Karyopharm Therapeutics at a Crossroads: Scientific Innovation Meets Financial Strain

Pioneering XPO1 inhibitor therapies position Karyopharm as an oncology innovator amidst looming liquidity challenges.

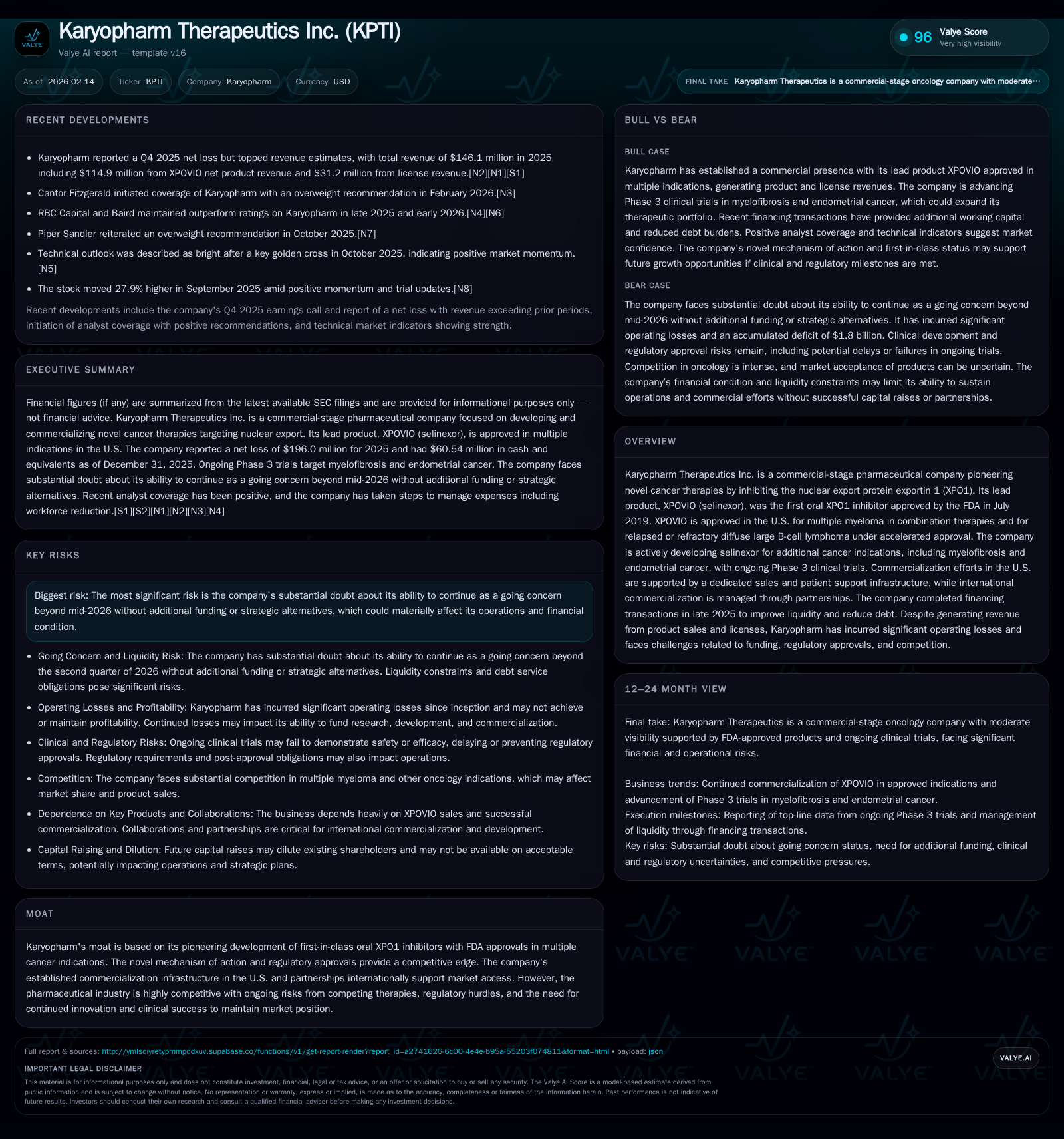

Karyopharm Therapeutics has carved its niche by developing selinexor, the first oral nuclear export inhibitor approved for multiple myeloma and DLBCL. While its expanding clinical pipeline and established U.S. commercialization infrastructure offer promising growth avenues, the company faces substantial financial headwinds, including going concern doubts extending into mid-2026. Strategic alternatives are imperative to balance its cutting-edge research ambitions with pressing capital demands amid intense oncological competition.

Breakthroughs in Nuclear Export Inhibition: XPOVIO’s Journey

Karyopharm Therapeutics’ hallmark innovation centers around its oral selective inhibitor of nuclear export, selinexor (branded as XPOVIO). This molecule targets exportin 1 (XPO1), a protein responsible for transporting tumor suppressors out of the cell nucleus; inhibiting this process disrupts cancer cell survival mechanisms. Selinexor's FDA approvals—first in July 2019—signify a milestone not only for Karyopharm but also for oncology drug development, marking it as the inaugural oral agent of this class.

Regulatory nods include approval for use in combination regimens for multiple myeloma patients with relapsed or refractory conditions and accelerated approval for diffuse large B-cell lymphoma (DLBCL), broadening its oncologic remit [S1][F1]. These endorsements provide a competitive moat grounded in novel mechanism-of-action pharmacology and regulatory validation, which bolster patent protections and market exclusivity periods.

The commercial viability of this first-in-class therapy has shifted Karyopharm from a purely research-driven entity toward a commercial-stage pharmaceutical firm with emerging revenue streams.

Clinical Pipeline: Expanding Indications and Trial Progress

Beyond existing approvals, Karyopharm is ambitiously expanding selinexor’s clinical horizons. The company is actively advancing late-stage trials targeting diseases such as myelofibrosis and endometrial cancer—serious malignancies lacking robust treatment options—to diversify future revenue vectors [S1][N1].

Recent earnings disclosures reveal ongoing Phase 3 trial enrollments with timelines oriented toward delivering pivotal data that could support label expansions. Management commentary underscores these trials as potential inflection points crucial for long-term growth amid competitive oncology landscapes [N1].

Success in these indications would validate the broader utility of nuclear export inhibition beyond hematologic cancers and may catalyze partnership interest or licensing premium.

U.S. Commercialization: Building Infrastructure for Market Penetration

Unlike many biotech peers reliant solely on R&D pipelines, Karyopharm has invested materially in building out U.S.-based commercial capabilities centered on XPOVIO. This includes a specialized sales force trained to engage oncologists treating complex hematologic malignancies alongside comprehensive patient support programs designed to ease therapy access and adherence [S1].

This operational foundation enables more direct feedback loops with prescribers and patients, allowing nimble responses to market dynamics relative to companies still developing their commercial infrastructures.

Such investments indicate management’s commitment to sustaining revenue streams essential for funding ongoing trials and corporate overhead.

Global Partnerships and International Reach

For markets beyond the United States, where regulations and commercialization channels vary considerably, Karyopharm leverages partnerships rather than direct sales operations [S1]. This approach contains fixed costs but introduces dependency on partners’ execution capabilities and profit-sharing arrangements.

While mitigating overhead pressures, reliance on licensees can dilute returns and complicate coordination between clinical developments and global regulatory submissions.

Managing these alliances effectively remains critical for maximizing international uptake of selinexor products amid broadening indications.

A Closer Look at Financial Health and Capital Challenges

Despite boasting product approvals and burgeoning revenues, Karyopharm’s financial position reveals acute stress. The December 2025 balance sheet shows cash and equivalents standing at approximately $60.5 million juxtaposed against current liabilities near $92 million—yielding a current ratio close to 1.12 [F1].

Operating losses have mounted, with net income plunging to -$196 million over calendar year 2025—a reflection of ongoing investment in trials coupled with commercial expansion costs [F1][N2].

A financing round completed in late 2025 injected about $36 million gross proceeds, providing critical liquidity inflows; yet management forecasts that existing resources plus operating cash flows will suffice only through the second quarter of 2026 [S2].

The narrow runway heightens urgency around managing cash burn rates without sacrificing clinical progression or commercialization momentum.

Risks Beyond R&D: Debt, Liquidity, and Going Concern Doubts

Perhaps the gravest concern arises from explicit "substantial doubt" disclosures regarding Karyopharm’s ability to continue as a going concern beyond mid-2026 without additional financing or strategic alternatives [S1][S2].

Financial covenants tied to convertible notes carrying 9% interest require maintaining minimum liquidity thresholds ($10 million currently escalating to $25 million post-October 2026), constraining financial flexibility further [S2]. Noncompliance risks triggering defaults potentially accelerating creditor actions.

These constraints underscore that absent new capital influxes or operational restructuring, sustaining R&D pipelines or even maintaining existing commercial efforts may become untenable.

Analyst Views and Market Sentiment: What Cantor Fitzgerald Sees

Intriguingly, Cantor Fitzgerald initiated coverage on Karyopharm with an Overweight rating shortly before earnings announcements [N3], furnishing a nuanced counterpoint to pervasive financial concerns.

Their bullish stance hinges on selinexor’s innovative mechanism combined with credible prospects from pipeline expansions that could drive revenue diversification. The analyst note stresses potential catalysts emanating from positive trial readouts across new indications as key value drivers.

This perspective encapsulates the classic biotech dichotomy: high scientific upside shadowed by execution risks anchored in financing realities.

Strategic Options on the Horizon: Funding or Restructuring?

Facing projected liquidity exhaustion by mid-2026, Karyopharm signals openness toward "strategic alternatives" encompassing additional financings, business development deals, or potential mergers/acquisitions [S1][S2][N1].

Follow-on equity issuances or debt restructuring would aim to elongate runway enabling trial completions; however dilution risks or unfavorable credit terms may weigh on shareholders.

Alternatively, expansive licensing agreements could unlock non-dilutive capital while sharing commercial risks internationally. M&A pathways could appeal if investor appetite favors consolidation within the increasingly competitive oncology sector.

Management communications denote these options remain under active evaluation amidst balancing swift capital needs against preserving long-term value.

Competitive Landscape and Innovation Imperatives

Despite pioneering status in oral nuclear export inhibition, Karyopharm confronts formidable competitors deploying diverse modalities such as CAR-T therapies, bispecific antibodies, proteasome inhibitors, and immunomodulatory agents across multiple myeloma and lymphoma spaces [S1].

Emerging therapies targeting overlapping pathways necessitate continual innovation both mechanistically and clinically to defend market share.

Regulatory environments also impose evolving hurdles requiring precise positioning of selinexor's risk-benefit profile supported by robust real-world evidence post-approval.

Maintaining this delicate innovation edge while managing financial constraints defines their operational crucible.

The Road Ahead: Balancing Scientific Promise with Fiscal Discipline

Karyopharm Therapeutics exemplifies the biopharma archetype where transformative science collides with exacting fiscal realities. Its unique XPO1 inhibitor platform underpins tangible therapeutic advances attested by regulatory acceptances; yet near-term survival hinges on deft liquidity management combined with adept strategic maneuvering.

Critical questions emerge: Can cash flow from XPOVIO revenues be optimized sufficiently while pipeline assets mature? Will capital markets reward continued risk-taking if milestones align? How might governance steer prudent resource allocation without stifling innovation?

Answering these will shape whether Karyopharm navigates successfully through this precarious phase or capitulates under funding pressure before realizing its full scientific promise.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as of February 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments