aimed at approving its merger with M2i Global [S3]. This event follows the necessary procedural steps typical for such transactions, including a proxy statement filed with the SEC detailing voting protocols and proposal specifics distributed to record shareholders as of April 17, 2026. The merger agreement contemplates Volato Merger Subsidiary absorbing M2i Global, with the latter surviving as a wholly owned subsidiary. Approval by Volato’s shareholders represents a crucial inflection point that will set the course of the company's operational trajectory—ushering in the potential integration of complementary businesses, operational synergies, and expanded capabilities.

This shareholder vote is more than administrative; it serves as a strategic gatekeeper determining how effectively Volato can leverage combined assets to scale operations across aviation services and advanced technology ventures. The company disclosed executing pro forma combined financials tied to this transaction, signaling preparation for operational integration challenges ahead. The final resolution of this vote will shape subsequent disclosure on synergy realization timelines and incremental growth prospects [S3].

Business Model Overview: Vaunt Platform and Aircraft Leasing

Volato’s primary revenue mechanism operates through the Vaunt platform—a specialized light jet aircraft aggregation service that consolidates offerings from various operators into an accessible digital interface. This platform recently expanded materially when Volato assimilated Leviate Air Group’s fleet comprising 13 aircraft into its portfolio [S1][F1]. This acquisition enriches Vaunt’s inventory breadth enhancing customer choice within the niche but competitive light jet segment.

Revenue generation is driven chiefly by customers who pay for flight access through Vaunt’s platform—likely structured around individual charter fees or subscriptions enabling streamlined booking experiences. Complementing this transactional flow, Volato has launched an aircraft leasing program intended to shift some revenue streams from one-time bookings toward recurring income via lease agreements [S1]. Such leases potentially involve fixed monthly payments over contract tenures which promote customer stickiness while smoothing cash flows in volatile demand periods.

Beyond aviation services, Volato also pursues ancillary technology fields via patent-pending cryptocurrency mining hardware or software innovations [S1]. This diversification may offer future licensing revenues or direct mining-generated cash flows but remains exploratory relative to the core business.

Overall, value resides in integrating fleet supply (ownership or control), proprietary platform convenience that reduces friction between operators and clients, plus leasing initiatives that anchor customer relationships longer term.

Competitive Positioning within the Specialized Aviation Sector

Within the light jet market segment, where asset capital intensity and operational regulatory burdens act as high entry barriers, Volato leverages partnerships like that with Leviate Air Group to attain scale quickly without sole reliance on organic fleet acquisition [S1]. This aggregation model fits an industry increasingly valuing flexibility and instantaneous access over traditional ownership models.

Pricing power stems partly from catering to affluent clientele seeking convenience combined with availability of localized light jets—where switching costs arise through operator familiarity and integrated scheduling efficiencies facilitated by Vaunt’s digital ecosystem.

Still, challenges persist around maintaining fleet utilization rates amid cyclic aviation demand fluctuations driven by macroeconomic factors or shifting travel patterns. Regulatory oversight affecting aircraft leasing structures requires careful compliance management due to jurisdictional variations on leasing contracts, especially as safety certification norms evolve.

Furthermore, industry reputation and brand trust play outsized roles given client sensitivity toward reliability in private air travel—making leadership pedigree a subtle moat factor given management’s deep experience spanning investment banking (Alan D. Gaines) and industrial sectors allied to logistics/energy domains [S1].

Growth Catalysts: Fleet Expansion, Leasing Programs, and Technology Ventures

Incremental growth drivers rely significantly on enhancing fleet size accessible within Vaunt’s platform. The recent addition of Leviate's 13 aircraft is expected not only to immediate increase volume capacity but also strengthen pricing leverage through a wider selection available to varied client profiles seeking short-notice flights or specific regional coverages [S1][F1].

The aircraft leasing program further diversifies revenue mix—early traction here could contribute recurring cash flows less sensitive to discretionary charter demand cycles than outright flight sales. Leasing contract lengths (tenure) serve as key KPIs influencing near-term revenue predictability and embedded renewal probabilities sustain longer-run customer engagement levels.

In parallel, successful commercialization or licensing of the company’s cryptocurrency mining patent-pending assets could unlock technologically driven revenue streams outside core aviation pathways. If traction materializes here—whether via royalties or direct equipment deployment—it would represent strategic differentiation blending aerospace focus with emergent tech innovation [S1].

Monitoring Key Performance Indicators such as average fleet utilization percentages post-acquisition integration, volume growth in active lease agreements including gross booked lease amounts/timespans, along with milestones in technology development phases will yield actionable insights into trajectory progression.

Risks and Constraints: Listing Compliance and Liquidity Challenges

While operational initiatives bear promise, pressing risks revolve around financial solidity demonstrated by recent liquidity metrics. As of December 31, 2025, Volato presents current assets totaling approximately $9.81 million versus current liabilities exceeding $13.7 million—resulting in a current ratio below unity at ~0.72 which flags potential working capital pressures [F1].

Coupled with this is NYSE American ongoing scrutiny regarding listing standards compliance tied specifically to equity thresholds relative to prior operating losses noted in previous filings [S4]. Execution risk amid merger integration activities also includes potential delays in synergy achievement or cultural mismatches impeding seamless operations—a typical hazard when combining entities within specialized sectors.

Liquidity constraints limit investment bandwidth for fleet expansions or R&D acceleration in crypto mining ventures; thus financial discipline alongside timely capital raises will be pivotal enablers governing pace at which strategic ambitions become realized.

Key Milestones to Monitor: Shareholder Vote, Integration Progress, Revenue Streams

Upcoming events spotlight critical near-term milestones:

- May 7, 2026: Shareholder vote results will determine merger closing timeline certainty; any delays here cascade downstream integration plans impacting reported combined revenues.

- Post-merger: Assimilation effectiveness measured through consolidated fleet utilization metrics across expanded Vaunt offerings including Leviate assets; early leasing program revenue run-rate cadence against targets will validate commercial assumptions.

- Quarterly disclosures (post-merger): Updates on cryptocurrency mining technology development stages or licensing arrangements offer markers for diversification viability.

- Regulatory monitoring: Continued adherence confirmations for NYSE listing criteria present ongoing governance checkpoints impacting access to capital markets.

Tracking these critical junctions provides internal insight into corporate resilience amid transformative structural shifts within both aviation service delivery models and emergent technological pursuits.

Latest Financial Snapshot: Insights into Liquidity and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $9.81mm | |

| 2025-12-31 | ||

| Current liabilities | $13.7mm | |

| 2025-12-31 | ||

| Current ratio | 0.72x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Net Income | 5,173,000 | |

| 2025-12-31 | ||

| Operating Income | 3,960,000 | |

| 2025-12-31 | ||

| Current Ratio | 0.72 | |

| 2025-12-31 |

Financial results ending December 31, 2025 indicate profitable operations with net income exceeding $5 million supported by operating income just under $4 million [F1]. These figures suggest operational control capable of generating positive earnings despite structural challenges inherent in emerging aviation platforms.

However, liquidity remains constrained as shown by current liabilities surpassing current assets leading to suboptimal short-term solvency ratios pointing toward careful cash flow management necessity going forward especially amidst integration-related costs or capital expenditure needs related to fleet servicing or technology investments [F1].

Disclaimer: This analysis provides insights grounded solely in Volato Group’s publicly available SEC filings and companyfacts data as of early May 2026 without offering investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments