Forian Inc. Strengthens Healthcare Analytics through Strategic Merger and Data Asset Expansion

Forian's April 2026 merger agreement and recent acquisition of Kyber Data Science mark a pivotal phase in its evolution within healthcare analytics.

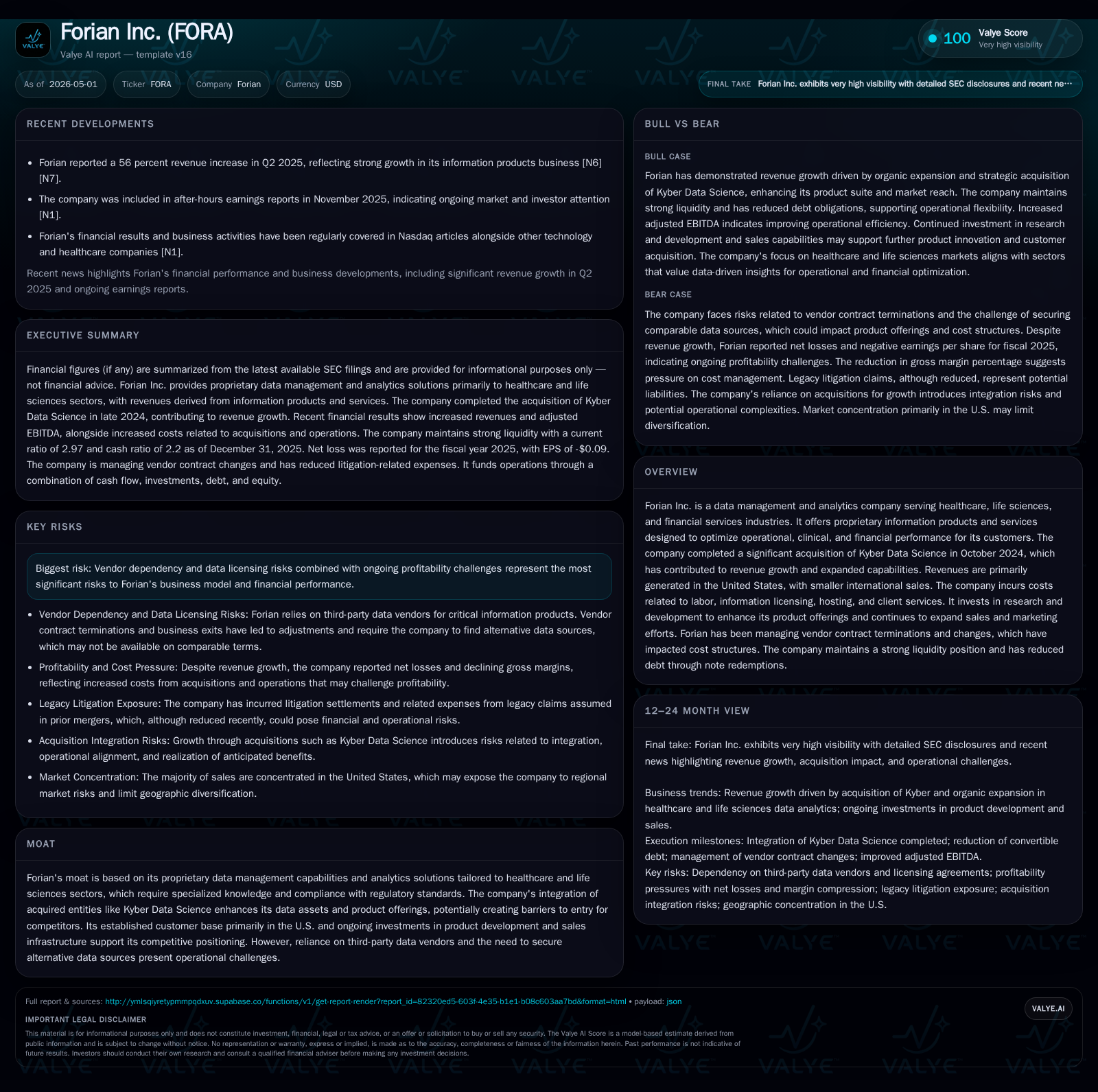

In early 2026, Forian Inc. sealed a transformative merger agreement signaling strategic expansion. This follows its October 2024 acquisition of Kyber Data Science, which has materially boosted revenue and product capabilities. The company’s proprietary data management and analytics solutions remain heavily focused on healthcare and life sciences, with a dominant U.S. revenue footprint. Forian faces operational pressures from vendor contract terminations but is actively investing in research and expanding sales capacity to sustain growth. Its current balance sheet reflects strong liquidity and no outstanding debt, supporting ongoing investments despite persistent operating losses.

Introduction: Merger Agreement as a Turning Point

On April 2, 2026, Forian Inc. entered into a definitive Merger Agreement with 2025 Acquisition Company, LLC aimed at creating enhanced scale and capabilities for the company’s operations in healthcare data analytics [S3]. This material event represents a significant inflection point in Forian's corporate lifecycle. Management has emphasized that the merger is designed to leverage combined assets for improved market position, operational efficiency, and accelerated growth potential. The event catalyzes a re-evaluation of Forian's strategic focus as it transitions into an expanded organizational structure anchored by proprietary data solutions [S3,S4].

Recent Operating Developments: Quarterly Update and Event Implications

In the latest quarter ended September 30, 2025, Forian reported revenues of approximately $7.76 million, up by over $3 million year-over-year driven largely by the Kyber acquisition completed in late 2024 alongside organic growth in legacy information products [S2]. However, cost of revenues increased disproportionately due to higher information licensing fees, data processing costs related to acquisition integration, and vendor contract changes resulting from upstream licensor restrictions announced mid-2024 [S2,S6].

Previously disclosed vendor exit announcements have led the company to terminate certain agreements effective end-2024, resulting in recorded cost adjustments totaling over $700,000 representing waived fees under terminated contracts [S2,S6]. Forian is actively pursuing alternative data sources to mitigate future supply risks but faces challenges in obtaining equivalent terms or data quality from other vendors [S1,S23].

Meanwhile, investments in research & development rose by over $900,000 compared to prior year periods due largely to Kyber-related expansion initiatives. Similarly, sales and marketing expenses increased by approximately $1.3 million amid efforts to expand selling capacity and brand awareness primarily within the United States market [S2]. General administrative expenses declined marginally due to lower stock compensation charges but remain elevated reflecting organizational support needs.

Business Model: Proprietary Analytics for Healthcare and Life Sciences

Forian generates revenue principally from subscription-like fees for its proprietary information products tailored to healthcare providers, life sciences firms, and select financial services clients [S1]. These products enable customers to optimize operational workflows, clinical outcomes, and financial performance through advanced data analytics derived from integrated datasets. Revenue recognition follows ASC 606 principles with performance obligations fulfilled upon delivery of analytic insights or data services.

The strategic acquisition of Kyber Data Science broadened Forian’s product suite by enhancing analytics sophistication and augmenting underlying data assets crucial for predictive modeling within regulated healthcare environments. These industries demand stringent compliance with privacy laws such as HIPAA alongside accuracy standards that differentiate Forian's offering from generalist analytics providers.

Cost structure drivers include labor-intensive R&D teams focused on continuous software innovation; substantial costs for hosting infrastructure enabling scalable analytics delivery; client service personnel ensuring solution adoption; plus fees paid to third-party data vendors whose licenses underpin the company’s datasets [S1]. Vendor terminations have added complexity to managing these costs while maintaining product continuity.

Competitive Landscape and Industry Structure

Forian operates in a niche yet competitive segment where specialized domain knowledge paired with proprietary datasets establishes entry barriers against commoditized analytics players. The company's moat lies primarily in its ability to integrate multiple licensed data streams accurately while complying with evolving regulatory landscapes common in healthcare and life sciences sectors [S1].

Nonetheless, dependence on third-party data vendors presents operational vulnerabilities as seen in recent licensing arrangement disruptions requiring costly adjustments or new contractual negotiations. This exposes the company to supply chain risks that competitors with owned or exclusive datasets may better mitigate.

Industry participants vary from large-scale healthcare IT conglomerates offering bundled solutions to smaller pure-play analytics firms competing on specialized feature sets or pricing flexibility. Forian’s approach leverages acquired entities like Kyber Data Science to continually enhance both depth of insights provided and clients' switching costs via ecosystem entrenchment.

Growth Drivers: Acquisition Synergies and Market Expansion

The acquisition of Kyber Data Science serves as the principal growth lever recently by expanding Forian’s addressable market through enriched analytic capabilities that appeal to more sophisticated clinical and operational clients [S1,S3]. Integration progress enables cross-selling opportunities across existing customer bases alongside development of new features accelerating adoption rates.

Sales force expansion plus sustained marketing investments underpin client acquisition strategies focused predominantly within North America where over 90% of revenues originate [S23]. While international revenue remains small—mostly Great Britain—and presents upside potential if scaled appropriately.

Looking ahead, anticipated merger synergies offer prospects for enhanced operational leverage including consolidated infrastructure costs, unified R&D pipelines, and expanded go-to-market channels post-close [S3,S5]. These factors collectively suggest a pathway toward improved margin profiles contingent on successful integration.

Risks and Constraints: Vendor Dependency, Profitability Challenges, and Integration Risks

Key risks persist around reliance on third-party data vendors whose upstream licensers can restrict access or alter terms unpredictably—as evidenced by contract terminations since mid-2024 forcing cost provisions and vendor diversification efforts [S2,S6]. Failure to secure comparable data could impair product value or increase costs materially.

Profitability challenges are evident given increasing SG&A expenses linked with acquisitions alongside ongoing R&D spend required for product competitiveness. Latest annual figures show operating losses approximating $3.76 million highlighting continued investment stage pressures despite revenue gains [F1].

The planned merger encompasses integration risks including management distraction from core operations during transaction execution—potential delays or failure could adversely affect business momentum—and realization of projected synergies remains uncertain given complexities involved [S5].

Looking Ahead: Key Milestones and Strategic Execution Markers

The merger transaction hinges on shareholder tender offer acceptance followed by customary closing conditions expected throughout 2026 quarters [S4,S5]. Observers should monitor updates regarding offer progress as well as scheduling disclosures for renewal or renegotiation of critical vendor licenses that impact supply stability.

Additional milestones include quarterly earnings reports detailing incremental contributions from merged operations alongside pipeline expansions fueled by R&D outputs or geographic penetration initiatives outside core U.S. markets.

Business execution will also be signaled through updates on cost containment effectiveness amidst vendor shifts; customer retention rates post-acquisition; new contract wins; product launch cadence; plus broader macroeconomic or regulatory factors influencing healthcare spending patterns applicable to Forian's clientele.

Financial Overview: Liquidity, Profitability, and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $13mm | |

| 2025-12-31 | ||

| Current assets | $43mm | |

| 2025-12-31 | ||

| Current liabilities | $14mm | |

| 2025-12-31 | ||

| Current ratio | 2.97x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

As of December 31, 2025, Forian held cash & equivalents totaling approximately $12.9 million with no reported debt liabilities contributing to a net cash position supportive of near-term funding needs [F1].

Despite this financial footing, Forian posted an operating loss exceeding $3.76 million for full year 2025 reflective of its investment phase characterized by increased cost absorption related to acquisitions (including Kyber), expanded sales efforts, research advancement expenditures, offset partially by revenue growth totaling over $22 million during first nine months ending September 30, 2025 alone [F1,S2,S8].

Management continues to emphasize funding operations via a blend of cash flow generation supplemented historically by equity issuances or asset divestitures ensuring runway adequacy amid profit-margin pressure conditions documented across recent SEC statements.

*Note: total debt metric current point last confirmed end-2022 per available evidence.[F1]

This analysis synthesizes publicly filed SEC documentation up through early Q2-2026 including Form 10-Qs for the three quarters ending September 30, 2025; annual amended Form 10-K/A for fiscal year-ended December 31, 2025; plus latest event reports regarding merger activity announced April 2026. All numeric disclosures are grounded solely in cited filings without extrapolation beyond confirmed facts.

The forward-looking prospects assume completing the announced merger transactions successfully while navigating vendor dependencies which remain pivotal operational variables for sustained competitive advantage within specialized healthcare analytics markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments