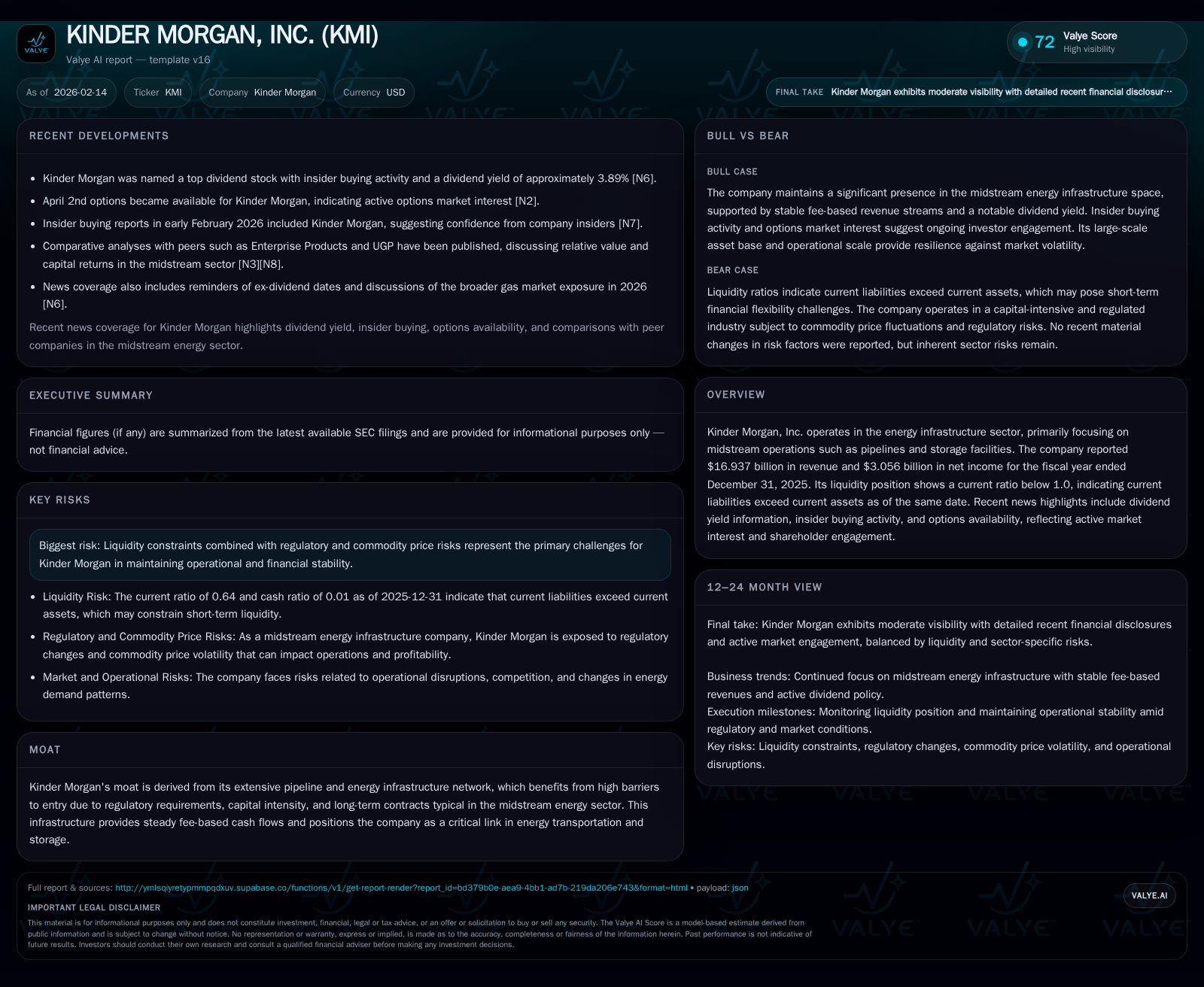

Kinder Morgan’s Midstream Resilience Amid Liquidity and Regulatory Pressures

Kinder Morgan balances robust fee-based cash flows and shareholder confidence with liquidity challenges and regulatory risks.

Kinder Morgan, Inc. leverages its expansive pipeline infrastructure to generate substantial fee-stabilized revenues, demonstrated by nearly $17 billion in 2025 revenue and over $3 billion in net income. Despite strong dividends and insider buying signaling confidence, the company faces a liquidity squeeze with current liabilities outweighing assets, underscoring short-term financial pressures. Regulatory complexities and commodity price volatility remain ongoing headwinds as KMI navigates evolving energy market dynamics.

Pipelines and Profits: Understanding Kinder Morgan's Core Infrastructure Moat

Kinder Morgan’s extensive midstream infrastructure network forms the backbone of its competitive edge. Its vast array of pipelines, storage terminals, and related facilities is entrenched amid significant regulatory hurdles that protect incumbents from easy entry by new players. The capital-intensive nature of pipeline construction combined with predominantly fee-based long-term contracts creates a revenue stream that exhibits durability against commodity price swings. With full-year 2025 revenue registering close to $17 billion, Kinder Morgan clearly demonstrates how this infrastructural moat translates into sizable, relatively stable cash flows — a hallmark of midstream energy that distinguishes it from more cyclical upstream segments [F1]. This structural advantage lies not just in asset scale but also in criticality to energy distribution networks.

Under the Microscope: A Close Look at Kinder Morgan’s 2025 Financial Performance

Financially, Kinder Morgan delivered net income of approximately $3.06 billion on $16.94 billion revenue through 2025, underscoring an efficient operating model firmly rooted in fee-for-service arrangements rather than commodity price exposure [F1]. The translation of top-line earnings into substantial bottom-line profit highlights effective cost control, scale leverage, and contract design favoring steady margins. This profitability underpins Kinder Morgan’s ability to sustain significant cash distributions to shareholders and fund incremental capital expenditures — critical levers for maintaining infrastructure integrity and growth potential.

Liquidity Squeeze: Analyzing Current Asset-Liability Dynamics

While the income statement paints a robust picture, the balance sheet reveals pressing short-term challenges. Kinder Morgan’s current ratio at fiscal year-end 2025 stands at 0.64—that is, current liabilities exceed current assets by a narrow but meaningful margin [F1]. Cash and cash equivalents are especially tight at around $63 million versus over $4.32 billion in current liabilities, indicating the company must rely heavily on non-cash working capital or external financing to meet near-term obligations.

This liquidity constraint merits close scrutiny given the sector’s capital intensity and regulatory environment that can lead to timing mismatches in cash flows [S1][S2]. Investing activities, debt maturities, or unforeseen regulatory sanctions could exacerbate strain if operational disruptions occur. Still, no material risk factor changes were noted recently, suggesting established risk management protocols remain in place [S2]. Nonetheless, stakeholders should monitor cash flow adequacy and covenant compliance given the gap.

Dividend Dynamics: What KMI’s Yield and Insider Activity Reveal About Confidence

Despite liquidity headwinds, Kinder Morgan maintains an attractive dividend profile; recently reported yields hover near 3.89%, placing it among top dividend stocks within midstream [N11]. Such yield levels often reflect robust free cash flow generation capacity aligned with management’s commitment to returning capital to shareholders.

Adding further credence to internal optimism is reported insider buying activity within KMI shares — a signal commonly interpreted as confidence by executives in underlying business prospects even amidst wider market volatility [N8]. Combined with ex-dividend notifications reinforcing payout reliability [N12], these factors speak to a shareholder engagement narrative that tempers concerns around short-term working capital tightness.

Navigating Regulatory and Commodity Risks in Midstream Energy

The midstream sector operates under a complex web of regulations governing environmental permitting, safety standards, tariff structures, and interstate commerce rules — all elements influencing Kinder Morgan’s operational flexibility [S1][S2]. Regulatory developments can delay projects or increase compliance costs unexpectedly.

Meanwhile, although Kinder Morgan benefits from fee-based revenues shielding it from direct commodity price fluctuations, linkages remain via throughput volumes tied to upstream activity levels impacted by oil & gas prices. Volatility can ripple through contractual arrangements or capital allocation priorities; thus commodity cycles still exert indirect influence.

Understanding these intertwined risks is critical when assessing Kinder Morgan’s stability outlook; no material updates occurred recently but vigilance remains warranted [S2].

Options Market Spotlight: Insights from Newly Available KMI Options

Market participants have shown elevated interest in Kinder Morgan shares with new options becoming available—specifically contracts expiring April 2nd — that open avenues for hedging or speculation linked to short-term price movement expectations [N5]. Such derivative availability often coincides with trending stock status heightened through volume surges or institutional positioning shifts [N7].

This development reflects active trading dynamics providing granular sentiment signals complementary to fundamental assessments. It suggests that notwithstanding traditional midstream profiles rooted in stable dividends, there is anticipation or concern about upcoming catalysts worth watching closely.

Comparative Midstream Landscape: Placing Kinder Morgan Among Peers

When positioned alongside peers such as Enterprise Products Partners (EPD), MPLX LP (MPLX), Liberty Energy, UGI Corporation (UGP), or Canadian giant Enbridge (ENB), Kinder Morgan occupies a nuanced spot blending scale with moderate valuation appeal [N1][N2][N3][N4][N6][N9][N10].

Enterprise Products has been highlighted for cheaper entry points driven by consistent capital returns [N4][N6][N10], while MPLX’s higher throughput volumes underpin recent earnings beats suggesting operational momentum [N2]. Liberty Energy similarly surprised positively on quarterly metrics [N3]. Meanwhile debate persists over relative value between UGP and KMI reflecting diverging growth profiles and regional focus [N9].

Kinder Morgan’s attributes remain compelling due to asset breadth yet tempered by more pronounced liquidity strains than some peers; these comparisons help refine understanding of relative opportunities within midstream equity landscapes.

The LNG Wave and Its Implications for Kinder Morgan’s Gas Exposure

A notable thematic shaping industry outlook is the accelerating global LNG demand — described as an 'LNG wave' — which carries implications for Kinder Morgan's natural gas midstream components [N13]. Increased export terminal activity could bolster volumes traversing KMI pipelines supplying liquefaction facilities.

This demand surge introduces growth avenues yet simultaneously raises operating complexity amid fluctuating export economics and geopolitical considerations influencing global gas flows. For Kinder Morgan, judicious capital deployment toward capturing LNG-related throughput expansion while managing associated risks will be pivotal moving forward.

Strategic Outlook: Balancing Growth, Stability, and Risk

Bringing these strands together lays bare a company executing a delicate balancing act — leveraging a deeply entrenched infrastructure moat generating strong profits yet grappling with tighter liquidity conditions worsened by regulatory burdens and market uncertainties.

Maintaining dividend attractiveness supported by insider confidence counters some investor fears regarding working capital constraints. The evolution of options market participation adds another dimension illustrating increased investor attention on short-term fundamentals.

As external conditions evolve—ranging from fossil fuel transition dynamics through increasing LNG market prominence to regulatory recalibrations—Kinder Morgan’s management faces the challenge of steering steady growth initiatives without compromising financial flexibility or operational resilience.

Longer term success will likely hinge on ability to innovate contract structures, optimize capital allocation amid tightening credit landscapes, and align shareholder returns with sustainable earnings generation inherent in midstream model.

Disclaimer: This analysis provides an informational overview rooted in publicly available filings and news reports as of February 14, 2026. It does not constitute investment advice or recommendations regarding Kinder Morgan or any other security. Readers should conduct their own due diligence before making financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments