Kentucky First Federal Bancorp: Navigating Regional Mortgage Concentration Amid Interest Rate Flux and Appalachian Economic Realities

A focused review of KFFB’s strategic positioning as a regional mortgage lender confronting interest rate volatility and localized economic challenges.

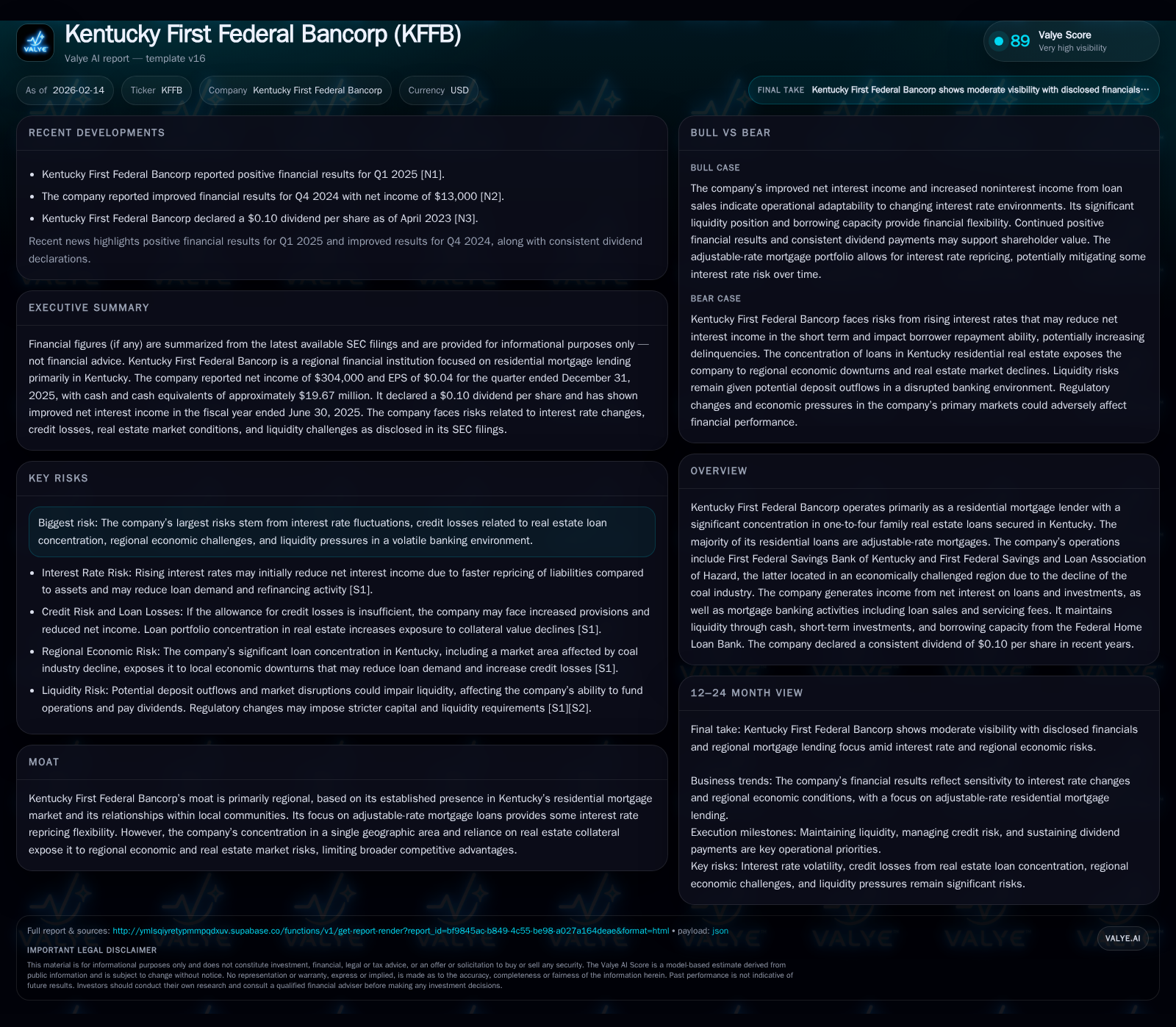

Kentucky First Federal Bancorp (KFFB) maintains a distinctive niche as a residential mortgage lender deeply embedded in Kentucky’s housing finance ecosystem, predominantly serving one-to-four family adjustable-rate mortgage borrowers. The company’s entrenched local presence creates a geographical moat yet concentrates exposure to regional economic shifts, notably the coal-dependent economy of Hazard. Recent Federal Reserve monetary tightening compressed net interest income by over $1.8 million before modest recovery, underscoring the dual-edged nature of adjustable-rate loans amid inflationary pressures. KFFB's liquidity remains solid with nearly $20 million in cash, supporting ongoing operations through Federal Home Loan Bank borrowing capacity, while a disciplined dividend policy reflects confidence despite macroeconomic headwinds and regulatory scrutiny. This analysis unpacks the interaction between KFFB’s geographic concentration, loan portfolio structure, and evolving external risks shaping its operational and financial outlook.

Kentucky Roots: The Geographical Moat and Market Focus

Kentucky First Federal Bancorp derives its primary competitive edge from its entrenched presence within Kentucky's residential mortgage landscape. Through its operating subsidiaries—First Federal Savings Bank of Kentucky and First Federal Savings and Loan Association of Hazard—the company maintains intimate ties to local communities, particularly serving homeowners seeking financing for one-to-four family residential properties. This hyper-local focus fosters customer loyalty and enables nuanced underwriting attuned to regional market conditions [N#valye_report_excerpt; S1 Item 1 Business].

However, this geographical concentration is a double-edged sword. While it creates barriers to entry for out-of-state competitors lacking local insight or relationships, it similarly exposes the company to systemic risks tied to specific Kentucky submarkets. For example, the Hazard area is challenged by structural economic headwinds from coal industry contraction, which directly impacts borrower repayment capacity and collateral values—potentially intensifying credit losses concentrated in that locale [N#valye_report_excerpt; S1 Risk Factors].

This localized moat distinguishes KFFB's operational strategy but necessitates proactive risk monitoring given the absence of diversification across broader geographies or industries.

Interest Rates and Income: Navigating the Tide of Volatility

The monetary policy landscape over recent years has heavily influenced KFFB’s financial performance. Beginning March 2022, the Federal Reserve enacted a series of rate hikes intended to counteract rising inflation. These increases persisted until August 2023 before policy reversal towards easing commenced in late 2024 [S1 Risk Factors].

These dynamics materially compressed KFFB’s net interest income (NII), which declined by $1.8 million or roughly 20% during fiscal year ending June 30, 2024 compared to prior year levels. The chief driver was an initial mismatch between rapidly rising funding costs on shorter-term liabilities versus slower asset repricing on loans and securities [F1]. As adjustments unfolded into fiscal year 2025 alongside rate cuts, NII partially rebounded—from $6.9 million in FY24 to $8.3 million in FY25—signaling some restoration of spread efficiency.

Adjustable-rate mortgages dominate KFFB’s asset base (~93.8%), granting repricing flexibility to recalibrate yields more rapidly than fixed-rate portfolios could amid ascending rates [N#valye_report_excerpt]. Nonetheless, short-term volatility in spreads can persist due to lag effects; higher interest expenses often precede full asset yield adjustments, compressing margins transiently [S1 Risk Factors]. This underlines the importance of portfolio composition in mitigating cyclical pressures.

Loan Portfolio Dynamics: Adjustable-Rate Mortgages in an Inflationary Era

KFFB's loan portfolio consists overwhelmingly of adjustable-rate mortgages (ARMs), representing approximately 94% of residential real estate loans with various initial fixed terms before monthly or annual repricing kicks in [N#valye_report_excerpt]. This structural feature provides inherent sensitivity to prevailing interest rates: when rates rise, borrower payments escalate correspondingly after initial floors expire.

In an inflationary environment persisting through much of 2025—with price pressures complicating household budgets—this payment volatility presents dual implications. On one hand, ARM repricing improves lender yields helping sustain net interest margins; on the other hand, increased borrower payment burdens may impair repayment capacity possibly elevating delinquency risk [S1 Risk Factors Lending Activities & Inflation].

Consequently, while ARMs offer operational advantages for managing rate cycles compared to fixed-rate products locked at lower coupons during low-rate eras, they also concentrate credit risk tied directly to macroeconomic affordability shifts.

Economic Underpinnings: Appalachia’s Coal Decline and Credit Risks

A critical contextual element shaping KFFB’s risk profile lies within its service footprint encompassing Appalachia's Hazard region—a community grappling with decades-long economic contraction catalyzed by coal industry decline [N#valye_report_excerpt]. This structural shift results in diminished employment opportunities and suppressed wage growth critical for sustaining timely mortgage servicing.

Such economic distress heightens credit risk factors for loans originated or serviced within Hazard. Borrowers confront constrained disposable income against mortgage obligations that reset upwards due to ARMs' indexed payments reacting to general inflation and Fed rate policy [S1 Risk Factors Credit Losses]. The interplay raises real possibility of rising delinquencies or impaired collateral values amid weakening property markets locally.

This localized credit vulnerability demands heightened caution around provisioning levels for expected losses as well as rigorous underwriting discipline tailored to microeconomic realities rather than perceptions informed solely by broader Kentucky housing trends.

Capital Strength and Liquidity: Fortifying Amidst Uncertainty

Despite external challenges, KFFB displays solid liquidity metrics supportive of operational continuity. As of December 31, 2025, cash and equivalents totaled approximately $19.7 million [F1], supplemented by undrawn borrowing lines with the Federal Home Loan Bank (FHLB). This liquidity arsenal buffers timing mismatches in cash flows while accommodating potential funding stress scenarios [N#valye_report_excerpt].

From a capital adequacy standpoint, the institution operates under regulatory governance requiring maintenance of minimum tangible capital levels monitored closely following agreements with regulatory bodies such as the Office of the Comptroller of the Currency (OCC) [S1 Forward-Looking Statements]. Deviations could prompt corrective actions impacting dividend distributions or portfolio growth strategies.

Heightened regulatory scrutiny coupled with stress-tested internal controls thus compel balance sheet prudence—a dimension further emphasized by the company's cautious dividend approach.

Dividend Discipline: Consistency Against the Odds

KFFB has consistently declared dividends at a rate of $0.10 per share in recent years despite prevailing uncertainties impacting banking profitability generally [N#valye_report_excerpt]. This stable payout conveys management's intent to maintain measured capital returns while preserving sufficient earnings retention for growth investments or loss absorption.

Given regulatory approval requirements tied to payout ratios amid capital adequacy thresholds—and potential limitations on dividends originating from subsidiary earnings—the continuity reflects deliberate conservatism rather than exuberant shareholder reward ambitions [S1 Forward-Looking Statements]. Investors interpret such steadiness as an anchor amidst shifting financial tides demonstrating underlying confidence without sacrificing balance sheet fortitude.

Regulatory Expectations and Forward-Looking Risks

Operating in tightly regulated domains obliges Kentucky First Federal Bancorp to navigate multiple compliance landscapes including capital regulation adherence, reporting transparency mandates, dividend approval protocols, and internal controls validation [S1 Forward-Looking Statements; S2 Risk Factors]. The OCC agreement outlines enhancements required post-examination findings designed to safeguard solvency metrics reducing systemic vulnerabilities.

Such regulatory dimensions impose incremental cost burdens while limiting strategic flexibility especially under prospective macroeconomic stress testing scenarios involving elevated inflation or regional economic deterioration. Additionally, governance discipline extends towards information security protocols confronting emergent cyber threats prevalent across financial institutions broadly.

Forward-looking statements caution that unanticipated changes—whether legislative evolutions or macro shocks—could materially alter prospects underscoring prudence over definitive forecasts [S1 Forward-Looking Statements].

Valuation Implications: Risk-Adjusted Opportunity in Regional Banking

Synthesizing this comprehensive view reveals Kentucky First Federal Bancorp as an institution shaped by both its strong local roots and attendant concentration risks characteristic of regional banks with limited geographical diversification. Its dominant focus on adjustable-rate residential mortgages confers tactical agility navigating changing interest environments though not devoid of borrower payment strain implications amidst inflationary cycles.

Persistent economic headwinds especially pronounced within Appalachian regions induce elevated credit vigilance through allowances for loan losses carefully calibrated against observed delinquency patterns tied intrinsically to localized socioeconomic factors rather than generic market assumptions.

Steady dividend payouts combined with ample liquidity buttress operational stability under regulatory frameworks demanding sustained capital adequacy despite pressure points emerging from rate volatility or macro uncertainty.

From an analytical perspective prioritizing idiosyncratic risk-adjusted evaluation rather than broad sectoral extrapolation suggests that KFFB epitomizes both opportunity grounded in community entrenchment alongside cautions warranted by single-region dependency compounded by economically challenged borrowers reliant on fragile industries.

This analysis incorporates publicly disclosed company information as well as regulatory filings up to February 2026 without extending speculative investment guidance. Readers should consider evolving economic conditions alongside individual risk tolerances when contextualizing these insights.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments